The Muscle That Backed China's Stimulus Is Quaking

China’s $2 trillion development bank has been noticeably low-profile and may not be in shape to help this next round of easing.

(Bloomberg Opinion) -- China’s most prominent development bank has been noticeably low-profile lately.

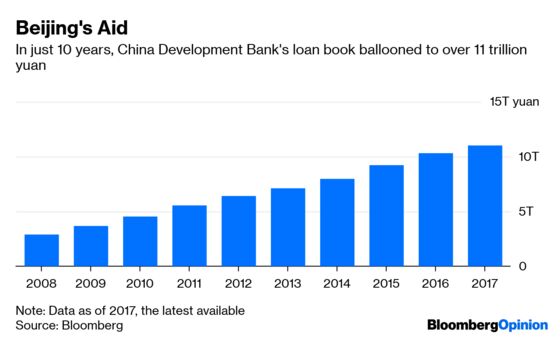

For the last decade, the 16 trillion yuan ($2.39 trillion) China Development Bank, and its less-muscular cousins Agricultural Development Bank of China Ltd. and Export-Import Bank of China, were on the forefront of every major stimulus push. In 2008, CDB financed the 4 trillion yuan spending pledge by the Ministry of Finance, its former controlling shareholder. The bank shifted its focus to the monetary side after 2015, disseminating 3.5 trillion yuan of helicopter money for the central bank via shantytown developments.

At this year’s National People’s Congress, though, policy banks seemed to be getting sidelined. There was hardly any mention of them; instead, the heavy stimulus lifting will be financed by special-purpose municipal bonds.

Policy banks are also beginning to feel uneasy with the quality of their loan books. China Minsheng Investment Group Corp., the latest default basket case, is now in a disagreement with its leading creditors over whether to offload the company’s assets to pay down debt, Debtwire reported. China Minsheng is pressing for a straightforward asset sale to raise cash, but the Export-Import Bank of China is concerned that a fire sale could cause creditors to take a haircut.

While CDB is in talks to fix the debt woes of a few municipalities, the finance ministry hasn’t blessed any large-scale bailout packages, Caixin reported last month. As of last June, the bank was already tightening its oversight of new shantytown development projects, wary of exposure to local government debt.

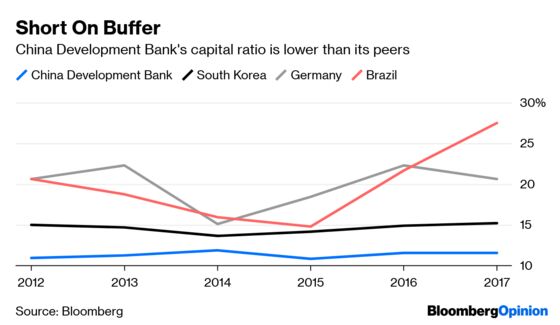

They should be worried. CDB’s total assets – two-thirds of which are loans – have ballooned to more than 15 percent of China’s GDP, making it by far the world’s biggest development bank. However, its nonperforming loan ratio, at 0.7 percent, is unrealistically low, and its capital buffer against bad loans is below its global peers.

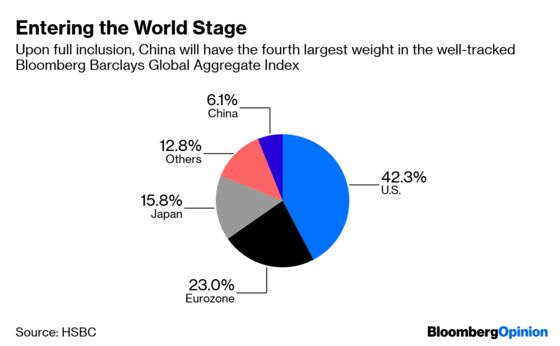

Soon, foreign investors will be putting policy banks under the magnifying glass. On April 1, China’s government and policy-bank bonds will be included in three of Bloomberg Barclays’s bond indexes. If fund managers follow the benchmark, China may see more than $150 billion of net inflows, estimates HSBC Holdings Plc. Upon full inclusion, China will have the fourth-largest weight in the widely tracked Bloomberg Barclays Global Aggregate Index. Bloomberg LP owns the Bloomberg Barclays indexes, and is the parent of Bloomberg News.

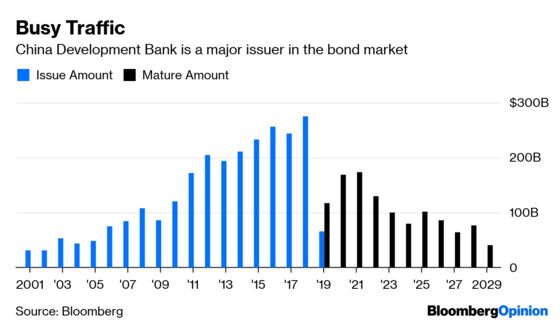

Unlike the big state-owned commercial banks, which rely on household deposits for funding, China’s policy banks utilize bond markets. CDB, for one, is a busy issuer.

Currently, CDB pays 20 basis points to 70 basis points more than notes issued by the Ministry of Finance. That’s only to compensate investors for the 25 percent capital-gain tax that they have to pay to hold non-sovereign issues. In practice, CDB bonds are viewed just like Chinese government bonds.

But should they be? While the Ministry of Finance has been careful to keep its official fiscal deficit within the 3 percent international standard, China’s policy banks have been doing the dirty work, offering loans to local governments to build roads to nowhere and apartment complexes that stay empty.

One could argue that in this round of easing, policy banks aren’t well-positioned to help. The big problem now is that the private sector has limited access to funding, and these businesses are too small to be on CDB’s radar.

That may well be. But the policy banks also have thousands of hidden wounds. One day, they may need a bailout themselves.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.