(Bloomberg Opinion) -- The antitrust movement is making a comeback. Zephyr Teachout, candidate for New York state attorney general, is promising to fight monopolies. Activists such as Matt Stoller of the Open Market Institute are beginning to draw attention to the problem of concentrated market power. Think tanks like the Washington Center for Equitable Growth are starting to zero in on the issue as well. The revival of this movement is still in its infancy, and certainly hasn’t reached anything approaching the fervor of the Progressive Era a century ago. But the new antitrust crusaders are experiencing a tailwind from an unlikely ally -- the economics profession.

In the past, economists have not exactly crowned themselves with glory in the fight to keep big business from getting too big. Some have made a bomb of money offering their services as consultants to companies looking to execute megamergers. The so-called Chicago School of antitrust analysis, popularized during the mid-20th century, dismissed the dangers of market concentration except in the case of explicit price-fixing or outright domination of a market by a single company. This school of thought heavily influenced the burgeoning movement to integrate law and economics, leading to looser antitrust enforcement in the 1980s and afterward.

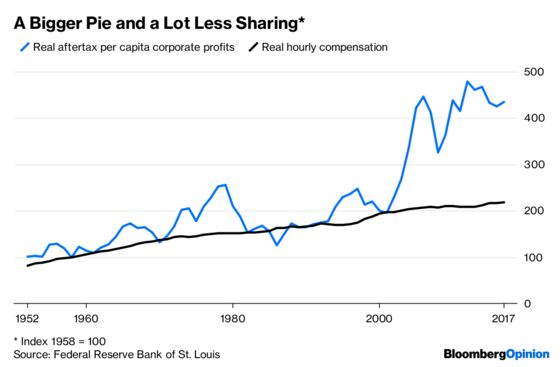

But in the past few years, economists have become increasingly concerned with the problem of stagnating wages. Profits have grown strongly since the turn of the century, but real wages -- even including health and retirement benefits -- have risen only slightly:

There are many theories to explain the divergence: global (especially Chinese) competition, the impact of technology, and rising land values. But another theory -- rising market power -- is gaining increasing currency in the profession.

In the past few years, a series of papers by a mix of younger and well-established economists has argued that industry is becoming more concentrated, partly as a result of mergers; that this concentration has led to higher consumer prices and lower wages; and that companies are managing to squeeze more profit out of the economy even as they invest less for the future.

Now the concern about monopoly power is spilling out beyond the halls of academia, and reaching the ears of the country’s top policy makers. At the recent Jackson Hole, Wyoming, policy conference, central bankers from the Federal Reserve heard a number of senior figures sound the alarm. Those included Esther George, the president of the Federal Reserve Bank of Kansas City, Massachusetts Institute of Techonology economist John Van Reenen, and Jason Furman and Alan Krueger, two Ivy League professors and former economic advisers to the Barack Obama administration.

Krueger’s remarks provide a good overview of the emerging consensus. He notes that even as industries have become more concentrated, the traditional forces that balance the power of corporations have weakened:

The decline in union representation and the erosion of the real value of the minimum wage have contributed to the significant rise in inequality and polarization of incomes in the U.S. since the early 1980s.

Krueger also notes that structural changes in the U.S. economy -- the rise of noncompete agreements, temp-staffing agencies and outsourcing -- have aggravated the situation.

Meanwhile, the steady drumbeat of research papers continues. A paper by economists Chris Edmond, Virgiliu Midrigan and Daniel Yi Xu built a model showing how high markups -- the difference between the price a company charges for its products and the cost it paid to create those products -- can be very detrimental to consumers. Van Reenen, with co-authors Zack Cooper, Stuart Craig and Martin Gaynor, connects monopoly power to health-care prices -- the authors looked at price variation in health=care markets and found that in places where hospitals have a local monopoly, prices are 12 percent higher. Ioana Marinescu and Herbert Hovenkamp discuss the possibility of using antitrust law to prevent companies from lowering wages, rather than maintaining the current exclusive focus on consumer prices.

It’s important to note that the economics profession isn’t in universal agreement about the issue. A team of researchers from the Economic Policy Institute has argued that rising market concentration can explain only a small part of wage stagnation. Edmond et al. caution that breaking up large companies could hurt productivity, especially if the giants are more efficient. And Van Reenen argues that changes in information technology and globalization, rather than weakened antitrust law, are the culprit behind the rise of dominant companies, by creating winner-take-all markets.

Nor are all economists joining the fight. Interestingly, those who are sounding the alarm tend to be researchers who study labor, public finance, trade and macroeconomics. Economists in industrial organization, the field traditional focused on assessing the effects of mergers and market power, have been relatively muted -- in fact, the number of empirical studies assessing the impacts of mergers after the fact has been curiously low for a number of years. A cynical interpretation is that this may be due to industry capture; economists specializing in this area may not want to jeopardize their future ability to land lucrative pro-merger consulting gigs.

But overall, economists are growing more concerned about the threat posed by corporate power. The budding antitrust movement will offer them valuable ideas, data and intellectual heft in its quest to stem the rampant power of industrial giants.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.