Forget the FAANGs. Pay Attention to the Highflying PUTINs.

(Bloomberg Opinion) -- Those of us who write about technology and financial markets spent a good chunk of last year chronicling the ups and downs of FAANG stocks (or FAAMGs), the awful acronyms for a handful of successful U.S. tech companies.

So far in 2019, the shares of tech superstars and U.S. market indexes in general are higher with relatively modest valuations —based on what investors are willing to pay for each dollar of profit.

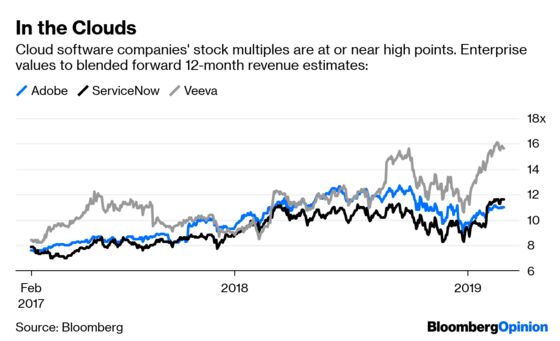

With far less notice, however, a category of typically fast-growing cloud software firms have stretched their valuations so far that they’re vulnerable to a meltdown. If you’re looking for a bubble, this might be it.

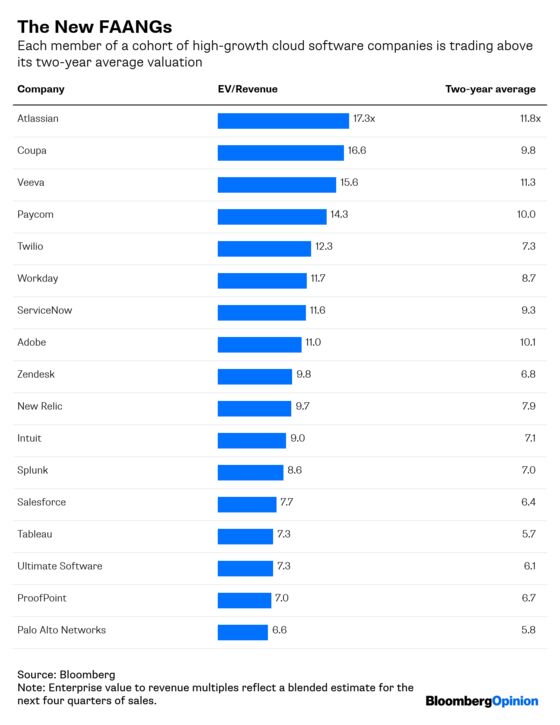

I looked at a selection of 17 top cloud companies such as Salesforce.com Inc., Atlassian Corp. and Workday Inc., and each one is trading above its average valuation over two years, according to Bloomberg data. Stock buyers are paying 9.8 times each dollar of the companies’ expected revenue in the next 12 months, based on the median of my cloud cohort. The median over two years is 7.3.

Analysts also expect the companies’ sales growth to slow, which means investors are generally paying more for less oomph from these companies.

The only thing missing is a terrible acronym. How about VAZSAW, for Veeva Systems Inc., Atlassian, Zendesk Inc., Salesforce, Adobe Inc. and Workday Inc? Or PUTIN — Palo Alto Networks Inc., Ultimate Software Group Inc., Twilio Inc., Intuit Inc. and New Relic Inc.?

Investors’ willingness to pay top dollar for highflying software firms shows that stock buyers are desperate to get into tech growth areas and don’t care much about the cost of entry.

That may be bad news for the health of the stock market or those individual cloud companies if they can’t grow fast enough to match expectations. On the other hand, investors’ eagerness is good for Slack Technologies Inc., Palantir Technologies Inc. and other business software startups that want to go public soon.

A good example is Atlassian, which makes software such as Jira and Confluence used by developers and IT departments. It’s typically one of the most expensive stocks — and for good reason. Atlassian’s revenue in its fiscal year ended in June 2018 rose 41 percent, and on average analysts expect a 36 percent jump in the current fiscal year.

That fast growth goes a long way to explaining why a tech company your friends and neighbors has never heard of is worth more than Kroger Co. despite having less than 1 percent of the supermarket chain’s sales. And Atlassian’s stock is getting pricier as growth eases off. The company’s market value after accounting for its cash and debt is about 17 times Atlassian’s expected revenue in the next 12 months. That’s the highest price since the company went public in 2015, Bloomberg data show, and about three times more expensive than Google parent Alphabet Inc.

Those kinds of stratospheric cloud share prices increase the chance of a stock crash if the companies falter. We got a glimpse of that Wednesday when Box Inc.’s forecast for quarterly revenue fell short of Wall Street estimates, and the shares cratered. More broadly, Bloomberg Intelligence analysts cautioned this week that above-average company valuations and a potential slowdown in global software spending later this year may lead valuation multiples to shrink.

This isn’t new territory. The high-growth, richly valued cloud software firms tend to swing in value more drastically than older, slower-growth companies. It happened in early 2014, in early 2016 and again last fall. And most of the time they come back stronger than ever. Or a stock swoon will compel some companies to sell themselves.

The share price of human-resources software company Workday, for example, fell 40 percent in the early 2014 downturn for highflying young companies, again lost 40 percent of its value in the 2016 hiccup and more than 20 percent in about six weeks last fall. Its share price hit a record high on Wednesday, and it is seven times the price at which Workday went public in 2012. (Facebook is four times its 2012 IPO share price.)

The increasing cost of cloud software firms will not and should not prompt the hand-wringing that accompanied the FAANGs dominating the stock market. Cloud software firms are relative specks compared with the tech superstars. That doesn’t mean, however, that there won’t be pain if and when they fall from the stratosphere.

I selected these companies because they have relatively high market values ($5 billion or more)and are generally well regarded by investors. A broader cohort of cloud software stocks, the BVP Nasdaq Emerging Cloud Index, has an enterprise value to revenue multiple of 11 times.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.