Dollar’s ‘Exorbitant Privilege’ Takes Another Blow

(Bloomberg Opinion) -- The International Monetary Fund released its quarterly report on global foreign-exchange reserves on Friday, and for dollar watchers, it sent some worrisome signals.

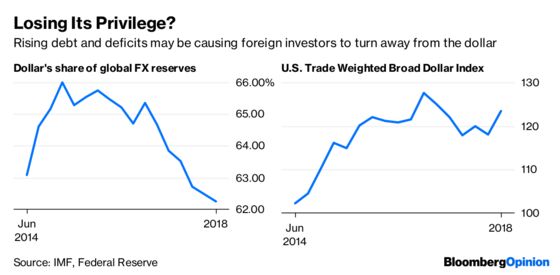

The report revealed that the dollar’s share of global reserves fell for the sixth straight quarter to the lowest since 2013, dropping to 62.3 percent in the three months ended June 30 from 62.5 percent in the prior period. It was 65.4 percent when President Donald Trump took office in January 2017.

That may seem insignificant until you realize that it came in the face of a huge rally in the greenback, with the Federal Reserve’s U.S. Trade Weighted Broad Dollar Index surging 4.52 percent. The last time the dollar’s share of global reserves dropped when its value increased by at least 4 percent was in the final three months of 2008, when everyone thought the global financial system was in jeopardy of collapsing.

The fact that the dollar’s share of global reserves edged lower in the face of a big rally may be a clear sign that foreign central banks, sovereign wealth funds and institutional investors see increased risks from holding dollars as the U.S. government rams up its borrowing to unprecedented levels to pay for what is soon to be a $1 trillion budget deficit.

Markets were in an uproar on Friday over the Italian government’s decision to run a budget deficit that is 2.4 percent of gross domestic product, worrying that the rating firms may cut the credit rating on Italy’s $2.30 trillion of government debt to below investment grade, or junk. Let’s hope they don’t take a close look at the U.S., which has $21.5 trillion of debt and is running a budget deficit that is 3.7 percent of GDP, the most in the developed world.

Yes, the U.S. — which has the ability to print more dollars to pay off its debt if it ever came to that — is much different than Italy, which is part of a currency union and can’t print euros. But more and more investors and strategists are talking about the possibility that the U.S. fiscal situation spirals out of control. JPMorgan Chase & Co. strategist Marko Kolanovic raised the question in a report this week, arguing that Trump’s isolationist foreign policy is a “catalyst for long-term de-dollarization.”

Put another way, the dollar is in jeopardy of no longer being the world’s primary reserve currency and enjoying the “exorbitant privilege” that goes along with that, such as interest rates that are lower than they might otherwise be and the government being able to fund budget deficits in perpetuity. “With the current U.S. administration policies of unilateralism, trade wars, and sanctions increasingly affecting both friends and foes, the question arises whether the rest of the world should diversify away from the risks of the U.S. dollar and dollar-centric finance,” Kolanovic and his team of quantitative and derivatives strategists wrote in a research note.

Donald Trump’s refrain may be “America First,” but his policies are threatening the preeminence of the greenback.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.