(Bloomberg Opinion) -- Stocks plunged the most since October on Tuesday, with the Dow Jones Industrial Average at one point plummeting 818 points. The thinking among commentators was that the sell-off was sparked by some tweets from President Donald Trump, calling himself “Tariff Man” and implying more are on the way if talks with China break down. But a bigger bogeyman has rattled investors, and it’s called the bond market.

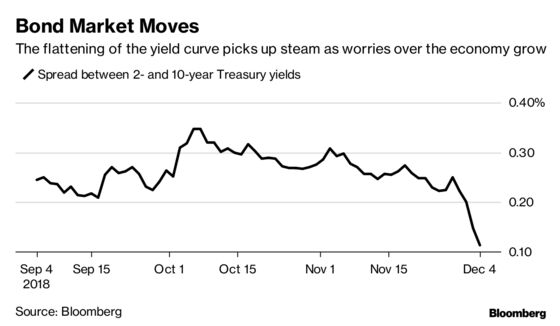

On Monday, for the first time since 2007, a small part of the yield curve inverted as yields on five-year Treasury notes fell below those on three-year notes. As Wall Street interns learn on their first day on the job, an inverted yield curve has historically preceded a recession. So, at the very least, an inverted curve carries a lot of shock value. The one saving grace is that the more widely watched difference between two- and 10-year Treasury yields has yet to invert, but bond traders seem to be doing their best to make sure that happens. Not because the economy is about to go over a cliff tomorrow, next week or even next month, but because as is the case so often in markets, that’s what momentum dictates as those betting on a wider yield curve capitulate and reverse those trades. The gap between two- and 10-year yields has rapidly shrunk in recent days, to 11 basis points from 25 last Wednesday. The potential for an inverted yield curve is the market’s equivalent to the “bogeyman,” the strategists at Brown Brothers Harriman wrote in a research report Tuesday. They feel the move has less to do with the economic fundamentals, especially since the Institute for Supply Management said Monday that its manufacturing gauge for November rebounded and continues to hover around the highest levels since 2004 while the unemployment rate is below 4 percent. “Economic conditions have not shifted that much over the past few weeks” to warrant an inverted yield curve, the strategists added.

The Brown Brothers strategists are correct, but the markets — especially the bond market — are forward looking. And the recent action in the bond market suggests that traders don’t seem to like what they see coming in terms of the economy. S&P Global Ratings issued a report Tuesday saying that it expects economic growth to slow to 2.3 percent in 2019 from 2.9 percent in 2018. It gets worse after that. “As the boost from recent fiscal stimulus fades and the central bank’s monetary tightening begins to take hold, we forecast growth in the world’s biggest economy slipping back to 1.8 percent by 2020,” S&P Chief Economist Beth Ann Bovino wrote in a research note Tuesday.

WHERE’S THE BEEF?

That’s not to say that Trump’s tweets threatening additional tariffs on China aren’t weighing on stocks. They are. Stock traders are concerned that no real deal was struck between Trump and China’s Xi Jinping in Buenos Aires over the weekend. They care little about Trump’s tweets describing his “very strong and personal relationship” with Xi and are demanding some evidence to back up his assertions that something monumental was agreed upon. Because if more tariffs are on the way, that will just weigh on the rapidly decelerating profit growth of U.S. companies. Fourth-quarter profit forecasts have declined steadily to 13.6 percent from 16.1 percent at the end of October and 17.1 percent at the end of September, according to DataTrek Research. Looking to 2019, Bloomberg Intelligence says U.S. profit growth will decrease to a rate that’s more in line with the rest of the world. That’s important because U.S. profit outperformance in late 2017 and for much of this year has allowed American stocks to trounce their global rivals. Earnings for companies in the MSCI All-Country World Index excluding the U.S. are expected to rise 9.7 percent in 2019. “Unless that estimate or the projection for a 9.3 (percent) median (earnings per share) growth rate for the S&P 500 is wrong, the earnings trend will likely start to favor non-domestic stocks,” the BI strategist wrote in a research note Tuesday.

YEN ATTRACTS CURRENCY BULLS

It’s also a bit unsettling that the yen, one of the world’s ultimate havens, is quickly becoming a star of the currency market. The Bloomberg Correlated-Weighted Index measuring Japan’s currency against nine developed market peers rose as much as 1.11 percent Tuesday in its biggest gain since May. The reason investors flock to the yen in times of turmoil is because Japan’s sizable current-account surplus doesn’t make the country reliant on foreign capital. Also, many investors take advantage of Japan’s ultra-low interest rates by borrowing in yen to finance investments in higher-yielding assets elsewhere. In a risk-off environment, those trades are reversed, fueling demand for yen as the loans are paid off. At about 117.80 Tuesday, the yen will probably appreciate to 105 by 2020, according to a Bloomberg survey in which the weakest estimate was for 113. The more bullish analysts, including Commerzbank AG and Morgan Stanley, see it solidly below 100, reaching levels last seen in 2013, according to Bloomberg News’s Austin Weinstein. The dollar-yen rate hasn’t closed below 100 for an extended period since 2008-2013, when investors sought shelter in Japan’s currency amid the financial crisis and its aftermath.

