(Bloomberg Opinion) -- The Federal Reserve gave markets what they wanted on Wednesday by leaving its main interest rate unchanged and continuing to pledge patience to see how the U.S. economy responds to a global slowdown. Stocks and bonds initially rallied and the dollar weakened. All positive developments. Then Jerome Powell started speaking.

Markets quickly reversed as the Fed chair said the current low rates of inflation are likely “transitory” in nature and that the central bank doesn’t see a strong case for moving rates down or up. The reason that rattled markets so much is because bond traders have priced in about a 65 percent chance that the Fed would cut rates this year, given that inflation remains so stubbornly low. Those relatively high odds have underpinned this year’s big rally in equities. And if the Fed is less inclined to cut rates because it sees inflation rebounding, then that’s bullish for the dollar – which isn’t necessarily a good thing for stocks, as a stronger greenback has the potential to make U.S. exports less competitive at a time when global trade volumes are falling at the fastest pace since the depths of the financial crisis. Beyond that, there is another reason why markets were likely rattled, and it has to do with Powell’s communication skills. He has made some notable gaffes in his time as head of the Fed, most notably in December when he said that the federal funds rate was still a long ways away from a neutral level. Those comments spurred concern that the Fed was out of touch given how signs were already emerging that the global economy was decelerating and markets were in turmoil. Powell’s comments Wednesday during his press conference that low inflation rates are likely transitory don’t exactly jibe with the growing consensus that inflation is low for structural reasons. Breakeven rates on Treasuries — a measure of what bond traders expect the rate of inflation to be over the life of the securities — suggest the market doesn’t see inflation meeting the Fed’s 2 percent target anytime over the next decade.

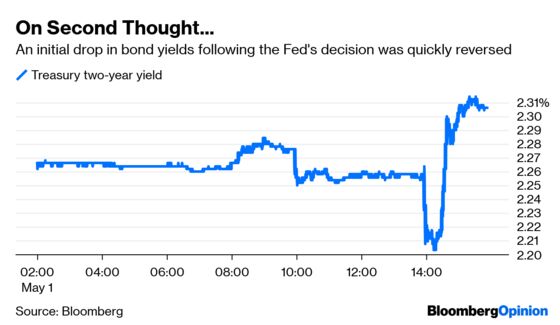

A predictable central bank is one of the underappreciated hallmarks of a strong, stable market. After all, there's little room for surprise when the Fed is telling you what it's going to do, when it’s going to it and by how much. The problem now is that no one can be sure what the Fed will do, when it will do it and by how much. “Overplayed narratives often lead to extremes in investor sentiment,” the strategists at Cantor Fitzgerald wrote in a research note before the Fed decision. “Extreme sentiment may reverse quickly alongside a change in the narrative.” No wonder the yield on the benchmark two-year Treasury note went from falling by about six basis points to 2.20 percent to rising four basis points to 2.31 percent.

DOLLAR DILEMMA

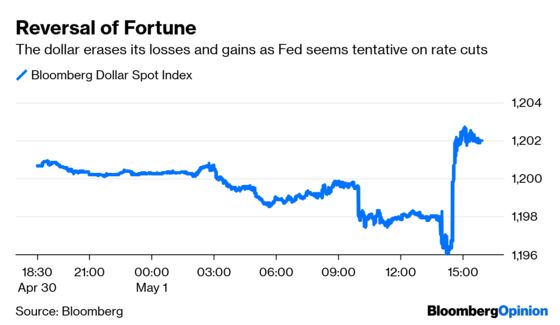

Of all the market moves, perhaps the most concerning was the rebound in the dollar. Like Treasury yields, the Bloomberg Dollar Spot Index initially fell on the initial headlines from the Fed’s decision, dropping as much as 0.3 percent, only to reverse those losses and surge as much as 0.26 percent when Powell started speaking. Of course, there are many benefits to a strong dollar. For one, it provides an incentive for foreign investors to own U.S. financial assets such as stocks, bonds and real estate. But there’s a downside, too, in that it makes U.S. goods less competitive at a time when the global economy is decelerating. In other words, foreign buyers may feel less inclined to buy relatively expensive American products. That could act as a drag on U.S. economic growth as well as corporate earnings. S&P Global Ratings figures that 30 percent of the revenue of S&P 500 companies comes from outside the U.S. Jodie Gunzberg, managing director and head of U.S. equities at S&P Dow Jones Indices, calculated that the S&P 500 rises 3.7 times more from a falling dollar than a rising one. And over the past 12 months, the Bloomberg Dollar Spot Index is up more than 4 percent. The greenback is also the strongest performer over that time among a basket of 10-developed market currencies that includes the euro, yen and pound. Besides the smaller odds of a rate cut, the prospects for a stronger dollar help explain the S&P 500’s reversal from being up 0.28 percent to falling 0.75 percent on the day.

