Is the Market Overreacting or Is the Fed Underreacting?

(Bloomberg Opinion) -- In his press conference this week, Chairman Jerome Powell emphasized that while the Federal Reserve takes financial conditions into account when setting policy, they are only one of many factors it considers. The markets were not pleased. Trending higher before the Fed announcement, they cratered halfway through the press conference and have continued to fall.

Do the markets know something that the Fed doesn’t? Or is this an overreaction, as Treasury Secretary Steven Mnuchin says? As a two-handed economist, my answers are: Yes and no, respectively.

The Fed’s reliance on hard economic data leaves it vulnerable during turning points in the economy. Most of the time, the Fed is correct not to pay attention to the fluctuations in the market, which after all have no real bearing on its mandate (stable prices and low unemployment). As long as the country’s economic fundamentals are sound, the financial markets can do whatever they want.

But that “most of the time” phrase is crucial. The earliest signals that something is wrong in the larger economy come almost exclusively from financial markets. The single most reliable signal — the willingness of lenders to deal with borrowers with even a minimal amount of default risk — may come from the credit markets. These financial measures can move sharply and decisively, providing an early warning of a recession that may be as much as a year away.

By contrast, the real economy has an enormous amount of inertia. When things go bad, they tend to keep going bad for a while. Consider the unemployment rate. Since 1960 it has never trended up for more than a month unless it was just coming out of or about to head into a recession.

So simply monitoring the unemployment rate is of little use in forecasting: Once it became clear that it was heading in the wrong direction, the Fed would not have time to react. To its credit, the Fed has developed forecasting models for major macroeconomic variables — but these, too, tend to adjust slowly in the face of a recession and leave forecasters behind the curve.

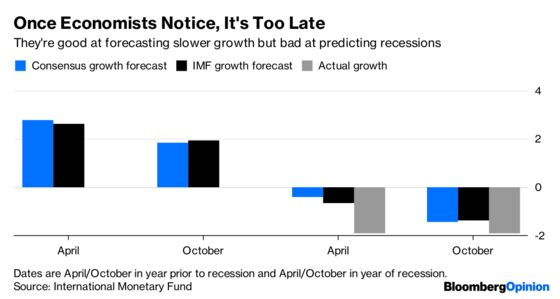

It’s not just the Fed, either. Earlier this year, the International Monetary Fund released a study of recessions in 63 countries from 1992 to 2014. Its authors found that, while forecasters were pretty good at anticipating an economic slowdown, they almost always underestimated its magnitude.

For advanced economies, the average growth in a recession year was about -2 percent. A mere eight months before the recession began, however, the consensus estimate was for 2.8 percent growth, while the IMF’s was 2.6 percent. Three months before the recession hit, the economists downgraded their growth estimates (to 1.85 percent and 1.94 percent, respectively). But they still failed to anticipate the recession.

What does all this have to do with the Fed? Well, in September the median forecast of Fed officials was that growth in 2019 would be 2.5 percent. Now the expected growth rate has been downgraded to 2.3 percent, and this week Powell suggested that officials may mark down their forecasts yet again.

Why exactly forecasters are so bad at seeing recessions is a matter of debate. At any rate, financial markets, by aggregating the knowledge and intuition of lots of participants, seem to do a much better job. That’s why the Fed should pay attention.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a senior fellow at the Niskanen Center and founder of the blog Modeled Behavior.

©2018 Bloomberg L.P.