There’s No Pleasing the Stock Market If You’re the Fed

(Bloomberg Opinion) -- It’s clear that no matter what the Federal Reserve and Chairman Jerome Powell did and said at the final monetary policy meeting of the year, they couldn’t make stock investors happy. Despite the Fed doing what had been expected, which was boosting interest rates for the fourth time this year and cutting its 2019 forecast to two hikes from three, the S&P 500 went from being up as much as 1.54 percent to down as much 2.25 percent.

The Fed’s decision should have been good news for stocks, as any more of a dovish tilt would have raised concern that the Fed sees the economy deteriorating much faster than thought. East West Investment Management Co. market strategist Kevin Muir captured the zeitgeist in a blog post before the Fed’s statement when he wrote that “the market has talked itself into believing the Fed will err on being dovish, so the bar has been raised for Powell’s performance.” Perhaps, but the reality is that the equities market has been on a steady decline since early October and the path of least resistance, especially with the year rapidly coming to an end, is lower. What we know is that the stock market is poised to set its low for the year in December for only the sixth time in the past 91 years. When that happens, stocks are typically either in a long-term downtrend for a large part of the year or break violently lower in December, according to Bianco Research. This is significant because when this happened in the past, the following year was not a good one for equities. Recessions occurred in four of the five subsequent years and stock returns “were nothing short of a disaster,” according to Bianco, with losses averaging 18.4 percent. The lone exception to a recession was 1941, when the Pearl Harbor attack caused the market to drop to a new low that December. While 1942 did not experience a recession, stock returns suffered for the first half of the year before rebounding to end 12.4 percent higher.

The point to all this is that while it may be a cliché to say that markets overshoot and react, it doesn’t mean they are wrong. And while the folks at Bianco note that there are too few examples of stocks hitting their lows for the year in December to be statistically significant, “we would argue there is still a message to be gleaned.”

THE BOND BULL MARKET LIVES

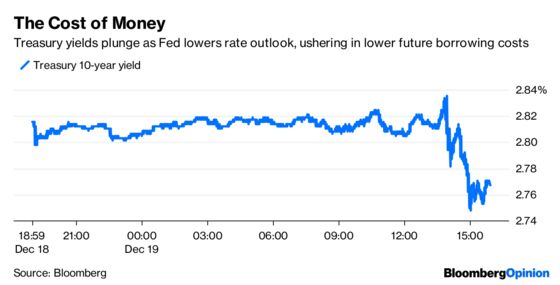

At least bond traders are happy. The news that the Fed pared the number of expected rate increases next year to two from three and trimmed its inflation forecast sent prices of U.S. Treasuries soaring. That pushed the yield on the benchmark 10-year note down almost 6 basis points to 2.76 percent, which is the lowest in eight months. Recall that just last month, the yield was floating around 3.25 percent. What all this means is that the long-anticipated bear market in bonds has been put on hold. Even before Wednesday’s gains, the Bloomberg Barclays U.S. Treasury Index was up 0.10 percent for the year through Tuesday, looking to avoid its first annual loss since 2013. The drop in market rates is helping to offset some of the sting of higher policy rates. The average 30-year U.S. mortgage rate has dropped to 4.63 percent from 4.94 percent in early November, a move that should provide some support to the all-important housing market. Earlier Wednesday, the National Association of Realtors said sales of previously owned homes rose for a second consecutive month in November, exceeding forecasts and suggesting consumer demand is picking up as price gains moderated amid rising mortgage rates between August and November. Still, the gains in U.S. government debt aren’t likely to prevent the global bond market from ending the year lower. The benchmark Bloomberg Barclays Global Aggregate Bond Index was down 2.11 for the year, which could give companies less of an incentive to raise debt financing to expand and invest.

THE OTHER DOLLAR STORY

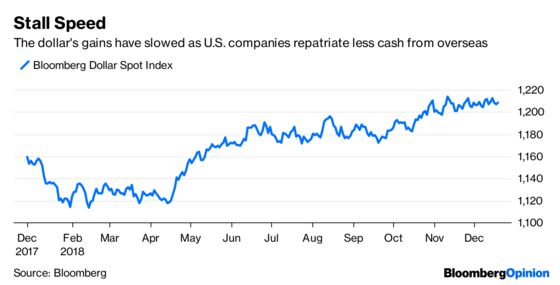

The Bloomberg Dollar Spot Index, which measures the greenback against a basket of its main peers, posted a small increase Wednesday despite a dovish Fed, bringing its gain for the year to about 4.20 percent. President Donald Trump has cited the dollar’s strength as a reason the Fed should stop raising interest rates because higher rates tend to attract foreign capital to a currency. But that debate has tended to mask what looks to be a primary driver of the dollar this year: repatriation. Tracking the currency’s performance this year shows that the bulk of its gains came in the first half of the year, when the amount of offshore cash corporations brought back to the U.S. under the new tax laws soared to $478.6 billion. The pace slowed significantly in the third quarter to $92.7 billion, according to data released Wednesday by the Commerce Department. It just so happens that the Bloomberg Dollar Index’s rise stalled in the second half of 2018. The economists at Morgan Stanley wrote in a report that they now expect a total of about $650 billion to be repatriated this year, short of the $1 trillion that many expected. The impact goes beyond the dollar. The strategists at JPMorgan wrote in a recent report that the slower pace of repatriation could result in fewer stock buybacks by companies, further weighing on equities.

