(Bloomberg Opinion) -- If you were already inclined to believe that the global slowdown in growth was beginning to hit the U.S., this week’s data shored up your argument. And the new information makes what Chairman Jerome Powell says at the Federal Reserve’s upcoming meeting almost as important as what the Fed does.

First, the numbers. It’s not just that job growth, at 155,000, was some 43,000 below the consensus forecast, and that there were also downward revisions for of the previous two months’ numbers. More disturbing is that the so-called underemployment rate, which includes workers who have only loose attachments to the workforce or have given up looking for a job, ticked up from 7.4 to 7.6 percent. (The economy had previously been doing a good job of drawing those workers into regular employment.)

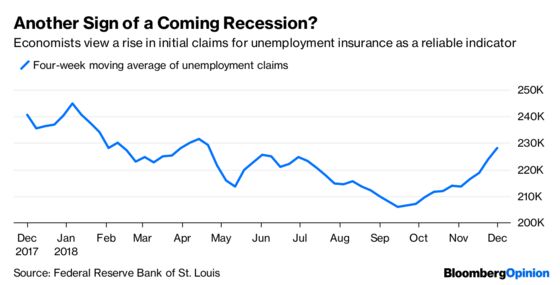

And there are the initial claims for unemployment insurance, which came in earlier this week. The four-week moving average has started to make what looks like the beginning of a distinct leg upwards. This is significant: Along with the (partially) inverted Treasury yield curve, a rise in initial claims for unemployment insurance is a reliable indicator of a coming recession.

All of this makes what the Federal Reserve does at its meeting the week after next even more important, and I have argued that it re-evaluate its path of rate hikes. Markets are increasingly pricing in the probability that the Fed could hold off on a long-anticipated December rate increase; last week, Fed Funds futures contracts indicated just a 17 percent chance that the Fed would choose to hold rates steady at the next meeting, but this week those same contracts were indicating a 32 percent chance.

Given Powell’s temperament, however, it’s highly unlikely that the Fed would make such a major course correction without giving the markets a heads up. In the absence of a horrifically bad signal — like sudden collapse in interest rates on 10-year Treasury bonds or a full inversion of the yield curve — not raising rates would probably just cause confusion.

The secret to calming markets and leaning against slowing economic activity will not be the rate decision, the much-studied dot plots or even the formal statement. What will be crucial is the tone Powell sets in the press conference following the meeting — and whether his concerns are amplified by other Fed officials.

Not all these officials agree. That’s OK; board governors and the regional bank presidents operate with different economic models. What markets need to see, however, is Fed governors and presidents expressing a shared and increased concern about the new data.

On Thursday, the president of the Dallas Fed, Robert Kaplan, did exactly that, stressing the importance of patience in an uncertain economy. If Powell picks up on this theme, and makes it clear that the yield curve and potential upswing in jobless claims are affecting the committee’s thinking, then there could be a significant easing of financial conditions going into next year.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a senior fellow at the Niskanen Center and founder of the blog Modeled Behavior.

©2018 Bloomberg L.P.