(Bloomberg Opinion) -- Macroeconomics is getting interesting again. For the past five years, monetary policy was simple and boring — the economy was recovering steadily, but not yet at full employment, and inflation remained muted, so the Federal Reserve simply had to keep interest rates low and not interfere with a good thing.

But now this happy era of tranquility may be ending. The number of prime-age Americans with jobs — probably the most accurate measure of the labor market — is approaching its pre-recession peak:

This number probably understates the degree of the recovery, since there has been aging within this group, which makes even prime-age people a bit less likely to work. Other indicators of the labor market also show a return to health.

That raises the question of whether it’s time to raise interest rates. Standard thinking says that a tight labor market leads to inflationary pressure. Workers have more purchasing power, leading them to buy more; that creates more demand for workers, raising wages, while also raising prices. This is known as the wage-price spiral, and something like this idea is lurking in the background of most macroeconomic analyses. The idea was advanced by the legendary macroeconomist Milton Friedman in the form of a so-called accelerationist Phillips curve — a mathematical relationship stating that when unemployment goes below its so-called natural rate, inflation accelerates out of control.

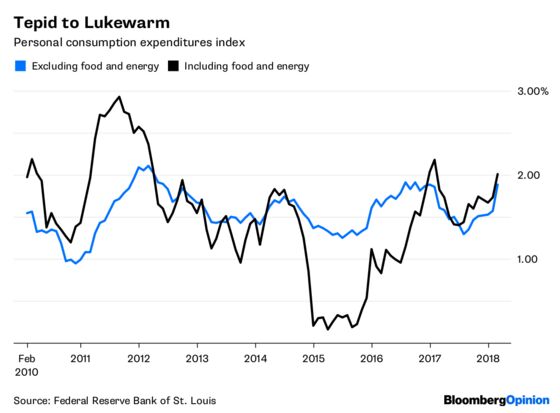

Both wages and prices have increased at faster rates in the past two years. Inflation, whether including volatile food and energy prices or stripping them out, is approaching the Fed’s target level of 2 percent:

The growth of workers’ compensation accelerated in 2017 and was even higher in the first quarter of 2018:

Wage growth, meanwhile, although consistently higher in 2016, is still running at about 3 percent a year:

If you focus on total compensation rather than just wages, and if you look only at the past few months of data, it’s possible to see the beginnings of a wage-price spiral. That would imply a need for interest rate increases, to keep price and wage growth steady and measured. And this is what the Federal Reserve is doing — Fed Chairman Jerome Powell has declared the central bank’s intent to continue increasing rates at a deliberate pace.

But there are reasons for caution. As Paul Krugman points out, the spiral hasn’t been in evidence in recent decades.

Wage growth has indeed accelerated as the prime-age employment-to-population ratio recovered since early 2014. That part of the theory looks fine. But price inflation hasn’t followed. As wage growth has climbed, prices have continued to increase at a steady rate of about 1.5 percent — less than the Fed’s 2 percent target. Except perhaps for the last few months, there has been no acceleration in prices.

That’s good news for workers, since it means that real wages have been rising (albeit only slowly). But it’s bad news for the Friedmanian theory of inflation. If a tightening labor market causes prices to explode out of control, it must only happen when employment levels get very high.

So it makes sense for the Fed to go easy on the rate hikes. Core inflation has barely reached its target, and not in any sustained fashion. As long as consumer prices are not increasing all that fast, the Fed shouldn’t consider rising wages to be a danger sign. In fact, tightening in response to accelerating wages while inflation is still roughly constant risks turning monetary policy into a tool of wage suppression — it seems like a bad idea for the Fed to put on the brakes every time wages outstrip prices.

In the meantime, policy makers and macroeconomic analysts should rethink the basic mental model that they use to evaluate the state of the economy. Because rising wages don’t seem to trigger a wage-price spiral — or at least, not at moderate levels of wage growth — much of the conventional wisdom about the root causes of inflation is probably wrong. The failure of the accelerationist Phillips curve to match reality during the past few years means that prices don’t behave the way many experts in industry and government instinctively expect them to. If those experts keep relying on the conventional wisdom imparted from the 1970s and 1980s, big mistakes could result.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

©2018 Bloomberg L.P.