The World’s Dullest Multibillion-Dollar Scandal

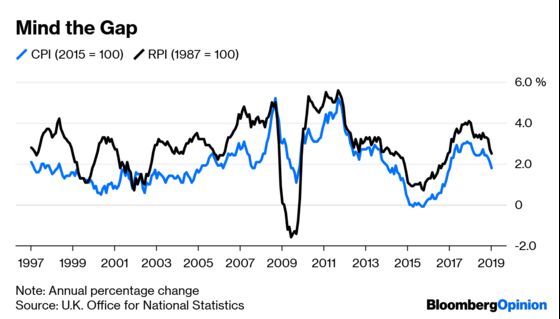

U.K. measures inflation using indicators like the RPI and the CPI. Awkwardly, both have long yielded mismatched inflation rates.

(Bloomberg Opinion) -- Rarely has a multibillion-dollar scandal been quite so boring.

For years, the U.K. has measured inflation using rival indicators, notably the Retail Prices Index and the Consumer Prices Index. Each has its place. CPI is used by the Bank of England to guide monetary policy, for instance, while RPI is used as the reference rate for inflation-protected government bonds.

Awkwardly, the two measures have long yielded mismatched inflation rates, with RPI typically producing a higher estimate. When a new methodology for measuring clothing prices was introduced in 2010, that difference widened sharply — from about 0.5 percentage point to an average of about 0.8 percentage point in the years since.

That’s a big deal. For one thing, investors in inflation-linked gilts have benefited from significantly higher coupon payments than they otherwise would have. The government, in turn, has had to pay more for its borrowing — to the tune of some $1.3 billion in unplanned taxpayer generosity each year. Those costs stretch far into the future: Some of the gilts won’t mature until 2068.

It gets worse. Far from fixing this discrepancy, successive governments have used it to their advantage. In a practice called “index shopping,” they’ve tended to use RPI for raising revenue (when calculating rail fare and the interest on student loans, for instance) and CPI when determining outlays (for welfare, pensions and so on). In effect, bond investors benefit at the expense of commuters and students, a redistribution that would likely be unpopular (to put it mildly) if made more explicit.

An oddity of this scandal is that everyone knows. Various reviews over the years have concurred that the current arrangement is indefensible as public policy. In statements last week, two parliamentary committees called the situation “grossly unfair” and “a ridiculous merry-go-round.”

Ending the ride should be a priority. A seemingly obvious solution would be to abolish the RPI, which the U.K. Statistics Authority concedes “is not a good measure of inflation” and “does not have the potential to become one.” Unfortunately, it’s not so simple. RPI’s use is mandated by law in some cases and by contract in others, including in many private-sector pension plans. Hundreds of billions of dollars in liabilities are linked to it, not counting all the lawyers’ fees.

Given that reality, two steps would be helpful.

One is to reduce distortions in the bond market. As a start, that should mean indexing new gilt sales to CPI. What to do with existing gilts linked to RPI is a harder question. Shafting investors who reasonably expected those bonds to produce a higher return wouldn’t be fair. But letting RPI stagger on without changes would be irresponsible.

An imperfect solution is to keep RPI in place, but resume making incremental adjustments to its methodology — for instance, by mitigating widely acknowledged flaws in its measurement of clothing prices. Investors will still grumble as the spread between the two indexes narrows. But the prospectuses they signed on to, in almost all cases, explicitly allow for such changes; the key is to enact them gradually and defensibly.

A second step is to phase out both RPI and CPI for all future government uses in favor of a single transparent inflation metric. Doing so would simplify matters, bolster public confidence in official statistics, prevent bureaucratic index shopping, and eliminate a substantial and inadvertent redistribution of taxpayer funds.

For all its tedium, this scandal exemplifies an important truth of policy making. Accurate metrics are an essential part of governance, and small changes in methodology can, in aggregate, have a profound effect on public welfare. They must be maintained with extreme care and foresight — and fixed when things go wrong.

Editorials are written by the Bloomberg Opinion editorial board.

©2019 Bloomberg L.P.