Alphabet Is a Money-Making Mystery But It Works

Investors can take issue with tech giant’s paltry insights into its profitable inner workings, but it is a money-making machine.

(Bloomberg Opinion) -- Investors are getting constant reminders that it's not cheap for tech giants to stay on top.

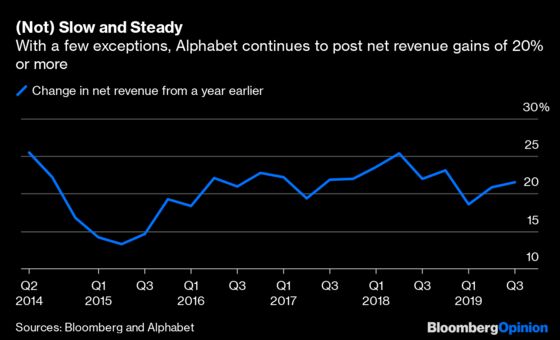

Alphabet Inc. reported on Monday that its third-quarter revenue increased 21.5% from a year earlier, excluding payments to Apple and other partners that carry Google’s ads or funnel web-search traffic to the company. This continued the company's nearly uninterrupted trend of quarterly sales gains of 20% or more — a notable accomplishment for a company with more than $125 billion in yearly revenue.

As was true with fellow tech superpower Amazon last week, Alphabet's expenditures are growing at an even faster pace than its sales. Operating costs increased by 27% from a year ago, the steepest increase in years. The disclosure about Alphabet’s spending seems to have contributed to a slight decline in the company’s share price in after-market trading.

Where is Google’s parent company directing all that spending? Well, the company doesn't say specifically, but it has numerous research and development costs — think engineers and other investments in everything from Google's cloud-computing operation to artificial intelligence technology and consumer hardware development labs. Google also picked up its outlays on capital projects such as computer centers and real estate after a bit of a breather in the first half of the year.

As with Amazon, investors have to make an assessment about whether Google's investments are justified. Mostly, it's hard to quibble with the company's track record of turning spending into product changes large and small that generate sales, and (potentially) projects that might become Google's next big thing.

The trouble with Alphabet is always transparency. The company doesn’t provide outsiders much insight on either what is perking up revenue at the company, or where all of its spending is going. That makes it tough to assess the return on the company’s investments.

Google, for example, has dropped loads of cash on buying companies that make hardware — in recent years it picked up engineering and design teams of smartphone company HTC for more than $1 billion and purchased home-device makers Nest and Dropcom — and reportedly recently made an offer to buy the fitness tracking gadget maker Fitbit Inc. Yet if Google has a coherent strategy for all its hardware projects, it hasn't articulated it.

Investors can justifiably take issue with Alphabet’s paltry insights into its money-making machine, but it is a money-making machine. That is mostly through constant tiny tweaks to its web-search service and other products such as YouTube, and perennially advancing options for companies to pay Google to find customers.

Much of this work isn’t the type of awe-inspiring technology advances that grab headlines, but it is Google’s magic. Investors for now have to look at the continued healthy sales gains as vague proof that whatever is happening under Google’s hood will continue to dazzle.

This excludes Alphabet's cost of revenue.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.