(Bloomberg Opinion) -- Over the past two and half years, the Federal Reserve has consistently underestimated how low unemployment could fall before sparking an increase in inflation. As a result, the Fed began raising interest rates sooner than was necessary — leading to slower economic growth and fewer jobs.

How many fewer? Research by Adam Ozimek, senior economist for Moody’s Analytics Inc., suggests that the economy would have created up to 1 million more jobs in the last few years.

Before getting into the details, it may be helpful to look at the big picture. Even in the best of times, some unemployment is inevitable. In a dynamic economy, there will always be some companies laying off workers as others are struggling to hire more. This churn in employment, combined with the entrance of new workers into the labor force, means that at any given time some percentage of workers will be looking for a job but won’t have one.

Macroeconomists call this percentage the long-term natural rate of unemployment. Standard economic theory suggests that unemployment can fall below this level only temporarily: The shrinking pool of workers means growing companies will have to raise wages. As the competition for workers intensifies, wages will increase faster than productivity growth. Profit margins will shrink, and businesses will raise prices to make up the difference. This will cause the rate of inflation to rise, eroding the initial wage gains. What had initially seemed like good news for workers will turn into a Red Queen’s race between wages and prices. People are no better off as either workers or consumers.

To prevent all this from happening, the Federal Reserve strives to slow down the economy as unemployment falls close to its long-term natural rate. Which is certainly a sensible goal, but for one problem: Economists don’t know exactly what that rate is.

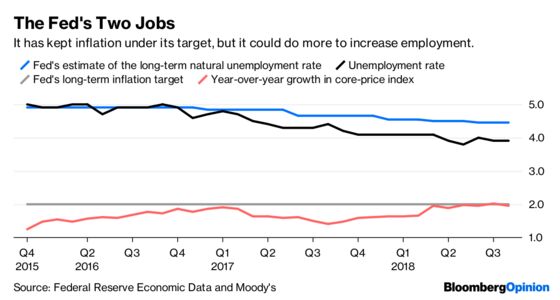

Now back to the matter at hand. In March 2015, when the Fed first began raising rates, the unemployment rate was 5 percent. At the time, the Fed’s estimate of the natural rate of unemployment was 4.9 percent. Even if the rate dipped a little below this, the bank said, it would be OK because inflation was also below its 2 percent target. So Fed settled on a gradual series of rate increases to slow the economy enough so that inflation would wind around the target.

Since that time, however, unemployment has continued to fall — and inflation has remained low. There are various theories as to why. I have suggested that the Great Recession was so severe it caused millions of workers to give up looking for jobs. As a result, they were not counted as unemployed. Thus the potential pool of workers was — indeed still is — greater than the unemployment statistics suggest.

At any rate, the Fed has acknowledged that its estimates of the natural rate were too high. In June, the Fed revised its estimate to 4.45 percent. The unemployment rate at that time was 3.9 percent, and since then has fallen to 3.7 percent. Nonetheless, inflation pressures seem mild.

Even assuming that the Fed’s current estimate of the natural rate of unemployment is correct — and it seems high — the series of rate hikes that it began in March is premature. Ozimek estimates that had the Fed believed the natural rate was 4.45 percent all along, it would not have raised rates until June 2017, resulting in stronger job growth and roughly 500,000 more workers today.

And yet, given the continued mild inflation, the possibility exists that the Fed is still overestimating the natural rate of unemployment. Suppose that June’s unemployment rate of 3.9 percent is the true natural rate. In that case, Ozimek estimates that the Fed should not have begun raising rates until March of this year. Had the Fed followed that course, Ozimek estimates that 1 million more people would be employed than are today.

But don’t let this speculation obscure the main point: The Fed’s premature rate increases have almost certainly reduced job growth.

The economy is performing exceptionally strong right now, in response to an oil and gas boom and the stimulus associated with the tax reform. If the Fed continues on its current path of rate hikes, it may be setting itself up for tepid growth and disinflation once those effects wear off. That combination is particularly hard on borrowers and makes the economy vulnerable to a financial shock.

By revising its estimate of the natural rate of unemployment , the Fed has implicitly acknowledged that its current series of rate hikes began too soon. Future revisions may well reveal that it ended too late.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a senior fellow at the Niskanen Center and founder of the blog Modeled Behavior.

©2018 Bloomberg L.P.