Federal Reserve Forward Guidance Is Alive and Well

(Bloomberg Opinion) -- The Federal Reserve has failed in its efforts to reduce the amount of forward guidance it provides. In the wake of the market turbulence that followed the December Federal Open Market Committee meeting and Chairman Jerome Powell’s press conference, policy makers have essentially abandoned efforts to wean market participants off forward guidance.

To be sure, the guidance has shifted from the FOMC statement to public appearances, but it is forward guidance nonetheless. The new keyword is “patient,” and it clearly means the Fed is on hold for the time being.

Central bankers began setting the stage to make forward guidance less explicit in mid-2018. Federal Reserve Bank of New York President John Williams prophesied last May that forward guidance would be deemphasized in favor of a renewed emphasis on communicating the Fed’s reaction function. Powell echoed those thoughts later that month. By September, Williams claimed that “explicit forward guidance about the future path of policy will no longer be appropriate.”

The Fed soon learned, however, that this was easier said than done. Following a turbulent period for the stock market in the final months of 2018, explicit forward guidance has made a comeback. As a result, the most important word in the Fed’s lexicon is now “patient.” See, for example, this from Powell’s interview last week. Or this from Vice Chairman Richard Clarida. Or this from Federal Reserve Bank of Boston President Eric Rosengren.

It’s clear that the Fed is sending a coordinated message that policy makers think an extended pause is more likely than not. In other words, forward guidance is alive and well. While central bankers may try to claim they have ended forward guidance because it comes via public appearances rather than the FOMC statement, this is a distinction without a difference.

Why did the Fed need to revert to more explicit forward guidance before they even had much of a chance to pull back into a more uncertain policy framework? I think the Fed’s efforts over the years to provide more information has actually increased the need for coordination of that information and as a consequence the need for forward guidance.

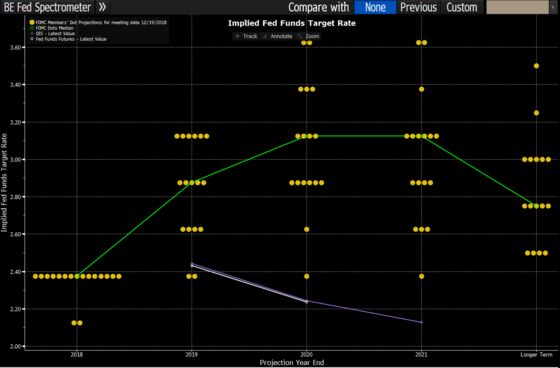

Consider the forecast contained within the Summary of Economic Projections, including the “dot plot” of interest rate projections. The Fed doesn’t want us to focus on those interest rate projections as a pre-determined policy path. Instead, the Fed wants us to think of the forecasts as illustrations of its reaction function. In this light, the path provided by the median economic projections is only one of many possible paths.

That said, the economic projections highlight the median forecasts, implying that those forecasts have some special significance even though the Fed bristles at such an implication because there are no official FOMC forecasts. Combine those forecasts with the FOMC statement, which relates that policy makers judge further rate hikes will be needed. Add in the numerous policy speeches claiming that the Fed needs to act preemptively to contain inflation.

Mix these communication elements together and it is easy to conclude that the Fed intends to boost rates twice in 2019 and those hikes need to be front loaded in order to be preemptive. This is a fairly hawkish takeaway, especially given the mood of financial market participants in December.

A different reading of that information might be that given inflation is expected to remain under control, and with only two rather than the earlier three rate hikes expected in 2019, there is no rush to tighten further with policy rates are at the lower end of neutral estimates. The Fed can afford to be patient, and that means they don’t have to decide about a rate hike until the middle of the year. This is obviously the more dovish takeaway. Eventually, the Fed realized they needed a coordinated effort to lead market participants to this interpretation.

Try as they might, the Fed won’t be able to easily rid themselves of explicit forward guidance. If not delivered in the FOMC statement, policy makers will likely need to deliver that guidance via public appearances. They need the forward guidance to act as a coordinating force across all the various elements of their communication strategy. That forward guidance now tells us that barring a dramatic shift in the data, the Fed doesn’t feel compelled to decide about the next rate hike anytime soon.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2019 Bloomberg L.P.