Traders Party, But Just Wait for the Hangover

Fed is parroting the sentiment of ECB President Draghi, who last week noted a growing downside risk to the economy.

(Bloomberg Opinion) -- Talk about a knee-jerk reaction. Global stocks soared, with the S&P 500 Index rising as much as 1.91 percent, after the Federal Reserve did a 180-degree turn away from the bias it expressed just last month toward higher borrowing costs. It now promises to be “patient” on any future interest-rate moves. The thinking now is the Fed won’t cause a recession by tightening monetary policy too much. Fair enough, but there’s still the issue of a global slowdown that the U.S. is unlikely to avoid, which the Fed seems to now acknowledge.

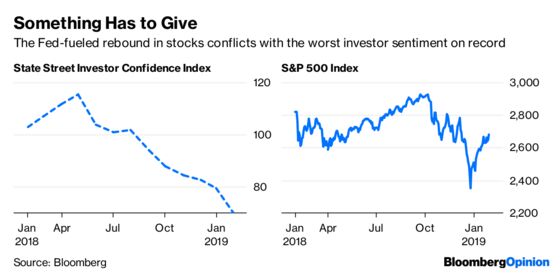

In essence, the Fed is parroting the sentiment of European Central Bank President Mario Draghi, who last week noted a growing downside risk to the economy. Also last week, the International Monetary Fund cut its global growth forecast for the second time in three months, predicting the world economy will expand at the weakest pace in three years in 2019. S&P Global Ratings said in late November that it saw a not inconsequential 15 percent to 20 percent chance of a recession this year, up from its prior forecast of 10 percent to 15 percent. In that sense, Wednesday’s action could be described as more of a relief rally than any newfound confidence in equities after last quarter’s gut-wrenching sell-off. At least that’s what the smart money is signaling. Consider State Street Global Markets’ monthly index of global institutional investor confidence. Released this week, it plunged to a record 70.2 for January from 79.8 for December, which was the previous low — lower than even than during the financial crisis. The measure has some authority because unlike survey-based gauges, it’s based on actual trades and covers 15 percent of the world’s tradeable assets.

The Fed’s actions are “very supportive for risk assets — at least in the short term,” Putri Pascualy, a managing director and partner at Paamco, which manages about $10 billion, wrote in a research note Wednesday. “The backdrop of slowing economic growth on a global basis is the 800 (pound) gorilla in the room.”

THE BOND MARKET TELLS THE REAL STORY

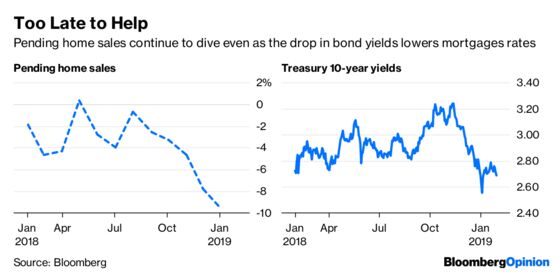

And if everyone really believed that a more dovish Fed would save the economy, then the logical thing would be for bonds to weaken — but they didn’t. Most U.S. Treasuries rallied. That’s not so unusual for very short-dated notes, which are most sensitive to changes in Fed policy. What was more surprising was that longer-term notes participated in the gains, with 10-year yields dipping back below 2.70 percent. As recently as November, those yields were flirting with 3.25 percent. But in a sign of the challenges facing the U.S. economy, the National Association of Realtors said earlier on Wednesday that contract signings to purchase previously owned homes unexpectedly fell for the third straight month in December despite the recent drop in mortgage rates. The organization’s index of pending home sales was down 9.5 percent from a year earlier, the worst drop since early 2014. That followed a report Tuesday from the Conference Board, which said its index of consumer confidence for January showed the biggest two-month decline since 2008, falling 16.2 points over the course of December and January.

THE DOLLAR’S DROP HAS A SILVER LINING

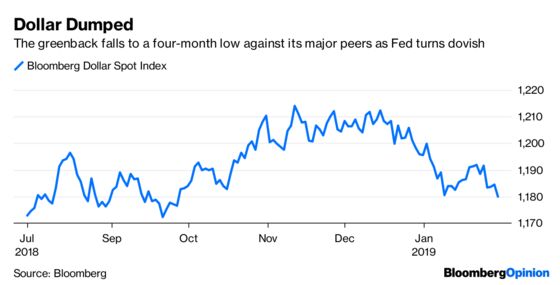

Dollar traders didn’t take the Fed’s dovishness very well. They pushed the Bloomberg Dollar Spot Index to a four-month low. There’s less reason to own greenbacks if the Fed is done raising interest rates for now. About the only major currency the dollar wasn’t down against was Mexico’s peso. The silver lining here is that a weaker dollar should help make U.S. exports more competitive, which would support the economy and underpin corporate earnings. S&P Global Ratings figures that 30 percent of the revenue of S&P 500 companies comes from outside the U.S. Jodie Gunzberg, managing director and head of U.S. equities at S&P Dow Jones Indices, wrote in a blog post in May that the S&P 500 rises 3.7 times more from a falling dollar than a rising one. So, all else being equal, a weaker greenback is a serious tailwind. But the currency market is a zero-sum game, which means if the dollar is falling, then other currencies are rising. The euro, yen, Canadian dollar and even the beleaguered British pound appreciated against the U.S. currency on Wednesday.

