When the Dollar Talks, the Fed Should Listen

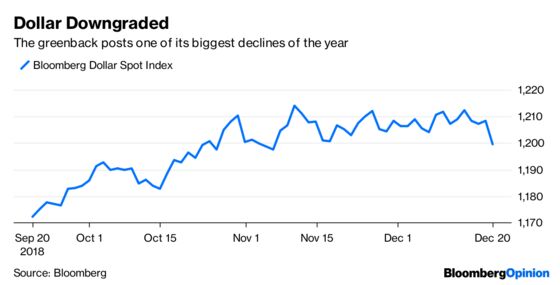

The Bloomberg Dollar Spot Index, which measures the currency against a basket of its main peers, tumbled as much as 0.84 percent.

(Bloomberg Opinion) -- Overlooked amid the big drop in stocks and Treasury yields after what was generally perceived by the market as a disastrous interest-rate hike by the Federal Reserve on Wednesday and the ensuing threat of a government shutdown is the dollar. It’s said that a nation’s currency is not much different from a company’s share price in that it’s the best indicator of investor sentiment. If that’s true, then the greenback got slapped with a “sell” recommendation.

The Bloomberg Dollar Spot Index, which measures the currency against a basket of its main peers, tumbled as much as 0.84 percent Thursday in its biggest decline in seven weeks. In a sign of how rare such a move is, the index has dropped more than 0.8 percent only four other times this year. As one of the ultimate havens in global markets, the dollar should be benefiting from the current turmoil in risky assets and rising concern about a global economic slowdown. But the fact that investors are fleeing the currency suggests that they are more concerned that the Fed is making a mistake by not listening to the message being sent by markets and will drive the economy into a recession just as the political rancor in Washington heats up. “A sharp sell-off in the dollar is perhaps the ultimate rebuke,” FTN Financial chief economist Chris Low wrote in a note to clients Thursday. “When a central bank is more hawkish than expected and its currency drops, you are witnessing the collective wisdom of the global market.” In another blow to the dollar, the Bloomberg Consumer Comfort Index’s monthly expectations gauge fell to a one-year low in December as more respondents said the economy is getting worse.

The foreign-exchange market is the largest in the world, with more than $5 trillion of currencies changing hands each day. As such, it would be foolish to ignore the signals it is sending. Just last month, before all the latest turmoil, S&P Global Ratings said that it saw a 15 to 20 percent chance of a recession in the next 12 months, up from its previous estimate of 10 percent to 15 percent.

STOCKS GET A TASTE OF FED COURAGE

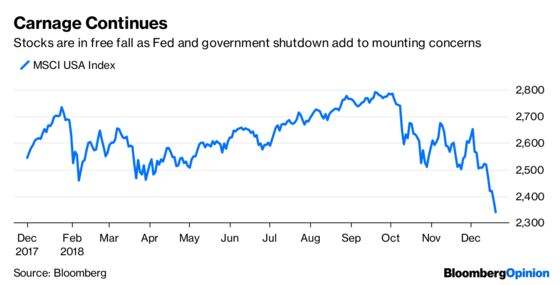

The MSCI USA Index of 621 stocks fell on Thursday to its lowest since August 2017 as technology shares continued to crater. The benchmark is now down some 16 percent from its closing high this year on Sept. 20. While the decline is certainly painful for most everyone except those who were betting against stocks, a surprising number of market participants are calling the move cathartic and necessary as the Fed weans the market off of years of extraordinary stimulus that artificially propped up risk assets. Between 2008 and 2015, the Fed injected a bit less than $4 trillion into financial markets through its bond purchases despite an economy that grew at an average of more than 2 percent after 2010. This year, almost $500 billion has been withdrawn as the Fed has shrunk its balance sheet assets. “It’s valid to say that (Fed Chairman Jerome) Powell should have been more dovish this week than he was, but it’s important to remember that the economy and the markets are only as fragile as they are today because his predecessors lacked the courage he apparently” has in removing that accommodation, former hedge fund manager Jesse Felder wrote in his widely followed The Felder Report blog. The Fed’s “real policy error was keeping rates at zero for (seven) years, waiting an eternity in reversing it and quintupling the size of its balance sheet,” Bleakley Financial Group chief investment officer Peter Boockvar wrote in a note to clients Tuesday. “After that, the Fed entered a no-win situation in reversing it no matter when it came and regardless of the pace.”

NOT ALL BONDS BENEFIT

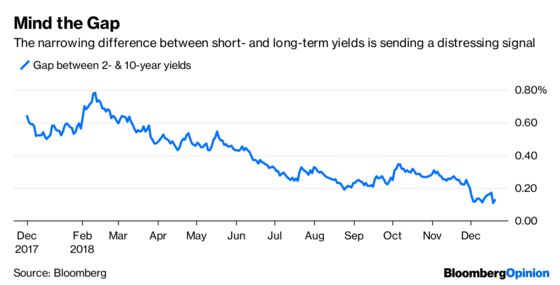

Although Treasuries were unable to hold their gains from Wednesday, the yield on the benchmark 10-year note managed to stay below 2.80 percent. To understand how surprising the rally in the bond market this month has been, consider that the median estimate of more than 50 economists and strategists surveyed by Bloomberg in June was for the yield to be around 3.20 percent by now. As with stocks and the dollar, the concern is that the Fed’s policies will drive the economy into recession sooner than otherwise would have happened more naturally. “We’ve seen the peak of Treasury yields,” Tano Pelosi, a portfolio manager at Antares Capital, told Bloomberg News. Those worries are being manifested in the yield curve, or the difference between short- and long-term bond yields. The gap between two- and 10-year Treasuries has shrunk to around 10 basis points from almost 80 in February. Everyone is worried that the curve may invert, with long-term yields falling below short-term yields, because that’s usually a sign of a looming recession. “As the curve keeps flattening on us, it’s telling us that monetary policy is being too restrictive and that we don’t have enough reserves in the system to stimulate the economy,” said Scott Minerd, chief investment officer at Guggenheim Partners. The upside to lower long-term Treasury yields is that they have to potential to ease borrowing costs for companies. But that’s not really happening, as the general “risk off” environment has investors demanding an extra 1.40 percentage points in yield to own investment-grade corporate bonds instead of Treasuries, the most since 2016.