EMERGING MARKETS BUCK THE SELL-OFF

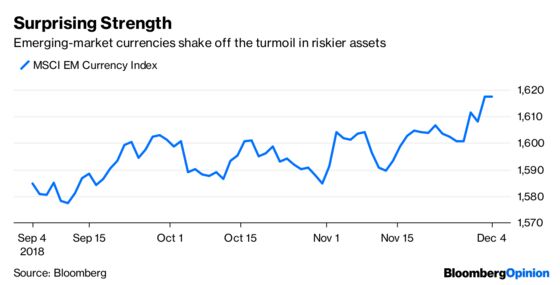

In a minor surprise, emerging markets held up fairly well despite the jitters in U.S. stocks. The MSCI Emerging Markets Index of currencies was effectively unchanged on Tuesday, holding at its highest level since early August. The equivalent MSCI index of emerging-market equities dropped just 0.5 percent, barely eroding Monday’s gain of 2.23 percent. These markets have a had tough go of it for much of the year amid concern that a rising dollar will make it incredibly expensive — or almost impossible — for borrowers in developing nations who gorged on cheap dollar-denominated debt in recent years to meet their obligations. The good news is that there have been no major blowups, and more investors are coming around to the notion that emerging markets can be viewed as a something of a haven. There’s no question that these economies have taken advantage of the recovery from the financial crisis to shore up their balance sheets to give them a greater cushion when times get tough. Foreign-exchange reserves for the 12 largest emerging-market economies excluding China stand at $3.13 trillion, rising from less than $2 trillion in 2009, data compiled by Bloomberg show. Although emerging-market stock volatility has risen this year, it remains a third of what it was at the end of the financial crisis a decade ago, according to Bloomberg News’s Srinivasan Sivabalan.

OIL CUTS WALKED BACK

The big rout in oil the last two months has slowed in recent days amid signs that OPEC and its key allies will cut supplies to help stem the plunge in prices. But on Tuesday, traders were bracing for a renewed decline in crude prices after Saudi Arabia’s oil chief indicated OPEC and the cartel’s allied producers have yet to reach consensus on whether supply curbs are in order, according to Bloomberg News’s Alex Longley and Alex Nussbaum. In an interview Tuesday, Saudi Energy Minister Khalid Al-Falih walked back recent calls for a cut of 1 million barrels to daily output by OPEC and other major exporters. The comments came just days after an agreement between Saudi Crown Prince Mohammed bin Salman and Russian President Vladimir Putin appeared to smooth the way for a production accord when OPEC gathers in Vienna later this week. “It’s premature to say what will happen” in Vienna, Al-Falih said in an interview at a United Nations climate-change conference in Poland. “We need to get together and listen to our colleagues, hear about their views on supply and demand and their projections of their own countries’ production.”

TEA LEAVES

U.S. financial markets are closed Wednesday for a national day of mourning for the death of former President George H.W. Bush. That’s likely to put even more of a spotlight on the Bank of Canada’s monetary policy meeting. Although no change in the central bank’s key interest rate of 1.75 percent is expected, money-market traders are beginning to doubt that policy makers will pull the trigger next month either after the steep drop in oil prices, according to Bloomberg News’s Sydney Maki. Alberta, Canada’s largest oil-producing province, just took the unprecedented step of cutting oil production next year to bolster crude prices. Bank of Montreal economists Benjamin Reitzes and Robert Kavcic predicted in a research note Monday that gross domestic product could expand by 1.8 percent next year instead of the 2 percent forecast previously if there are extended shutdowns in the oil sector. Investors globally have been paring back expectations for policy tightening next year amid signs global growth is flagging, and Canada is likely to be no exception.

DON’T MISS

Yield Curve Inversion Is a Happy Sign for Some: Marcus Ashworth

Maybe We Have the Economic-Growth Equation Backward: Noah Smith

Investors Deserve a Peek at Bond Managers’ Tricks: Nir Kaissar

Hedge Funds Should Fear Market Whimpers, Not Bangs: Mark Gilbert

Go Beyond GDP, Just Not Too Far Beyond: Leonid Bershidsky

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.