(Bloomberg Opinion) -- It’s one of the few issues on which Democrats agree with President Donald Trump: America needs to spend more — up to $2 trillion more — to improve its infrastructure. But the bipartisan agreement evident at this week’s meeting between Trump and congressional Democrats soon gave way to arguments over how to come up with the money.

That’s unfortunate, because in the current economic climate, how the federal government spends $2 trillion is more important than how it gets the $2 trillion.

Some background: For decades, economists have decried budget deficits as a drag on the economy and a burden on future generations. Deficits, according to the conventional wisdom, are doubly harmful: They cause increases in both interest rates and taxes.

They raise long-term interest rates by competing against private investments. The more the government borrows, the higher the rate it has to offer to get investors to buy all of its bonds. And since U.S. Treasury bonds are widely considered a safer investment than private bonds, most corporations and financial institutions must then offer even higher interest rates to remain competitive. Increased borrowing costs for everyone lead to less investment and slower growth.

And eventually, of course, the government bonds have to be paid off, requiring an increase in taxes.

The problem with this view is that even as government borrowing has steadily risen over the past two decades, interest rates on long-term U.S. bonds have fallen. Indeed, interest rates are now lower than the growth rate of the U.S. economy.

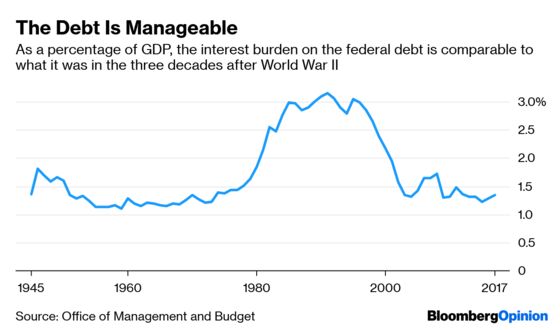

Today’s low interest rates are a product of an aging global society and a demand for safe investments. The result of these low rates is that the U.S. can grow its way out of debt — without raising taxes. That might sound crazy, but there is a historical precedent: After World War II, the U.S. had the largest debt in its history. During the postwar economic boom, however, debt as a percentage of GDP actually fell.

Rising interest rates in the 1980s and ’90s meant that the government no longer had this luxury. It was forced to get serious about deficit reduction, and it did. The surpluses of the late 1990s brought debt back under control.

Since 2000, the economy has been in a position similar to that just after World War II. This time, what makes the debt easier to bear isn’t rapid growth but low interest rates. Still, the effect is the same: The cost of servicing the debt is on par with levels that prevailed after World War II.

The implication is that finding a way to pay for infrastructure spending isn’t crucial. What’s crucial is finding a way to spend the money well. Directing resources toward pet projects or boondoggles, such as California’s failed experiment in high-speed rail, is not the way to go. But it is the nature of politics for there to be disagreements over what constitutes a worthy public project; even a bridge to nowhere starts somewhere.

So the question is how to judge which projects are a wise use of public money. A good rule of thumb is whether spending on any particular project could be better used to increase the child tax credit, which provides much-needed relief to growing families. Support for children is the most fundamental investment a nation can make. Citizens should demand that all public investments meet that standard.

Not all proposed projects will measure up, but some will: effectively addressing the lead-pipe crisis in Flint, Michigan, for example, or rehabilitating dams that are in danger of cracking. Instead of bickering about funding in era of rock-bottom interest rates, the president and members of Congress should be working to identify critical public-works projects.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a former assistant professor of economics at the University of North Carolina's school of government and founder of the blog Modeled Behavior.

©2019 Bloomberg L.P.