(Bloomberg Opinion) -- For hedge funds, 2018 is looking bad, certainly worse than 2013 and perhaps as bad as 2011. According to major indexes, hedge funds in aggregate were up around 1 percent through the first three quarters of the year, only to lose about 3 percent in October, the most in more than five years.

But indexes have issues. They aggregate different types of funds and are dominated by long-short equity funds, which are the largest category and the most volatile. Funds choose whether to report or not, and report on different bases. Valuations can be stale or uncertain. When institutional hedge fund investors report their “alternative” results, these are generally worse than the hedge fund index returns. So, it pays to look at measurements that we can put more faith in to analyze the drivers of hedge fund performance in 2018. These show that only some types of hedge funds are struggling, and for two distinct reasons.

Liquid alts, which are hedge fund strategies run in public mutual fund form, have more reliable data. The chart below shows year-to-date performance by four liquid alts run by AQR Capital Management. These are broadly diversified funds within each category. They won’t match the performance of individual private hedge funds, but they indicate drivers of performance of different type funds.

Arbitrage funds are supposed to generate moderate low-risk returns, and that’s exactly what they’ve done in 2018. Macro is supposed to generate higher returns with more risk, and that’s also worked out. Managed futures have had an up-and-down year, climbing back to near break-even by the end of the third quarter before dropping 5 percent in October. Equity funds have steadily declined since the end of January, a performance made worse by October. These latter two categories seem to be the source of reports of a terrible October for hedge funds.

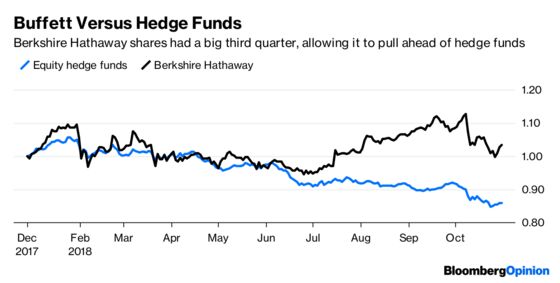

Given that equity hedge funds are the main problem in 2018, it’s worth comparing them to the performance of another equity investor, hedge fund critic Warren Buffett. The charts are similar for the first two quarters of 2018, and also in October, but Buffett managed to make 13.5 percent in the third quarter while equity hedge funds were flat. Despite the difference, it seems reasonable that the main drivers of poor equity 2018 performance are similar.

Investors expect to earn about 4 percent per year from each of these factors, with a volatility of around 8 percent. Robust at just over 2.6 percent is only a little below average, but conservative at negative 8 percent and value at negative 13.1 percent are suffering major downturns. Equity markets have not been kind to sensible value investors this year and Buffett’s excellent third quarter results from some idiosyncratic magic beyond the quant factors.

This gives a more nuanced picture of hedge funds than the indexes suggest. Equity hedge funds drag aggregate performance down, because the things that normally work in the market — value, robust and conservative factors — haven’t worked in 2018. My opinion is that value investing works in the end, and buying solid profitable companies at cheap prices is smart. If they get even cheaper after you buy them, that’s a reason to buy more, not to sell.

More worrisome is that managed futures and similar trend-following strategies have not managed to capture gains even when momentum is strong — in equity markets anyway. While the losses are smaller than in equities, momentum is the opposite of value. If you get a trend wrong, you reverse positions. So if it turns out that you were right the first time and the original trend continues, you lose double instead of making your losses back.

The message for hedge fund investors seems to be that macro and arbitrage funds are doing fine. Equity is going through a rough patch, but if you believe in value and have a long-term horizon, it shouldn’t be a concern. Momentum looks good to an academic, but produces losses in the market, so investors have to take a hard look to figure it out.

These are not perfect proxies for hedge funds. Regulations generally push them to use less leverage and hold more liquid assets. But their positions and performances are transparent, with daily prices based on rigorous methodology (since the funds have to buy and sell shares at these prices, and satisfy the SEC about valuations) as opposed to monthly pro forma figures sent by hedge funds to private data collectors without uniform rules.

“Equity” is AQR Equity Long-Short Mutual Fund; “Arbitrage” is AQR Diversified Arbitrage Fund; “Macro” is AQR Global Macro Fund; “Managed Futures” is AQR Managed Futures Strategy Fund.

These are five sources of excess return identified by Eugene Fama and his long-time collaborator Kenneth French.

They chose not to include this factor in their canonical five.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Aaron Brown is a former Managing Director and Head of Financial Market Research at AQR Capital Management. He is the author of "The Poker Face of Wall Street." He may have a stake in the areas he writes about.

©2018 Bloomberg L.P.