(Bloomberg Opinion) -- Europe’s leaders are engaged in a high-stakes standoff with Italy, trying to coerce the populist government to drop its budget-busting spending plan. But how far can they go? Can they risk pushing Italy out of the currency union?

Judging from the exposures of French and German banks, they have a strong incentive to seek a compromise.

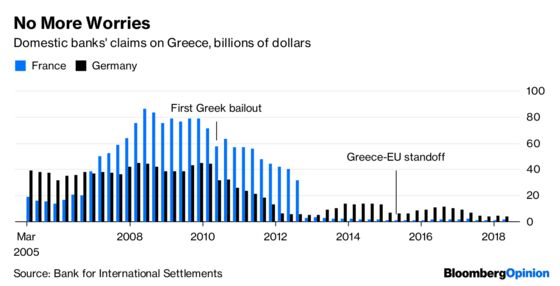

Looking at what banks are up to can be useful in understanding the behavior of France and Germany, the euro area’s two most influential members. When, for example, revelations of Greece’s fiscal mismanagement triggered a crisis in 2010, French and German banks were holding about $115 billion in various Greek investments, according to the Bank for International Settlements. This gave their governments ample reason to offer Greece the financial lifeline it needed to survive. But five years later, when a new left-wing government tried to rebel against the austerity they had imposed, their exposures had dwindled to less than $8 billion — and they proved much more willing to let Greece go to the brink.

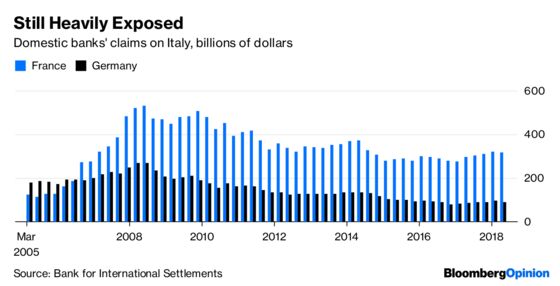

So how much do the banks have at stake in Italy? A lot. As of June, French institutions had some $316 billion in Italian investments, according to the BIS. That’s much more than they ever had in Greece. German banks’ claims on Italy, at $91 billion, were smaller but still significant.

Italy’s plan to increase the budget deficit to 2.4 percent of gross domestic product represents a threat to the banks, because it undermines government bond prices and weakens Italian counterparties. But a deadlock that ultimately pushed Italy out of the currency union would be much worse, sharply devaluing all the banks’ Italian holdings. Probably the best outcome is a truce that allows Italy to do a bit of stimulus in return for a credible promise to be more frugal in the longer term.

Of course, keeping banks afloat isn’t the only reason to want Italy to stay in the euro. The exit of continental Europe’s third-largest economy would threaten the currency union’s very existence. But in trying to guess what Europe’s leaders might do, it’s helpful to know where the money is.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Whitehouse writes editorials on global economics and finance for Bloomberg Opinion. He covered economics for the Wall Street Journal and served as deputy bureau chief in London. He was founding managing editor of Vedomosti, a Russian-language business daily.

©2018 Bloomberg L.P.