Facebook’s Libra May Spark a Currency War

What if Facebook’s crypto, backed by fiat-currency assets, over time becomes people’s preferred store of wealth?

(Bloomberg Opinion) -- It's one thing for academics in Asia to rant against the tyranny of the dollar, or to make cheery forecasts about its impending eclipse by the Chinese yuan. But now that Facebook Inc. wants to spawn a new global currency – one that could meet the “daily financial needs of billions of people” and perhaps rival the greenback one day – central banks in Beijing, Jakarta, Manila or Mumbai won't exactly be ecstatic.

To them, the prospect of being at the mercy of a cabal of tech czars and venture capitalists sitting in Switzerland could well mean swapping the yoke of the U.S. Federal Reserve for a less predictable and potentially more sinister dependence.

What if Facebook's crypto, backed by fiat-currency assets and offering stable value, starts out by paying for coffee but over time becomes people's preferred store of wealth? What will it mean for monetary sovereignty? Suppose users of Libra, as the currency will be called, manage to set aside their outsize privacy concerns with Facebook. Were the tokens to take off and – against all regulatory odds at home and abroad – gain global acceptance, there will be several implications for governments around the world.

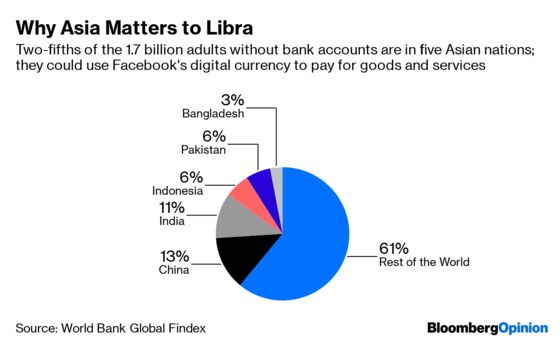

Some of them will be of particular concern in Asia, where most of the larger economies, starting with China, yearn for a growing role for their currencies in international commerce and as a store of value. Americans enjoy everything a little cheaper because the world – including money launderers, drug dealers and terrorists – wants the U.S. currency, which only the Fed can manufacture. China wants the same privilege for itself; and in a decade or two, India and Indonesia will, too. However, the long, patient game of internationalizing the yuan would get complicated if the Chinese on the mainland themselves take to Libra to bypass the country’s increasingly invasive social scoring system.

Shielded by capital controls, Asian central banks at times seek weaker currencies to stimulate their export-led economies. But if people can move their wealth with one scan of a QR code to a digital coin backed by a reserve of low-risk assets – including bank deposits in various currencies and U.S. Treasuries – such stratagems won’t work any more. The People's Bank of China could then respond with its own digital currency, and unlike Facebook, pay interest on it. Other central banks may join the battle for continued relevance. This competition, and not devaluation, could end up becoming the real currency war of the 21st century.

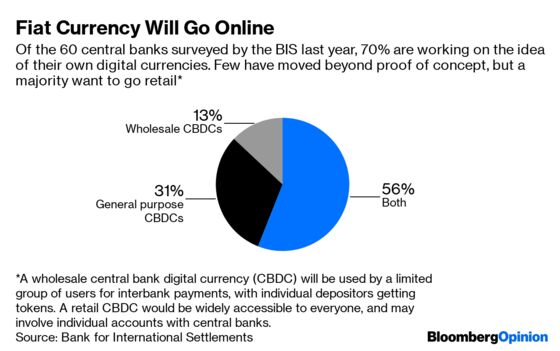

None of us has experienced a central bank-sponsored digital currency yet: Our online payments are mediated by commercial banks or fintech. But it’s not a far-fetched idea. Seventy percent of the monetary authorities surveyed by the Bank for International Settlements last year said they’re working on the concept. So far they’ve had no reason to take the leap. Central banks already make digital cash available to financial institutions. Those are called bank reserves. Presumably, the Switzerland-based Libra Association, which will also include Visa Inc., Uber Technologies Inc., venture capitalist Andreessen Horowitz and other founders apart from Facebook, will also rely on a “geographically distributed network of custodians” to tap this closed user group for reserves.

Nothing stops a central bank from providing its own digital tokens via commercial banks to compete with Facebook. If that doesn’t do the trick, the monetary authority can pull the ultimate stunt: It can open up its balance sheet to the public. Groups like the U.K.-based Positive Money, which is advocating for “Britcoin” to be held by individuals directly with the Bank of England, see it as the ultimate antidote to “extractive middlemen like banks and now tech companies.” Such a step would carry risks. In normal times, commercial banks can retain customer deposits by paying higher interest. But when panic strikes, deposits might flee to the central bank, even if the latter imposes a negative interest rate. Monetary authorities don’t want a funding shock to their banking systems. However, were Facebook to pose an existential threat, they may be compelled to walk an untrodden path.

New purchasing power will increasingly come from Asia and Africa where the demographics are still favorable for high income growth. To the extent that global tech avoids paying national taxes when this purchasing power turns into digital consumption, it’s already a headache. Were Libra or another such project backed by the technology industry to take over where the dollar leaves off, concerns around a fair share of taxes could multiply. For that reason alone, Libra may not end up going anywhere in Asia.

The Libra Association will use its income to pay operating expenses, and then to compensate early investors in the consortium.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.