(Bloomberg Opinion) -- Don’t write off these stock rallies yet.

S&P 500 Index futures fell as much as 2.2 percent Monday and China’s CSI 300 Index closed 5.8 percent lower after news that Beijing is considering delaying a trip by its top trade negotiators in response to U.S. President Donald Trump’s threat to raise tariffs.

No doubt, the prospect of steeper tariffs will dent investor demand for risk assets. But the easing of trade tensions is no longer a driving force behind the U.S. stock market’s 17 percent increase or China’s 30 percent gain this year (through Friday). Eventually, the reaction to these talks will evaporate in a big fat yawn.

It’s worth pondering why animal spirits are finally stirring in the U.S. After weeks of anemic trading volume, the market saw $6.6 billion of net inflows from mutual funds and ETFs in the week ending May 1.

A revival of the IPO market is responsible for the excitement. All of a sudden, unicorns are going public. Lyft Inc., Spotify Technology SA and Pinterest Inc. just did; Uber Technologies, Slack Technologies Inc. and WeWork Cos have filed; and even SoftBank Group Corp. is now floating the idea of listing its $100 billion Vision Fund in the U.S.

As long as interesting new companies keep on going public, investors will be lured in: A stock market without new IPOs is a dead pool. Considering the universe of U.S. public companies has been shrinking since the 1990s, it’s little surprise that this turnaround has helped to heat up the market.

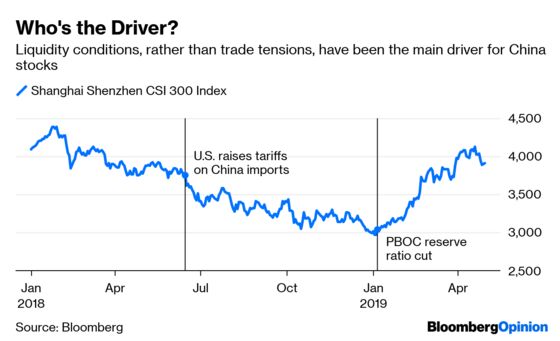

Move onto China. It’s no secret that domestic liquidity conditions have been the prime mover behind the world’s most volatile major market.

Case in point: Last year, Chinese stocks fell into a bear market even before the U.S. raised tariffs by an additional 25 percent in mid-June. Investors sold out on concern that Beijing’s deleveraging campaign would make it difficult even for companies with solid fundamentals to refinance. Escalating trade tensions were merely an unpleasant add-on.

Look at this year’s bull run. It took off only after the People’s Bank of China announced a reserve ratio cut on Jan. 4, when policy makers became alarmed that the nation’s manufacturing PMI – albeit heavily influenced by trade conditions – fell into a contraction in December.

The market churned along happily until mid-April, when traders came to realize the central bank wasn’t opening the floodgates. A much-anticipated reserve ratio cut on April 1 didn’t materialize. Even worse, the central bank has been skipping open-market operations, saying there’s enough liquidity in the banking system. It has a point: Total social financing jumped to 8.2 trillion yuan ($1.2 trillion) in the first quarter, from 5.9 trillion yuan a year earlier. Industrial output growth also rebounded to 8.5 percent, the fastest since 2014.

Ironically, Trump’s trade threats may force the PBOC’s hand and help halt a slide in the benchmark index from its April 19 year-to-date high. On Monday morning, the central bank said it would lower reserve ratio requirements for smaller banks.

The question is whether this will be enough. Chinese stock investors have been plagued by negative factors such as heavy insider selling and goodwill impairments. Last year, Shenzhen-listed companies wrote down a whopping 359 billion yuan of assets, 72 percent more than in 2017. While investors were away for the Golden Week holiday, Kangmei Pharmeceutical Co., one of the largest traditional Chinese medicine providers, said it overstated its cash holdings by 30 billion yuan. Such episodes erode confidence in the integrity of listed-company accounts.

Trade matters, but it’s no longer center stage. The U.S. market can continue to churn as long as unicorns go public. As for China – well, it’ll just stay a basket case.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.