How Japan’s Abe Should Spend the Next Three Years

The country still needs to reform its labor market, deal with an aging population, and press for gender equality.

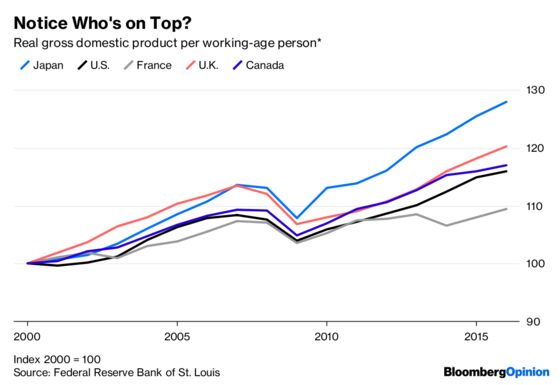

(Bloomberg Opinion) -- Japan’s economy is doing well. Unemployment is at multi-decade lows. Capital expenditure is up, as is return on equity. And wages are finally rising. For the longer-term, Japan also looks strong. Contrary to the popular myth that the country suffered multiple lost decades after the bursting of the bubble economy in about 1990, Japan has outperformed many other rich countries in terms of real gross domestic product per working age population since the year 2000:

It’s small wonder, therefore, that Prime Minister Shinzo Abe was recently chosen to continue to lead the Liberal Democratic Party for another three years. Because the LDP is usually in control of the Japanese government, barring only the occasional rare opposition victory, internal party elections can be more important than general elections. Nationwide, Abe’s approval ratings remain solid. There’s little question that his economic record is the reason he retains popularity.

So what should Abe do in his third term? Bloomberg News’s Isabel Reynolds points out that many of the items on the prime minister’s agenda, including raising the retirement age, delaying social-security payouts, increasing the consumption tax, and revising Japan’s pacifist constitution, will be uphill battles. But this isn’t such a big problem. Interest rates are at or lower than zero and debt-service costs low for the foreseeable future, and raising the consumption tax isn’t urgent. Adjusting social security to compensate for Japan’s aging population will be necessary, but the public and the legislature will likely accede to this necessity after much grumbling.

As for revising the constitution, Bloomberg’s editors are correct when they say that this shouldn’t be a priority. Japan could use a stronger, more flexible armed forces, but Abe has already reinterpreted the constitution to loosen some of the constraints on the military. And the other aspects of constitutional revision would generally take Japan in a more authoritarian direction.

Instead, Abe should focus his efforts on deepening and solidifying the economic resurgence that his policies have helped to jump-start. There are many areas of policy where making improvements doesn’t involve unpopular, painful trade-offs, as in the case of social-security adjustments. By maintaining his push for changes in Japan’s outmoded corporate culture, Abe can continue to improve productivity — the so-called third arrow of Abenomics, along with monetary easing and fiscal stimulus.

Corporate Japan’s most damaged institution is its labor market. A lack of mid-career hiring means that college graduates who fail to get full-time jobs tend to be permanently stuck in low-paid contract work. This also probably damps wages. In the U.S., employees often get raises by moving from company to company, igniting bidding wars, but this strategy is largely unavailable to Japanese workers.

Job immobility also hinders talent from flowing to the places where it can be best utilized, and prevents ideas and tacit knowledge from spreading from company to company. Abe could change this unhappy equilibrium by encouraging the growth of a robust market for hiring experienced workers. Tax cuts or other incentives for hiring of seasoned employees could nudge companies to change. Higher wages and more mid-career hiring would also help Japan attract the kind of skilled immigrants that the Abe administration wants.

A second, even more important area for Abe to focus on is work-life balance. Long, unnecessary hours in the office are a drag on productivity and make it harder for Japanese people to balance family and career, lowering the fertility rate. Cracking down on unpaid overtime is part of the solution, as is a stronger white-collar exemption for overtime rules. Government ministries should also push companies to create a system for tele-work, allowing employees to take some of their work home with them. This will both give Japanese parents more time at home with their kids, and will raise productivity by nudging companies to move to a business model focused on maximizing results rather than labor input.

A complementary policy is to extend Abe’s push for gender equality. Government should step up its policy of awarding contracts preferentially to companies that promote women to management positions. It should also increase the amount of publicly funded day care. One way to do this is to help retirees turn their homes into government-supported day-care centers, which would also help the goal of keeping the elderly in the workforce.

In addition to these structural reforms, there are a number of trade and industrial policies that could help Japan take advantage of emerging opportunities. Japan should continue taking the lead on free trade, pushing for trade deals with rich countries, increasing its investment in South and Southeast Asia, and banding together with other nations to push China to respect intellectual property more. Japan should also expand its effort to take the lead in tech sectors like artificial intelligence and biotechnology, especially by strengthening research partnerships among universities, corporations, venture capital and startups. The government should try to incentivize the creation of accelerators similar to the U.S.’s IndieBio, as well as improving the transfer of technology from universities to companies. Promoting Japan’s entertainment industry would also be a good idea.

So although Abe will face plenty of challenges in his third term as prime minister, there is no reason why he can’t build on the successful strategy he has implemented during the past few years. Japan will need a lot of smart policy-making to stay ahead of the looming challenge of aging. But Abe has shown that it has a fighting chance.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.