China Makes Its Presence Felt at the Fed, Quietly

China is the principal factor behind the the Fed’s pivot, even if it wasn’t mentioned directly in the latest policy statement.

(Bloomberg Opinion) -- China has gone from a boon to world growth to a source of fragility. The policy response, driven mainly by Beijing and the Federal Reserve, is likely to be equally global in nature.

The Fed took a big step on this front Wednesday, scrapping a preference to hike interest rates, citing global economic and financial conditions and waning price pressures. The principal worry is China and the weakness and deflationary pressures it’s exporting. China isn’t mentioned directly in the Federal Open Market Committee’s statement; it’s there in all but name.

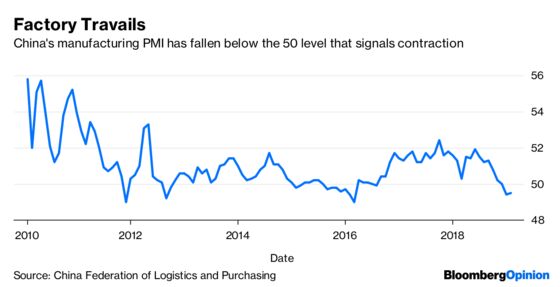

Slackening conditions are seen in a raft of manufacturing and trade measures, especially but not exclusively in Asia. More bad news came Thursday with a gauge of Chinese manufacturing again showing a contraction. South Korea's factory sentiment number, released earlier in the week, tumbled.

The emerging policy result, chiefly in the monetary arena, maps out as a long pause or tilt toward easing from the Fed, European Central Bank and Bank of Japan. In China itself, officials have undertaken about 60 easing steps since the middle of last year, according to Cornerstone Macro LLC.

Unlike an open-slather cut in interest rates such as the ones China unleashed from 2014 to 2015, these have been targeted at striking at least some kind of balance between stimulus and debt sustainability. Lately, they have erred more on the side of stimulus. They’re not exclusively monetary, either, encompassing tax cuts, lender reserve relaxation and so on. They do add up.

Outside China this means greater attentiveness in central bank statements to “global” factors, which seems like a euphemism for Asia’s biggest economy. Just look at the Fed's evolving use of the word: The Federal Open Market Committee's abandoning of “some further gradual increases” in favor of mere “adjustments,” was preceded by the clause “in light of global economic and financial developments and muted inflation pressures.'” (I wrote here in December about how the term has figured in Fed verbiage over the years.)

A look at the FOMC's previous statement shows a stark contrast. On Dec. 19, the Fed said it would “continue to monitor global economic and financial” conditions. In the space of about six weeks, this has gone from something relatively passive to almost a justifying clause. And what's being justified is a big shift, an effective declaration that rate cuts are just as possible as hikes.

Monetary fraternities are reluctant to openly criticize each other or be seen to finger fellow members of the club. Sure, Brexit (sigh) and Italy often come up in remarks, but given China contributes about 27 percent of global growth, make no mistake about what's really important.

These steps don't appear to be the product of some secret accord. This isn’t a 2008-style crisis; more like policy responding to some shared concerns.

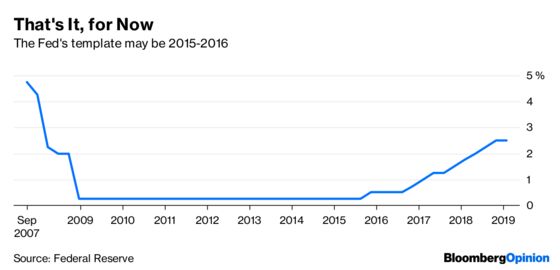

The 2015 and 2016 period is more instructive because there are signs we are replicating it: China is easing and conditions are pushing the Fed to shelve rate hikes that had been penciled in only last month. The Fed went into both 2015 and 2016 projecting four increases apiece. It eked out one each, in December of both years. Fed Chair Jerome Powell has spoken, almost with nostalgia, about the risk management during that period.

Don't central banks have domestic mandates? Of course. They also have come to see more clearly that what happens in China ricochets through the commercial life of their home country.

China’s woes could slice world growth to 2.3 percent, according to Oxford Economics, the slowest since the financial crisis and in the territory generally defined as a global recession. The IMF reckons that red line is about 2.5 percent.

For context, latest IMF numbers project growth of 3.5 percent this year and 3.6 percent in 2020. We are quite a distance from the precipice.

Central banks, however their stances are presented, want to keep the ship from steering close to the edge.

Fed chair Jerome Powell did mention China, fleetingly, in the 47-minute press conference that followed the FOMC statement. The session was dominated by questions about the Fed's balance sheet, the government shutdown and the perception among investors that there's now a ``Powell Put.''

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.