(Bloomberg Opinion) -- Federal Reserve officials meet Thursday to discuss monetary policy, and while no one expects the central bank to boost interest rates at this time, there's sure to be a lot of interest in how they address the recent turbulence in financial markets in light of their Goldilocks-like outlook for the economy. In other words, something has to give.

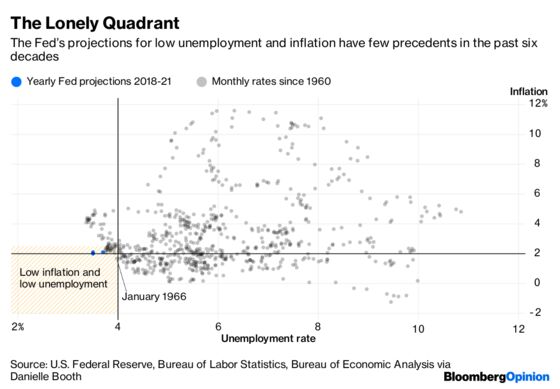

The minutes of Fed's Sept. 25-26 meeting revealed that a cadre of Federal Open Market Committee members advocated for pushing the federal funds rate, currently in a range of 2 percent to 2.25 percent, to beyond what is considered a neutral level into territory that restricts economic growth. Fed Chairman Jerome Powell puts the neutral rate somewhere in the neighborhood of 3 percent. That's predicated on the unemployment rate staying below 4 percent through 2021 and inflation remaining at an idyllic 2.1 percent level.

Goldilocks herself would blush at such a near perfect scenario. Consider that January 1966 is the only month since 1960 that unemployment has been below 4 percent with inflation being south of 2 percent. The Fed’s projections out through 2021 do not simply suggest we will go there but that we will stay there for an awfully long time. Such fairy tales would accomplish something: they would fill the empty quadrant that has but that sole occupant at the moment.

We have had a protracted period of well-behaved inflation, thanks to the deflation China exported around the world by way of its less expensive goods, technological advances that depressed prices and, of course, the extraordinary exertions of monetary policymaking in the post-Greenspan era. Precedent also exists for the unemployment rate staying below 4 percent for four years – it happened in the 1960s. But that episode was also accompanied by a functioning Phillips curve, with the inflation rate rising from a starting point of 2 percent to 5 percent.

While no straight line can be drawn between cause and effect, investors have been a bit agitated about the prospect for much higher rates since Powell nodded to how rarified the economic air is, noting that it would almost seem to be “too good to be true.” For good measure, he added that “better monetary policy has played a central role” in creating this picture perfect backdrop. Well, yes, $22 trillion in global quantitative easing goes a long way.

In return, we have financial markets worldwide suffocating as that liquidity is withdrawn and there are precious few places to hide. As Bloomberg News reported of a recent JPMorgan Chase & Co. strategy piece, one-in-five asset classes have positive returns this year with every market aside from the Nasdaq Composite Index, U.S. leveraged loans and commodities underperforming cash.

And yet, most investors will continue to hope for the best, which is emblematic of late cycle behavior. How else would it be possible to have 83 percent of companies filing to raise money via initial public offerings not generating profits? According to research undertaken by the University of Florida finance professor Jay Ritter, the proportion of unprofitable IPOs surpass that of the prior peak of 81 percent in 2000 just as the Nasdaq was tipping into crash territory.

The major difference between then and now is we have the Fed in a double-tightening mode, raising interest rates and shrinking its balance sheet assets, just as other major central banks begin a shift to tighter monetary policies -- or at least less accommodative policies. That's removing liquidity from the global financial system.

It all kind of makes you stop and wonder exactly where U.S. stocks would be absent 2018’s forecasted $1 trillion in share buybacks. The only question is whether anyone inside the Fed has woken to that same realization and with it the recognition that the empty quadrant is not apt to be filled in the coming years.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Danielle DiMartino Booth, a former adviser to the president of the Dallas Fed, is the author of "Fed Up: An Insider's Take on Why the Federal Reserve Is Bad for America," and founder of Quill Intelligence.

©2018 Bloomberg L.P.