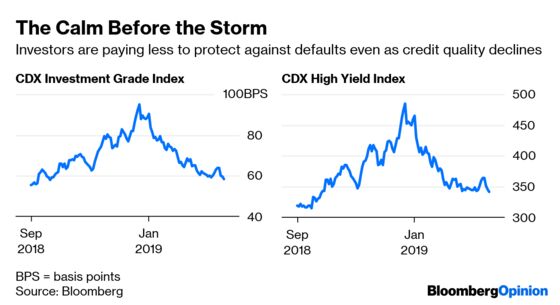

(Bloomberg Opinion) -- To say credit markets had a good day Wednesday would be an understatement. Indexes that measure the cost to protect both investment- and speculative-grade U.S. corporate bonds from default fell to their lowest levels since October, a sign of optimism about borrowers’ ability to pay their debts. Too bad about the Oaktree Capital announcement.

The credit-focused investment firm announced that it was selling a 62 percent stake to Brookfield Asset Management in a deal worth about $4.7 billion. On first glance, one might think this is a big vote of confidence in the debt markets. Otherwise, why buy into a firm that invests in the securities? Well, for one, Oaktree’s chairman and co-founder is the legendary Howard Marks, who built his fortune as a vulture investor in distressed debt. The firm controls about $22.3 billion of such assets. Perhaps Brookfield and Oaktree sense that the credit markets are about to enter a severe downturn and they are teaming up to take advantage of the fallout. That theory sounds more than plausible considering some comments Marks made last month on a conference call to discuss the firm’s fourth-quarter results. “Now is a good time to have dry powder,” given the outstanding amount of low-quality debt and fallen-angel candidates at risk of a downgrade, he said. “The pieces are in place,” Marks said, “but we need an igniter and that will probably require a recession.” Fallen angels are investment-grade companies that have their ratings cut to junk. The potential universe of fallen angels has never been bigger. About half the bonds in the $5 trillion U.S. investment-grade debt market have BBB+, BBB or BBB- ratings. That lowest tier of investment-grade has more than tripled since 2008. Then there’s the universe of junk-rated corporate loans, which have more than doubled to $1.15 trillion since before the financial crisis.

Oaktree Chief Executive Officer Jay Wintrob said in June he ultimately expects a flood of troubled credits topping $1 trillion as rising interest rates overwhelm low-quality loans and bonds. As for the igniter that Marks is looking for, it’s no secret that the economy is slowing. More than three-quarters of business economists expect the U.S. to enter a recession by the end of 2021, according to a semiannual National Association for Business Economics survey released late last month. That may seem like a long way off, but consider that the survey showed 10 percent of respondents see a recession beginning as soon as this year, while 42 percent project one will happen next year.

EQUITY TRADERS TAKE THE LONG VIEW

Stock investors also seemed to fail to fully appreciate the implications of the Brookfield-Oaktree tie-up, with the S&P 500 Index rising to its highest level in five months in intraday trading. Maybe they don’t subscribe to the theory that worsening credit conditions could be bad for stocks. The thinking here is that company executives would most likely divert cash from buybacks and dividends to paying down debt if it looked as if their credit ratings were in jeopardy of falling below investment grade. Another way to think about the strength in stocks is that the equities market has already discounted the stagnant earnings growth projected for this quarter and next, and is already looking ahead to the time when earnings begin to rise again. Earnings for members of the S&P 500 are forecast to drop 1 percent in the first half of 2019 from a year earlier before jumping 6 percent in the second half and 11 percent in 2020, according to Bloomberg Intelligence. Such optimism isn’t crazy after some data Wednesday suggested the first signs of green shoots in the economy. The Commerce Department said orders placed with U.S. factories for business equipment rebounded in January by the most in six months. “The durable goods report suggests continued growth, albeit modest growth, in heavy equipment in the U.S., defying the weakness evident in declining equipment orders in Japan and Germany,” FTN Financial chief economist Chris Low wrote in a note to clients.

OIL IS BREAKING OUT

But before popping open the champagne, keep a close eye on the oil market. Crude is back on the move, with West Texas Intermediate futures surging as much as 2.76 percent Wednesday. Oil reached $58.44 a barrel, the highest since mid-November, extending the rebound from its December lows. The spark for the latest gain was a decline in U.S. crude and fuel stockpiles, which added to evidence of tighter supplies, according to Bloomberg News’s Alex Nussbaum. The U.S. Energy Department’s closely watched weekly inventory report showed a 3.86 million-barrel decline for crude last week, defying forecasts of an increase. A 4.62 million drawdown for gasoline was the steepest since October. “We see this data as bullish for crude over the longer term," Leo Mariani, a Keybanc Capital Markets analyst, wrote in a research note to clients. The combined fall in crude and refined products “implies that the market is under-supplied." Crude and refined products in storage fell by 10.2 million barrels last week, according to the Energy Information Administration’s report. That pushed down total petroleum stockpiles to their lowest since December. Oil imports also slipped, offering another sign that OPEC curbs and U.S. sanctions on Venezuela are impacting the market. Oil is still far below the more than $70 barrel of early October, but rapidly rising prices have the potential to curb profit margins and consumer spending.

