(Bloomberg Opinion) -- When politicians face voters in troubled economic times, non-economic issues tend to recede. When economic performance is strong, by contrast, serious underlying problems may not get the attention they deserve.

That seems to be happening in Israel, where surveys show that voters are worried about their economic future. But with just two months to go before the parliamentary election that will decide whether Benjamin Netanyahu gets a record fifth term as the longest-serving prime minister in the country’s 70-year history, the economy isn’t a big part of the political debate.

Maybe that’s because Israelis are preoccupied by their many external conflicts, with Palestinians, Hamas, Hezbollah and their proxies in the West Bank, Gaza, Lebanon, Syria and Iran.

But sheer economic vigor undoubtedly explains a lot. Israel’s gross domestic product has been rising at an average annual rate of 3.69 percent since 2000, inflation has been negligible at 1.57 percent, and unemployment has fallen to half of its average for the period of 7.4 percent.

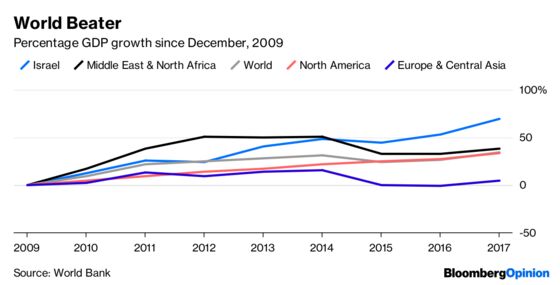

The nation of 8.4 million people — a little more than Switzerland and a little less than Austria — has outperformed these European stalwarts since the global economic research firm MSCI Inc. upgraded it to developed-market status in 2009. Israel’s GDP growth of 69 percent since then is more than 17 times what Austria managed and almost three times what Switzerland mustered, according to data compiled by Bloomberg.

Among the 36 developed economies that make up the Organisation for Economic Development and Cooperation, Israel is poised to climb to second-fastest growing in 2020 and will be No. 4 with Chile this year sharing 3.6 percent growth, behind Slovakia (4 percent), Poland (3.8 percent) and Slovenia (3.5 percent).

That’s not to say that Israel is joining the list of 10 happiest countries, which includes Switzerland, anytime soon. While 60 percent of Israelis said they are satisfied or very satisfied in a recent Israel Democracy Institute survey, a similar percentage said they are worried or very worried that they wouldn’t be able to help support their children, and 65 percent said they are concerned they aren’t saving money for the future.

Israel’s poverty rate of 17.7 percent is the second-highest in the OECD (many among Israel’s fast-growing ultra-orthodox population refuse to work). There is persistent dissatisfaction with infrastructure, public spending, hospital crowding and the so-called dual economy, where two-thirds of the workforce get less than the national average wage.

For all the pessimism inside and outside the country, there is no question that Israel is outperforming most of Europe and the OECD with accelerating growth that has taken it from 15th-fastest growing in 2015 to No. 9 in 2017 and 2018. Four years before quarterly unemployment reached a record low of 3.6 percent in 2018, Israel’s jobless rate hovered consistently below Austria’s. Last year, the favorable joblessness margin Switzerland perennially enjoys over Israel narrowed to the smallest gap in history.

Nothing gets the world’s attention more than a robust housing market. The combination of high growth and low unemployment made Israeli homeowners the biggest winners during the past decade, according to the Federal Reserve Bank of Dallas. Housing prices increased 88 percent, the most of any country among the 25 ranked by the bank. No. 2 New Zealand is an also-ran with a 10-year return of 51 percent. Switzerland is a laggard at 39 percent, according to data compiled by Bloomberg.

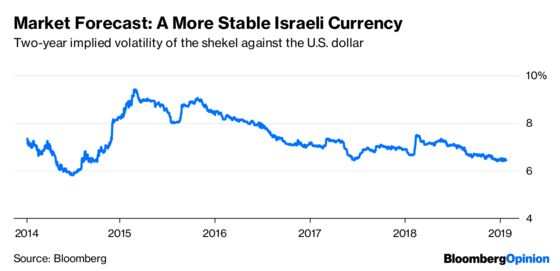

Economies rarely are secure without a strong currency, and the shekel more than holds its own in foreign exchange, strengthening 8 percent against the dollar during the past 10 years as the Swiss franc gained 16 percent and the Euro depreciated 12 percent, according to data compiled by Bloomberg. The perception of Israel in a perpetual existential crisis is belied by the shekel’s two-year implied volatility, a measure of economic uncertainty in the eyes of global investors. At 6.4 percent, it’s hovering at the lowest level since 2014, while the same measure for the euro continues to climb much higher, according to data compiled by Bloomberg.

Investors took a big hit 10 years ago, when MSCI put Israel’s publicly traded companies in the developed world. Overnight, one of the best-performing emerging markets in the new century became untouchable for global investors because of the changed classification. But even that formidable obstacle is gone now that these same companies gained 7.8 percent during the past 12 months, making Israel the second-best performer among 33 major economies as the global equity market was losing 3.3 percent.

Israel can even be said to be as creditworthy as any major economy, including the U.S. Prior to 2014, Israel paid a higher interest rate on its debt — as much as 1.9 percentage points more in 2011 — than any benchmark Treasury. The trend has been reversing since then, and today the yield on benchmark 10-year Israel obligations is 0.55 percentage points less than its U.S. counterpart.

Even in the heat of a fractious nation’s political campaign, the country’s economic performance doesn’t provide much material to argue about.

(With assistance from Shin Pei)

To contact the editor responsible for this story: Jonathan Landman at jlandman4@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew A. Winkler is a Bloomberg Opinion columnist. He is the editor-in-chief emeritus of Bloomberg News.

©2019 Bloomberg L.P.