EURO BORROWING BINGE

It’s been a good year for euro-area bonds, with the Bloomberg Barclays Euro Aggregate Bond Index rising 2.63 percent. That tops the 1.90 percent gain in the broader Bloomberg Barclays Global Aggregate Index. But now, the euro region’s outperformance will face a stiff test in May, with governments slated to see more bonds than any month since 2014. Citigroup Inc. forecasts gross issuance of 89 billion euros ($99.6 billion) this month, or 15 billion euros higher than the monthly average forecast for the year. The net cash requirement totals about 53 billion euros. That figure represents the amount of new cash being raised, rather than just selling bonds to refinance older ones coming due. The net cash requirement is highest in Germany, Italy and Spain. The good news is that there’s a growing belief that Europe’s economy has bottomed and is starting to improve, which may help lure foreign investors to the region’s bonds if they feel the euro will rally as well. The pace of growth in the euro region doubled in the first quarter to 0.4 percent compared with the final three months of 2018, amid a surge in Spain, resilience in France and a rebound in Italy. “A pick up in euro-area GDP growth in 1Q will finally give the European Central Bank reason to cheer,” Bloomberg Intelligence senior economist David Powell wrote in a research note. “The data suggests the drag on the region’s economy from country-specific shocks is dissipating and the long-awaited reversion to trend may finally be underway.”

SAUDI STOCKS TAKE FLIGHT

Saudi Arabia may be somewhat of a pariah on the global geopolitical scene for its role in the killing of Washington Post columnist Jamal Khashoggi, but the global investment community sure doesn’t mind. The kingdom had no trouble selling $10 billion of bonds in Saudi Aramaco, the world’s largest oil company, and now its stock market is starting to pull away from the pack. A recent spurt of gains has pushed the benchmark Tadawul All Share Index’s return this year to 19.6 percent, compared with 12.1 percent for the MSCI All-Country World Index. As recently as late March, the returns for the two indexes were similar at about 10.4 percent. Along with rising oil prices, the demand for the Aramco bond sale surely put to ease any concerns investors might have had in investing in Saudi Arabia. Goldman Sachs Group Inc.’s David Solomon last month became the first head of a global U.S. bank known to have traveled to the country since an international furor erupted last year over the murder of Khashoggi. It also helps that the first stage of Saudi Arabia’s entrance into MSCI’s benchmark emerging-markets index starts this month. JPMorgan Chase & Co. estimates the inclusion may lead to $15 billion of flows into the kingdom’s stock market. The iShares MSCI Saudi Arabia exchange-traded fund has had 10 consecutive weeks of inflows.

COPPER CRUMBLES

The optimists can no longer ignore the signals being sent by copper. The metal, which has a reputation for being a great leading indicator for the global economy given its wide use, got crushed on Wednesday, falling as much as 3.48 percent in its biggest decline since August. Prices are now at their lowest since mid-February. Recall that when the metal was rallying in January and February, many said it was proof that talk of a global synchronized slowdown — and even an imminent recession — were overdone. Well, maybe a global recession isn’t imminent, but it’s hard to argue that the worldwide economy isn’t decelerating. The Institute for Supply Management said Tuesday that its manufacturing index for April fell to the weakest level since 2016. Three of five index components declined: new orders, employment and production. Plus, China’s first official gauge of the manufacturing sector in April fell, while industrial production also tumbled in South Korea and Japan, and gross domestic product growth slowed a notch in Taiwan. The report came a day after top copper producer Codelco said it plans to restart some operations at its Chuquicamata smelter in northern Chile after a four-month stoppage, a move that will add to global supplies.

TEA LEAVES

Just because the Fed’s two-day meeting ended on Wednesday doesn’t mean central bank watchers can take the rest of the week off. Up next is the Bank of England, which wraps up its monetary policy meeting on Tuesday. Although JPMorgan, Citigroup and Toronto Dominion Bank are among some banks that see the possibility of a hawkish signal following the recent six-month extension the U.K. was granted from the European Union for carrying out its Brexit plan, that seems to be a long shot with so many major central banks going in the opposite direction. BOE policy makers “will inevitably sound a little less dovish, but not dramatically,” the economists at Bank of America wrote in a research note Wednesday. So why are some economists even thinking that the BOE may diverge from its peers? It’s because the U.K. economy is in relatively good shape. While the economic data globally is falling below estimates by the greatest degree since early 2016, the data in the U.K. has exceeded forecasts by the greatest degree in two years, according to Citigroup’s economic surprise indexes.

DON’T MISS

Milken Conference Trades Rainbows for Clouds: Stephen Gandel

Europe's Rebound Shows Draghi Got it Right: Ferdinando Giugliano

Companies Should Value Workers Like Shareholders: Raghuram Rajan

How Foreigners Helped Cool Australian Housing: David Fickling

Matt Levine's Money Stuff: People Want to Buy Uber Stock

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.