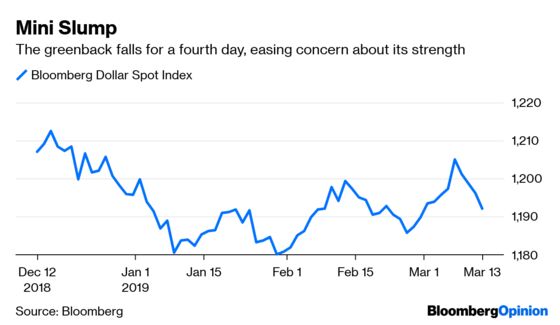

THE GREENBACK’S SLUMP

The dollar is starting to become a tailwind for risk sentiment. The Bloomberg Dollar Spot Index fell for the fourth straight day on Wednesday, bringing its decline over the period to 1.09 percent. The index, which measures the greenback against its major peers, is now back in line in with its three-month average. President Donald Trump has bemoaned the dollar’s gains, saying at the start of the month it was too strong and that U.S. companies might benefit it were weaker. The first part of Trump’s observation is debatable, but the second part carries some truth. S&P Global Ratings figures that 30 percent of the revenue of S&P 500 companies comes from outside the U.S. Jodie Gunzberg, managing director and head of U.S. equities at S&P Dow Jones Indices, calculated that the S&P 500 rises 3.7 times more from a falling dollar than a rising one. So, all else being equal (which it almost never is), the drop in the dollar should be a benefit for riskier assets such as stocks. The general sense among currency strategists is that the dollar is probably more inclined to fall than rise, especially if the worst of the global economic slowdown has past. If true, traders would be more inclined to scoop up some of the more beaten-up currencies in recent months, such as the Australian dollar, Swedish krona and Norwegian krone. A trade deal between the U.S. and China may also be negative for the dollar, as traders see less of a need for holding assets that are considered havens.

BRAZIL’S BOLSONARO BLUES

Brazil’s Ibovespa index of stocks surged about 40 percent between mid-June and the end of January as new president and populist Jair Bolsonaro brought big plans for reform. Along the way, Brazil became the darling of emerging-market investors. But since then, the Ibovespa has largely moved sideways, mainly due to concern that Bolsonaro might not be able to push through his various market-friendly economic proposals, such as easing environmental restrictions and boosting mining production through reforms, in the wake of the Vale dam disaster. Now, fresh data Wednesday will only raise pressure on Bolsonaro to prove investors were right to jump into Brazilian financial assets late last year. Government data showed that industrial output dropped 0.8 percent in January following 0.2 percent growth a month earlier. The decline was worse than forecast by all but one of 35 analysts surveyed by Bloomberg. January output fell 2.6 percent from the same month a year ago. The drop suggests companies are avoiding new investment despite record-low interest rates, according to Bloomberg News’s David Biller. The data also comes a month after Ford Motor Co. announced closure of its Brazil factory that assembles trucks. “The broadly weak industrial output in January deals another blow to expectations of a pickup in recovery,” Bloomberg Economics’s Adriana Dupita wrote in a research note. Nevertheless, the Ibovespa jumped about 1 percent on a day that the broader market for emerging-market stocks was little changed. Perhaps investors think that there’s no rising pressure on Brazil’s central bank to ease monetary policy.

TEA LEAVES

New home sales in the U.S. for December blew away the estimates, surging 3.7 percent when economists forecast a drop of 8.7 percent. Lower mortgage rates and more-affordable properties were among the reasons for the unexpected performance. Will lightning strike twice when the government releases new-home sales data for January on Thursday? The median estimate of economists surveyed by Bloomberg is for a very slight 0.2 percent increase. Bloomberg economists think so, forecasting an increase of 4.7 percent. They cite the 13 percent surge in mortgage applications in January, a 5 percent jump in pending home sales that month and a marked slowdown in home-price appreciation that has made owning a home more affordable. Developers are certainly confident. The National Association of Home Builders’s monthly sentiment index rose in February by the most since December 2017. The point is, a healthy real estate market may factor into the Fed’s decision-making over whether to raise interest rates this year.

DON’T MISS

Traders Have Made a Dangerous Bet on Brexit: Lionel Laurent

ETFs Can Temper Market Crashes, Reduce Contagion: Aaron Brown

Three Things to Keep in Mind About MMT: Mohamed A. El-Erian

Three Buzzwords That Point to a China Stocks Boom: Shuli Ren

Glass-Half-Full Hedge Funds May Get Doused: Stephen Gandel

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.