Fed Teases Bond Traders With Inflation Talk

To the market’s chagrin, Fed policy makers may actually mean it when they say they want to be patient.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg Opinion) -- The minutes after the release of the Federal Reserve’s interest-rate decision had all the looks of another dovish surprise from the world’s most important central bank.

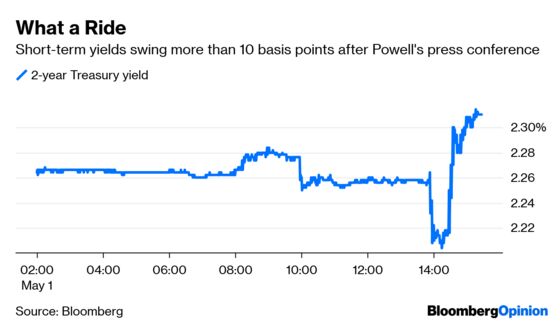

While the Fed left its benchmark lending rate unchanged, it dropped the interest paid on excess reserves by five basis points to 2.35 percent. Even though that cut was largely for technical reasons, it sparked a rally in short-dated U.S. Treasuries, with two-year yields tumbling by as much as six basis points. Even more importantly for the economic outlook, the Federal Open Market Committee’s statement tweaked language around inflation relative to its previous meeting:

March: On a 12-month basis, overall inflation has declined, largely as a result of lower energy prices; inflation for items other than food and energy remains near 2 percent.

May: On a 12-month basis, overall inflation and inflation for items other than food and energy have declined and are running below 2 percent.

On its face, this is clearly dovish. It’s no secret that stubbornly low inflation is vexing policy makers, with Fed Chair Jerome Powell calling it “one of the major challenges of our time.” It stands to reason that observed inflation running “below” rather than “near” 2 percent could compel officials to ease. He had a chance to follow up on that during his press conference — and chose to strike a decidedly more hawkish tone, at least relative to market expectations.

“We expect that some transitory factors may be at work. Thus, our baseline view remains that with a strong job market and continued growth, inflation will return to 2 percent over time, and then be roughly symmetric around our long-term objective.”

This is basically the Fed’s conventional thinking, and at past meetings it would be little more than a throwaway line. But bond traders built up expectations that policy makers would be willing to take unconventional measures to boost inflation. Specifically, some central bankers brought up the idea of insurance rate cuts in the face of price growth running persistently below 2 percent. That’s why fed funds futures were pricing in almost a full quarter-point cut by year-end.

Those bets changed in a hurry, with two-year yields rising 10 basis points from their session lows.

It seems increasingly clear that bond traders went too far in pricing in a Fed interest-rate cut so soon. Why? Simply put, policy makers mean it when they say they want to be patient. During the press conference, Powell was vigilant to dodge questions that tried to get him to define a threshold that would justify lowering rates.

One exchange stood out in particular, with Nancy Marshall-Genzer, a reporter at Marketplace. Powell had said if low inflation didn’t prove transitory, the Fed would have to “take it into account.” She asked: “How specifically would you take that into account?” Powell wouldn’t give a direct answer, only saying “There are many variables to be taken into account at any given time.”

“So cutting interest rates would be…” she began, before Powell interjected with “I can’t really be any more specific than what I’ve said,” and gave a forced smile.

Bond traders may have to force some smiles too after withstanding the Treasury market’s price swings. The yield curve whipsawed from steeper to flatter, reflecting that swift reversal in expectations about imminent Fed cuts. Of course, nothing from Powell suggested the Fed was going to raise rates, either, but two-year yields were briefly trading below the lower bound of the fed funds rate. That’s obviously mispriced for a central bank that’s resolutely holding policy steady.

Recent commentary from Fed officials, and even the language in the FOMC statement, was little more than a tease for markets. Ultimately, this sounds like the same old central bank that will dismiss below-target inflation as long as the economy is growing and the labor market is strengthening. The Fed may have a dual mandate, but Powell won’t let perfect be the enemy of good.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.