$500,000 a Year Yet Struggling? Let's Do a Double Take

(Bloomberg Opinion) -- Every so often you come across an article about someone who makes a lot of money, but who claims to be just scraping by. Among the more famous of these was a Wall Street Journal infographic from 2013 depicting the travails of single mothers making $260,000 a year and married couples making $650,000. Another was a 2017 graph on Reddit showing how a young Seattle resident spends a $100,000 annual income. Just this month, CNBC ran a story entitled “Here’s a budget breakdown of a couple that makes $500,000 a year and still feels average.” The story was based on a report by the website Financial Samurai, about a 30-something couple with two children living in New York City.

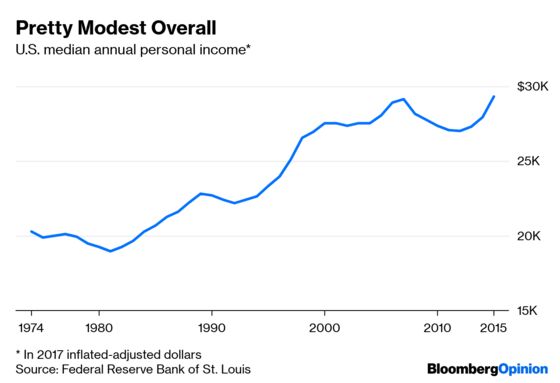

Each of these reports produces an outcry on social media, as people rush to denounce the hubris of high earners who claim to feel stretched. That’s only to be expected, given that median personal income in the U.S. is just a little more than $30,000, even including government benefits:

The median household income is about double that, and the median family income is roughly $76,000, but none of these comes close to the numbers in these articles.

Defenders of these stories will point out that because living costs and tax rates differ from place to place, a high income in New York City or San Francisco buys much less than a high income in a small town in Texas. This is certainly true. For example, the website Apartment List shows the median rent for a two-bedroom apartment in San Francisco as $3,100 a month — more than three times as much as the $1,020 a comparable apartment lists for in Houston. A small town would cost even less than Houston. And Texas has no state income tax, while California’s tax rates range from 1 percent to 12.3 percent.

But these regional differences only go so far. The median annual income for a family of four in New York City is a little more than $104,000. There’s no city in the world where a $500,000 income, like the one described in the Financial Samurai article, wouldn't be considered very high.

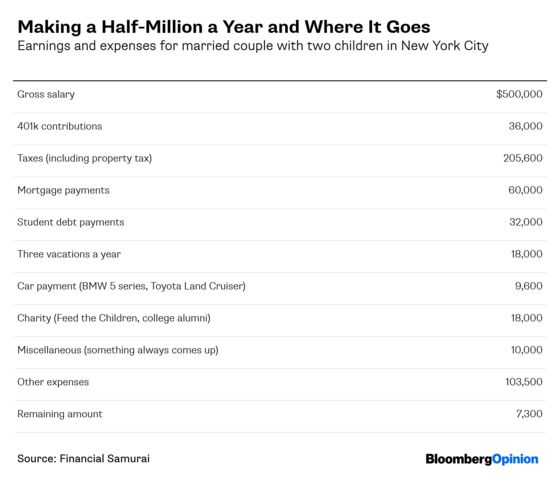

So if the people profiled in these articles are barely scraping by, what are they spending their money on? Here’s a condensed version of the income and expenditure breakdown for the $500,000 couple:

As you can see, this family isn't under financial stress. Spending $18,000 on vacations a year, giving another $18,000 to charity, keeping two luxury cars in New York City, and spending $10,000 a year extra because “something always comes up” are things that are out of reach for the vast majority of Americans. One recent survey found that 40 percent of Americans couldn’t even cover a $400 emergency expense.

But also, despite the claim to be scraping by, this family saves quite a lot of money in addition to the $7,300 “left over” every year. Contributions to 401(k) retirement plans are savings. That’s $36,000 a year for two adults — and that’s not even counting any employer-matching contributions, which probably aren’t included in the couple’s income in this table. The couple also makes $60,000 in mortgage payments a year and $32,000 in student-loan payments. Some of these payments are applied to the principal on their loans, which increases the couple’s net worth by either building their home equity or by reducing their student debt. So that’s also savings.

Depending on how much of their loan payments are going to principal, this family is probably saving $100,000 a year, or 20 percent of their gross income. They aren’t scraping by — they’re socking away quite a bit of money, building up wealth in 401(k) accounts and the family home.

Because 401(k) contributions and mortgage payments are structured methods of wealth-building, they might not feel like savings. But both 401(k) plans and mortgages are commonly cited as strategies to nudge Americans to save more. Ironically, their success may be predicated on the fact that people don’t realize how much they’re putting away every month.

But there might also be another reason high-income Americans don’t feel as rich as they are — in a country of rampant inequality, there’s always someone richer. A couple making $500,000 might rub elbows with other couples making $2 million. That couple will go to events and meet other couples making $20 million, and so on. At each level of affluence, many social climbers probably look at the people on the next rung higher and feel a burning need to keep pace.

Ultimately, living a happy life probably requires letting go of envy and appreciating what one has. But it’s also no wonder that so many Americans, even members of the elite, yearn for a more equal society. Even wealthy people might benefit from a smaller gap between the classes.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.