TURKEY’S CENTRAL BANK GROWS A SPINE

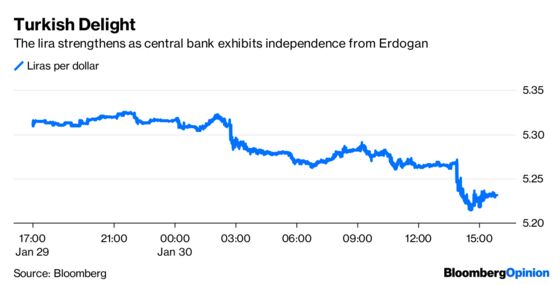

The Turkish lira had a horrible 2018, depreciating 28 percent as President Recep Tayyip Erdogan hounded the central bank to cut rates even though it should be doing the opposite. Given moves by Erdogan to gain greater control over economic matters, currency traders figured it was only a matter of time before the central bank caved, throwing the Turkish economy into further turmoil. But now, it looks as if the central bank is looking to make a statement about its independence. The lira was the best-performing currency in the world for most of the day on Wednesday, strengthening about 1.50 percent, after the Monetary Policy Committee barely tinkered with its projections for inflation and signaled it remains reluctant to cut borrowing costs, according to Bloomberg News’s Cagan Koc and Onur Ant. “The central bank deserves credit for publishing an inflation report which is market-friendly,” Rabobank strategist Piotr Matys told Bloomberg News. The lira is one of the more widely traded currencies in emerging markets, and rising investor confidence in Turkey’s central bank should be good for the assets of developing markets overall. The rally in the lira helped propel the MSCI EM Currency Index to its highest level since June.

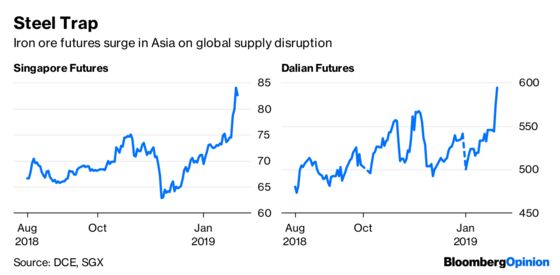

IRON ORE STEALS THE COMMODITIES SPOTLIGHT

There are a lot of unhappy steel executives in the world. That’s because the market for iron ore is going haywire after a deadly accident at a Brazil mine run by Vale SA, the world’s No. 1 producer of the key ingredient used in making steel. Vale said it will halt the use of all upstream method dams over three years, a process that will cut production from the sites by 40 million tons a year. The company had planned to mine 400 million tons this year, according to Bloomberg News’s Krystal Chia. As a result, benchmark futures on Singapore Exchange Ltd. jumped as much as 9.6 percent to $86.20 a ton, the highest since March 2017. This wouldn’t be much of a problem if the global economy were humming along nicely, allowing steel producers to pass along the rising cost of iron ore, but it isn’t. So, profit margins are likely to get squeezed. It’s no secret that global economic growth is slowing, with both the International Monetary Fund and World Bank lowering their forecasts. Probably the only thing keeping iron ore from rising even more is that China, the biggest consumer of iron ore, is looking sickly. Of the 30 Chinese provinces that have released their 2019 growth targets, 23 lowered their goals from those set for 2018, Bloomberg News reports, citing local government work reports.

TEA LEAVES

After last week’s monetary policy meeting, the ECB’s normally optimistic Draghi expressed some pessimism over the outlook for the economy. He said economic risks had moved to the downside, a marked a change from six weeks earlier, when he had described the risks as “broadly balanced.” He’s right. Data on Thursday is forecast to show that the euro-zone economy grew just 0.2 percent in the fourth quarter, the same as in the prior three-month period and matching the lowest rate of growth since 2014. As Bloomberg Economics Chief European Economist Jamie Murray noted in a research report, that’s “below the rate needed to keep unemployment and inflation stable in the medium term.” “Expect big downgrades in March when fresh forecasts are published,” Murray said in reference to the pending ECB estimates for growth and inflation. That likely means the ECB won’t be able to back off from its quantitative easing measures as expected, which should weigh on the euro and help push the region’s government bond yields even lower, as hard to believe as that may seem.

DON’T MISS

The Fed Is Officially at the Market’s Mercy Now: Brian Chappatta

Game Theory Says Don't Bet Against a No-Deal: Leonid Bershidsky

Watershed Looms for China's $11 Trillion Bond Market: Shuli Ren

Matt Levine's Money Stuff: If You Want to Invest in Pot, Buy POT

A New Venezuela Can Avoid the Oil Curse: Ellen R. Wald

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.