GOLD STARTS TO SHINE

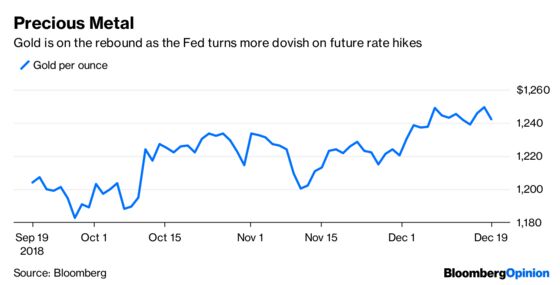

The price of gold rose to its highest since July on Wednesday, topping $1,260 an ounce before easing back in late trading. The rise from this year’s low of less than $1,175 in August has a lot to do with the worsening global economic outlook. It also has a lot do with the Fed. Because gold pays no interest, its appeal diminishes when rates are rising, and that’s why bullion had tumbled from almost $1,400 as recently as April. But now that the Fed has sent some dovish signals, bullion’s appeal has been rising. The latest weekly data from the U.S. Commodity Futures Trading Commission released late Friday showed that money managers’ bullish bets on the precious metal outnumbered their bearish wagers for the first time in five months. The consensus in a Bloomberg survey of 20 analysts and traders is for gold prices to increase to $1,325 by the end of next year. Almost all respondents said they were bullish, according to Bloomberg News’s Ranjeetha Pakiam, Susanne Barton and Rupert Rowling. Of course, that means there’s a lot of pain ahead for the global economy and markets. But on the bright side, probably not the amount of pain during the euro debt crisis of 2011 and 2012, when gold prices topped out at $1,900 an ounce.

RUSSIAN BONDS REJECTED

The ruble was in the emerging-market spotlight Wednesday as the currency erased its decline on news that the Trump administration is ready to remove sanctions on Russian billionaire Oleg Deripaska’s aluminum company, United Co. Rusal, after he reached an agreement to significantly reduce his ownership stake. Rather than offer relief, the ruble’s rebound only serves to underscore how awful it has performed this year, depreciating about 14 percent. That compares with a decline of about 4 percent in the MSCI Emerging Markets Currency Index. The sanctions have certainly weighed on the ruble along with the drop in oil prices. Economists surveyed by Bloomberg see Russia’s economy expanding by just 1.6 percent this year and 1.5 percent in 2019. The outlook for Russian financial assets is so bad that the government on Wednesday canceled a planned bond auction for the first time in almost three months. The auction of 10 billion rubles ($148 million) of notes maturing in February 2024 was canceled due to a lack of acceptable bids, the Finance Ministry said in a website statement. Earlier this month, longtime Russia investor Ashmore Group Plc said it was trimming its holdings of local assets because their indefinite exposure to sanctions amounts to a “slow-moving train wreck,” according to Bloomberg News’s Áine Quinn and Olga Voitova.

TEA LEAVES

The most anticipated Fed meeting in recent memory is over, but that doesn’t mean that investors can tune out for the year. Thursday promises to be a bonanza for central bank watchers, with policy makers in Japan, the U.K., Sweden and Mexico set to announce policy decisions. Neither the Bank of Japan nor the Bank of England are expected to tweak their rates or policies, but as usual their language will be parsed closely. All 49 economists surveyed by Bloomberg see the BOJ keeping its policy settings untouched, but many have pushed back their expectations of when the bank might join its global peers in normalizing policy given the mounting economic risks. The recent economic data in the U.K. has been overshadowed by the Brexit talks, with Prime Minister Theresa May struggling to avoid exiting the European Union without a deal in March. Sweden’s Riksbank may or may not raise rates, with 10 of the 24 economists surveyed by Bloomberg expecting policy makers to add a quarter percentage point to the benchmark repo rate, bringing it to minus 0.25 percent. The rest predict that the Riksbank will wait. In Mexico, the central bank is likely to maintain interest rates at 8 percent with a hawkish bias, according to Bloomberg Economics.

DON’T MISS

Stocks Face Obstacle No Matter What Fed Does: Stephen Gandel

Markets Join Trump in Pleading for Fed to Stop: Brian Chappatta

Why Economics Has Trouble With the Big Problems: Noah Smith

What Game Theory Says About Brexit Choices: Mohamed A. El-Erian

India’s Shadow-Bank Risks Put China in the Shade: Andy Mukherjee

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.