OIL TAKES EVERYONE BY SURPRISE

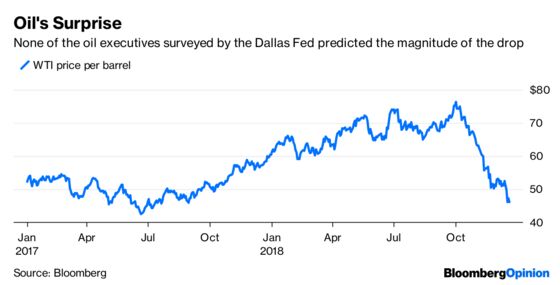

Oil prices dived again on Thursday, tumbling as much as 3.24 percent. At about $46 a barrel, West Texas Intermediate crude is down from about $77 in early October and the lowest since September 2017. What’s surprising about the move, which many market participants tie not only to a glut of oil but rapidly declining demand, is how few saw it coming, even among those in the business. The Federal Reserve Bank of Dallas in September asked 166 oil and gas executives a simple question: what do you expect the WTI crude oil price to be at the end of 2018? More than 80 percent reckoned in the high $60s to low $70s range, according to Bloomberg News’s Kevin Crowley. The lowest forecast was $55. Although the drop in oil prices is benefiting consumers, who are enjoying much lower gasoline prices, it’s contributing to the decline in equities. During the last oil price crash in 2014, the S&P 500 Index and Brent crude moved in opposite directions. Oil’s fall failed to prove much of a drag on U.S. equities and vice versa, as represented by a strong negative correlation coefficient of 0.65 between the two assets, according to Bloomberg News’s Alex Nussbaum and Brandon Kochkodin. A correlation of 1 means two assets move in lockstep, while -1 means the opposite. The relationship has changed during the commodity’s current collapse, with oil and the S&P 500 generally moving in tandem as the correlation has turned to positive 0.75. Part of the reason for this is the large amount of debt taken on by energy firms in recent years. A drop in oil prices generally squeezes their profit margins, making it harder for them to meet debt payments, which in turn weighs on their share prices.

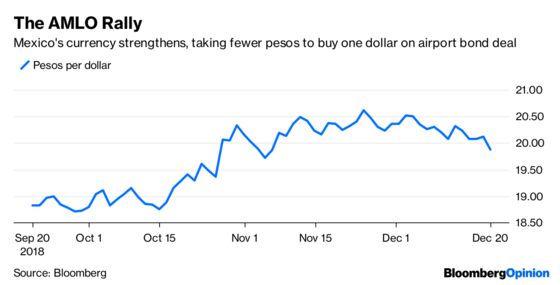

MEXICO’S AMLO WINS BACK SOME TRUST

Mexico was a bright spot in an otherwise tough day for emerging-market assets. The S&P/BMV IPC index of equities jumped as much as 0.88 percent even as the global MSCI Emerging Markets Index dropped as much as 1.17 percent. The peso strengthened more than 1 percent in its biggest gain since early October. Optimism is rising that new President Andres Manuel Lopez Obrador, who got off to a rocky start with international investors after he was elected, will solve a standoff with airport bondholders that had roiled markets. Things started to go off the rails in late October, when AMLO ditched a $13 billion airport project for Mexico City backed by some of the nation’s wealthiest businessmen. Bonds backing the project tanked. But now there are reports that a majority of bondholders accepted Mexico’s offer to buy back $1.8 billion of the debt. “It is a step in the right direction,” Jan Dehn, the head of research at Ashmore Group Plc in London, told Bloomberg News. “AMLO had a poor start in terms of creating confidence. He did not appear to show leadership on key issues, but after the budget and now this airport bond dispute he is winning back some trust.” As Bloomberg News reports, even though the deal was a big victory for AMLO because it wards off a potentially nasty battle with bondholders, it comes at a steep price. The government will now spend $1.8 billion — an amount which came from an existing trust for the airport’s construction — in an expensive buyback.

TEA LEAVES

The U.S. Commerce Department on Friday will release its monthly report on personal income and spending for November. The October data showed purchases jumped 0.6 percent that month, which was more than forecast and the biggest increase since November 2017. The data for this November is likely to be more subdued, rising just 0.3 percent, which is in line with the average over the past five years. Still, the data will be closely watched to see if the big drop in stocks in October, when the S&P 500 tumbled 6.94 percent, had any impact on consumers’ psyche or if the drop in gasoline prices made consumers feel flush. A government report last week showed that retail sales among a so-called control group subset, which some analysts use to gauge underlying consumer demand, climbed 0.9 percent, the most in a year and more than double projections.

DON’T MISS

Fed Weighs Growth Against Market Fragility: Mohamed A. El-Erian

Crypto’s Terrible Year Was Actually Pretty Good: Aaron Brown

U.S.-Japan ’80s Trade War Holds Clues to China Spat: Noah Smith

Emerging Markets Are Fed Up With FedEx and the Fed: Shuli Ren

Putin Erases the Truth About the Ruble: Leonid Bershidsky

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.