It’s Still a Man’s World at Hyundai

Proxy advisers ISS and Glass Lewis just dealt a blow to corporate governance reform in South Korea, @anjani_trivedi writes.

(Bloomberg Opinion) -- Shame. One of the world’s biggest investors and some of the most influential proxy advisory firms just stuck another nail in the coffin of corporate governance reform in South Korea.

The country’s National Pension Service, which is advised by Korea Corporate Governance Service, will vote against proposals for dividend payout and board changes at Hyundai group put forward by activist investor Paul Singer’s Elliott Management Corp. The fund holds the single largest stakes in Hyundai Motor Co. and Hyundai Mobis Co. after units of the conglomerate.

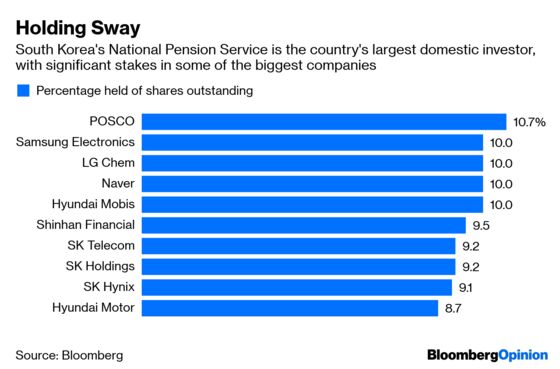

A vote in favor of Elliott would have been largely symbolic. Even so, the fund decided to take the path of least resistance — despite having voluntarily signed up to the country’s newly minted Stewardship Code last year. The pension service, with 8.7 percent of Hyundai Motor and 10 percent of Mobis, is a significant voice. It holds between 5 percent and 12 percent of nine-tenths of companies on the Kospi 200 index. So much for being more active, or at least vocal, over voting and shareholder rights.

Elliott’s proposal would have put the Hyundai companies on par with international peers, an objective the group has set for itself. The U.S. investor is seeking to expand the size of the Hyundai Mobis board to 11 from nine by adding more outside directors. In theory, a more diverse and independent slate of directors should help improve oversight. The Hyundai Mobis board in its current form is all-male and mostly Korean, with a limited range of experience. There’s also significant overlap with current management.

Meanwhile, proxy advisory firms Glass Lewis & Co. and Institutional Shareholder Services Inc., having initially urged investors to vote against Hyundai’s own restructuring proposal, are dilly-dallying. The firms guide shareholders on how to vote and command significant sway, with billions of dollars following their recommendations. The U.S. Securities and Exchange Commission is expected to propose the first set of U.S. rules on such companies as early as this spring. ISS and Glass Lewis have a 97 percent market share.

The Hyundai plan lacked business logic in parts and was designed to benefit the founding family, Glass Lewis said last year. Yet, while acknowledging deficiencies at the auto company pointed out by the U.S. hedge fund, the firm recommended shareholders vote against Elliott’s proposal. It called Hyundai’s moves to nominate three new external directors “governance enhancements.”

At Hyundai Motor, ISS advised shareholders to vote against Margaret S. Billson, the only female nominee for the board. Billson, a heavy-hitter in industrial manufacturing, was rejected because her predominantly aviation-related experience wasn’t deemed relevant. ISS plumped instead for the company’s candidate, investment banker Chi-Won Yoon. While qualified in his field, Yoon doesn’t have significant experience as an outside director or in industrial manufacturing. Hyundai Motor’s board is currently filled with management, academics or government officials.

There’s more than a whiff of hypocrisy to ISS’s stance. The advisory firm has talked up gender diversity, quoting studies on the business advantages of recruiting more female leaders. Late last year, ISS unveiled its new proxy voting guidelines in the U.S., with a focus on board gender diversity. Starting next year, the policy says the adviser will generally recommend voting against the nominating committee chair if there are no women on a company’s board.

Glass Lewis said Hyundai Motor’s three board recommendations — Yoon, a professor and a retired buy-side analyst — were more suitable than Elliott’s candidates. It also recommended against a one-time dividend payout in favor of the company investing in research and development, and potential mergers and acquisitions, given the current state of the auto industry. Again, though, it noted that “it remains to be seen whether the company will generate sufficient returns on such spending.” The adviser even went on to say that a large return of capital to shareholders might “prove more beneficial.”

The trouble is that Hyundai needs deep surgical changes, as we’ve written, not more spending with limited or no returns in the foreseeable future.

Sure, there were a few victories for Elliott, with proxies agreeing on some nominees, but not enough to force meaningful change on Hyundai ahead of a shareholders’ meeting this Friday.

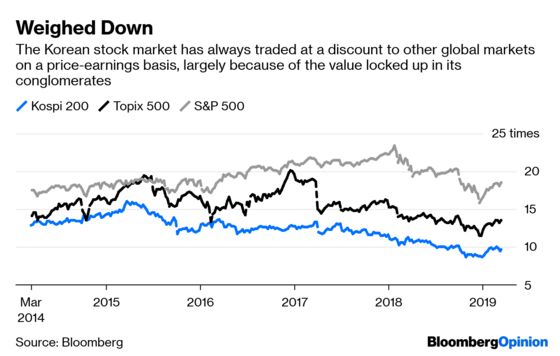

A united front would have helped push the seemingly indomitable chaebol to open up, setting an example for others and holding out the prospect of higher returns in a market that’s weighed down by the power of entrenched interests. Instead, the pension fund and proxy firms just strengthened the status quo.

ISS's new 2019 proxy voting guidelines are effective Feb. 1, 2019. But on the issue of board diversity, where it announced a new voting policy, the adviser is giving companies a one-year grace period until Feb. 1, 2020, given the current lack of gender diversity.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.