The Bad and Less Bad News About Italy's New Budget

(Bloomberg Opinion) -- The budget unveiled on Monday evening by the Italian government looks like a "Greatest Hits" album containing all the measures that have failed to spur growth in the past.

The populist administration has largely neglected companies and younger workers, who will receive little benefit from the proposed policy changes. Instead, it is letting workers retire early and handing out a still undefined income support scheme, which will be hard to design and even harder to implement sensibly.

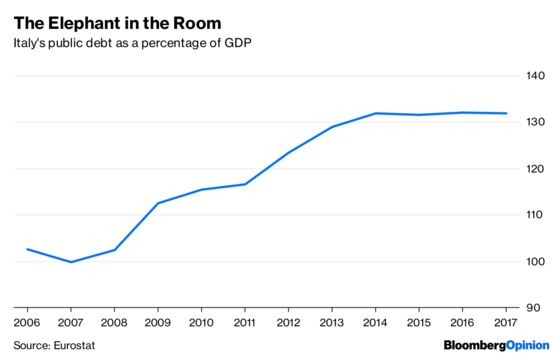

In the great tradition of Italy's governments from the 1970s and 1980s - who accumulated a large chunk of the country's enormous public debt - the League and Five Star are being very generous with money they don't have. The result will be a negligible boost to growth and higher budget deficits, which could turn out to be even worse than forecast.

The new Italian administration wants to break with "austerity" and mend public finances through higher growth. The government has pencilled in a budget deficit of 2.4 percent of gross domestic product for next year, which it believes will help to lift the rate of expansion of the economy to 1.5 percent.

The executive forecasts that the policy package will boost growth by 0.6 percentage points, but it is extremely hard to see where this would come from. True, watering down past pension reforms to let workers retire at 62 (provided they have paid contributions for 38 years) will create some vacancies in companies. But it is delusional to imagine that these will all be filled, especially at a time of high uncertainty and slowing European growth. Any income support scheme will put some money in the pockets of low-earners. But the risk is that many of the recipients will be tax avoiders or workers in the black economy, not the country's poorest. Money will also be spent on imported goods, reducing its impact on growth.

Meanwhile, companies are set to lose a range of deductions, which will result in an increased tax burden. Some self-employed workers will receive a tax cut, but this will not extend to the majority of workers. The effects of all these measures on the short- or long-term rate of economic expansion will be negligible. Little wonder, Italy's fiscal council has rejected the growth forecasts from the government as unrealistic.

Such an excess of optimism puts in peril the fiscal forecasts too, and there are also other reasons to be doubtful. The government has unveiled a generous tax amnesty, as well as on some poorly specified spending cuts. The former is a one-off measure, which could actually discourage some workers from paying their taxes since they expect more amnesties in the future. As for the latter, they may not be delivered in full. The combination of all these risks could well mean that the government will miss its target of letting public debt fall marginally next year.

The budget does tell investors something positive, at least for the short run: The governing parties have not lost their willingness to compromise. The Five Star Movement had to make an enormous u-turn on the idea of a tax amnesty, which it relentlessly criticized in the past. Meanwhile, the League will have to accept that the income-support scheme will largely benefit the south, where it has a smaller (albeit growing) base. The government partners seem on course to have passed their first big test of reciprocal loyalty. This may help to explain why government bond yields fell today and the stock market rallied.

Finding a compromise with the rest of the EU will be a far harder task. The European Commission has already sent a letter to Finance Minister Giovanni Tria, saying there was a serious risk the budget would violate the bloc's fiscal rule. Commission President Jean-Claude Juncker said on Tuesday that the rest of the EU could revolt over Italy's budget.

All of this will not matter to the League and Five Star. They aim to arrive to the elections for the European Parliament in May having delivered on some of their pledges and having shown that Italy does not take orders from Brussels. This strategy may achieve some short-term electoral victories, but it will leave Italy well short of a long-term revival.

To contact the editor responsible for this story: Therese Raphael at traphael4@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns and editorials on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2018 Bloomberg L.P.