If Draghi’s a Currency Manipulator, Then So Is Donald Trump

Draghi shouldn’t make the mistake of engaging with Trump by talking down the euro to counter the president’s words.

(Bloomberg Opinion) -- Mario Draghi has often had to defend the independence of the European Central Bank in the face of attacks from politicians. When Wolfgang Schaeuble, then Germany’s powerful finance minister, accused the central bank of fueling the rise of the extreme right in his country, Draghi hit back quickly: “It is normal for politicians to comment on our actions. But it would be abnormal if we listened to them.”

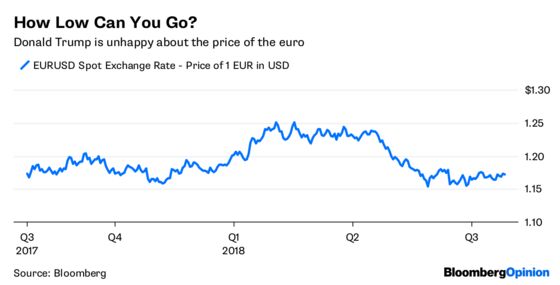

So Draghi will doubtless have something to say to Donald Trump when he meets journalists for his regular press conference on Thursday — and not just congratulating him for Wednesday night’s trade war ceasefire with Jean-Claude Juncker. The U.S. president last week lashed out at the EU, blaming it for manipulating its currency by keeping interest rates low, just as the Federal Reserve is tightening monetary policy. “As usual, not a level playing field,” Trump concluded.

Trump’s tweets contained some basic misunderstanding of the monetary arrangement of the EU. There are multiple currencies in use in the bloc, including for example the Swedish krona and the Hungarian forint. But Trump’s broadside was directed mainly at the euro, the official currency of 19 out of 28 EU states, and hence called into question the actions and independence of the ECB.

The accusations against the ECB of “manipulating” its currency are simply misplaced. Draghi has been at pains to stress that the exchange rate is not a policy instrument of the central bank. This is true of any big central bank in the rich world: Monetary policymakers prefer to discuss currency arrangements at multilateral bodies such as the G-7 or the G-20 to avoid the risk of a currency war.

The ECB sets interest rates and other policy instruments on the basis of its inflation target. The exchange rate is only one of several indirect expressions of its monetary policy. At the moment, the ECB continues to keep interest rates low as underlying inflation remains below its target of “close to, but below” 2 percent. The U.S. recovery is more advanced, which is why the Fed has already started raising borrowing costs. The exchange rate between the euro and the dollar merely reflects these differences in the cycle.

The irony is that President Trump is helping to strengthen the dollar through his own policy choices. For example, tax reform is providing additional stimulus at a time when the U.S. economy is already expanding, giving the Fed good reasons to tighten monetary policy faster than it otherwise would. If the ECB is a currency manipulator, so is Trump.

Furthermore, it’s hard to see the ECB as a stooge of EU politicians. In fact, the problem is the opposite. It is one of the world’s most independent central banks, since it sets its own inflation target as opposed to being given one (as happens, for example, at the Bank of England.) The ECB is often accused of poor political accountability: It answers to the European Parliament, which lacks the weight of national assemblies. The influence of Juncker, president of the European Commission, on Draghi is clearly less than that of Trump on Fed chairman Jerome Powell.

Still, Draghi shouldn’t make the mistake of engaging with Trump by talking down the euro in an attempt to counter the president’s words. One currency warrior in the rich world is just about manageable, even when he’s U.S. president. Add another, and you’re asking for trouble.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns and editorials on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2018 Bloomberg L.P.