Struggling to Reach 2 Percent Inflation? Try Three!

(Bloomberg Opinion) -- Japanese authorities have picked a heck of a time to go wobbly.

Wobbly on the Bank of Japan's inflation target, that is. Far from abandoning or watering down the idea of achieving 2 percent, as the finance minister has suggested, there’s a case for defending it. By sticking with this goal, officials would ensure consumers and businesses appreciate the intent behind that magical number.

If they don't, there's a chance not only that 2 percent won’t be reached, but that 1.5 percent or even 1 percent becomes unattainable. The lower the bar, the deeper the deflationary mindset becomes. It's as much about psychology as anything else.

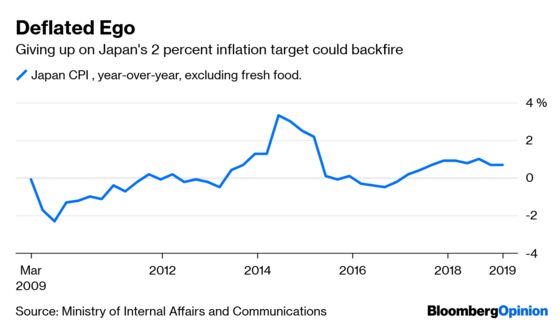

It’s true, the Bank of Japan hasn't been able to generate consumer price increases of 2 percent on a sustained basis, despite throwing a lot at it: quantitative easing, negative interest rates and purchases of exchange-traded funds, among other things. More worryingly, after a spurt higher, inflation is again receding. Embarrassingly for the BOJ, many of its forecasts have been too optimistic.

Frustration has spilled over into official discourse. Earlier this month, Finance Minister Taro Aso openly debated whether getting to 2 percent quickly is worth all the trouble. The resulting fracas – Governor Haruhiko Kuroda effectively repudiated him after the bank's policy meeting that day – had Aso scrambling for cover.

That wasn't the end of it. Aso and Prime Minister Shinzo Abe were quizzed about it in parliament last week. They dutifully affirmed the sanctity of the 2 percent target and faith in Kuroda. And while Aso assured lawmakers that there's no daylight between the three of them, he also refused to retract his initial remarks.

On the face of it, Aso is stating the obvious. The BOJ is having a tough time of it and being reckless with monetary policy isn’t the answer. The thing is, you aren't supposed to question sacraments like inflation targets, generally set around the world at about 2 percent. But why not? Maybe they are too low, rather than too high. Why not set it at 3 percent, or higher, if you really want to change assumptions?

Part of the zeitgeist is that, with inflation too low pretty much everywhere, keeping expectations healthy is a big priority. If major economies are heading into a downturn, which they seem to be, then the big fear is that central banks have no ammunition left to combat that potential slump.

Talk is of Japanification, the idea that economies can be characterized over the long term – not for merely a phase – by fear of deflation, low rates of growth, and zero or negative interest rates. Federal Reserve Chairman Jerome Powell alluded to this when he said low inflation is “one of the major challenges of our time.”

If Japan tweaks its target lower or enshrines into policy the idea it might not happen, then it could undo progress that has been made. Japan's economy isn't doing too poorly. Inflation had a fighting chance before a consumption-tax increase in 2014 damped activity. Unemployment is 2.5 percent.

Pushing inflation up depends on people being convinced something has changed and that such efforts aren't temporary. (Paul Krugman wrote convincingly on this subject last year.) The risk is that Aso reinforces doubts already out there.

Of course, the BOJ shouldn't pursue objectives completely divorced from reality. The trick is to acknowledge the hard yards ahead without convincing the public that the white flag is being hoisted. If the central bank surrenders, why shouldn't the public? Nothing good would follow.

Japanification is on everyone’s lips for less-than-flattering reasons. Arguably the real fight against deflation there didn’t begin until 2013. It would be a shame if Tokyo did something to imply a weakening resolve.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.