(Bloomberg Opinion) -- A corporate battle at Telecom Italia SpA shows why it’s tough to be an investor in Italy these days. The government is interfering with a private company to get hold of its most prized asset: the country’s phone and broadband network. The opposition tacitly supports the plan. Italy is playing fast and loose with property rights and no one seems to care.

The ruling Five Star Movement has presented a draft amendment to a fiscal decree, which envisages creating a single company to combine the networks of Telecom Italia and Open Fiber, a smaller rival. Luigi Gubitosi, who became Telecom Italia’s CEO at the weekend, is open to the plan. It’s also supported by Elliott Management Corp., a hedge fund from New York that’s in effective control of Telecom Italia. Populists can embrace some strange bedfellows.

Vivendi, the French media company that is Telecom’s largest shareholder, is opposed.

It would be easy to see this episode as the interests of the public and private sector happily aligning, but it’s murkier than that. To make things worse, it’s not clear how Rome means to pay.

The problem is that Open Fiber was the brainchild of a previous Italian government, which wanted another company to help accelerate broadband and fiber development in the country alongside Telecom Italia. Cassa Depositi e Prestiti, a state-controlled lender, owns half of Open Fiber, alongside Enel SpA, the state-controlled energy company. But Rome has subsequently realized that it wasn’t the smartest move to have two fixed network suppliers duplicating investment. So it’s trying to devise a way to repair its own mistake.

With Telecom Italia’s new CEO open to the merger, too, you could argue that this is merely the will of company and so should be respected. But you need to understand the background here.

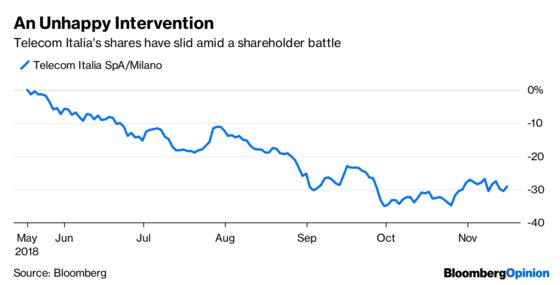

In the spring, the CDP took a minority stake in Telecom Italia and its votes helped Elliott seize control of the board from Vivendi. So Telecom Italia’s new willingness to play along is not merely the result of market forces, but of deliberate government meddling. Vivendi wouldn’t have been so amenable. Meanwhile, Telecom Italia’s shares have fallen by a quarter in the past six months.

This tale of state intervention is part of a broader story on the respect of property rights in Italy. Last Summer, when a bridge collapsed in Genoa killing 43, the Italian government immediately blamed the road operator, Autostrade per l’Italia SpA, saying it should lose its license. The Five Star Movement, in particular, wanted a greater role for the state in operating Italy’s motorway network.

Three months later, few formal steps have been taken, but the rhetoric has severely dented the credibility of Italy’s services sector for foreign money. Even if the blame does end up lying with the operator, who would want to invest in a country where the government isn’t bothered by due process?

The paradox is that Italy has little money to pay for its new penchant for intervention. Of course, Rome is free to pursue any license or network it wants, so long as it offers proper compensation. In the case of Telecom Italia, this would mean paying between 10 and 15 billion euros – depending on the valuation of the network – or taking over a chunky portion of the company’s debt, which has the network as collateral.

The trouble is that Italy is saddled with an enormous public debt of its own and is struggling to find resources to relaunch its anemic growth rate. One option would be for CDP to take over these assets. But this would still add to the state’s pile of contingent liabilities.

Rome said in its latest budget that it will dispose of state assets worth about 1 percentage point of GDP to cut debt. This is hard to square with new nationalizations. Or with coherent policy-making.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns and editorials on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2018 Bloomberg L.P.