Bond Traders Need to Get Their Mojo Back

(Bloomberg Opinion) -- This year’s rebound in stocks looks to be running out of steam, geopolitical risks are on the rise and central banks are turning dovish amid evidence that the global economy is slowing. And yet the bond market is doing a whole lot of nothing when it should be roaring ahead. That should soon change.

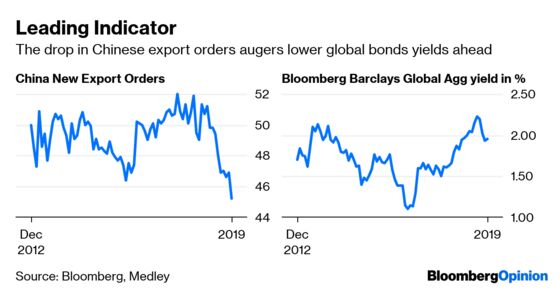

As of late Thursday, the yield on the benchmark 10-year U.S. Treasury note had traded in a tight range of just 12 basis points during February, making it the most static month since the 1970s, according to Bloomberg News’s Elizabeth Stanton. Also, the Bloomberg Barclays U.S. Treasury Index was on track to deliver its first negative monthly return since October. Now, this could be a sign that bond traders feel that the broader economy won’t get much worse. That makes sense, given that the latest forecasts show most economists don’t expect a recession to hit until late 2021. But recent history suggests there’s plenty of room for yields to move lower. Medley Global Macro Managing Director Ben Emons has noticed an interesting relationship between Chinese manufacturing and bonds yields. More specifically, Emons pointed out in a note to clients Thursday that yields tend to track the new orders portion of the China purchasing managers index with a six-month lag. Given that the most recent China PMI released Thursday fell to its lowest level since early 2016, the bond market should see sustained demand – and lower yields – in the months ahead.

After real GDP growth of 3.2 percent in 2018, aggregate growth among the Group of 20 economies will slow to 2.9 percent in 2019 and 2.8 percent in 2020, Moody’s Investors Service said in a research note Thursday. The credit-rating firm noted that key risks include a sharper-than-expected slowdown in China with negative spillovers for global growth, a further escalation of U.S.-China trade tensions and a renewed tightening of financial conditions.

STOCKS ARE GETTING STUCK

Global stocks ended a lackluster February with the MSCI All-Country World Index falling the most in about three weeks. Many markets worldwide seem to be getting stuck at key levels of resistance. For the S&P 500 Index, that level is 2,800. The benchmark did basically nothing the first three days this week, moving less than 3.5 points each day for a total journey of 7.2 points. The last time the gauge had such a small move over three sessions was 14 months ago, according to Bloomberg News’s Elena Popina. “The market has been jumping over the small hurdles on the way up, but we’re approaching the 2,800 line and the hurdle all of a sudden is four stories tall,” Michael Antonelli, a managing director and market strategist at Robert W. Baird & Co., told Bloomberg News. “We need some serious progress in U.S.- China trade talks for the S&P 500 to breach that line. As of right now, the markets are not convinced that we’re ready for new highs.” At the same time, long-short hedge funds on Credit Suisse Group AG’s prime brokerage platform have reduced their net exposure to equities in the last two weeks as they ramp up short bets, reports Bloomberg News’s Justina Lee. After slashing positions amid last quarter’s carnage, their gross positioning remains well below last year’s peaks – a 13 percent dip for long-short managers and 22 percent lower for quants.

CURRENCY TRADERS MISS YET AGAIN

If there is one word I would use to describe currency traders these days, it would probably be hapless. The Citi Parker Global Currency Index, which tracks nine distinct foreign-exchange investment styles, fell in each of the last four years, and is down again in February following a decline in January. The 1.33 percent drop for February is among the worst in recent years. There are a few takeaways from this dismal performance. The first is that currency traders are a victim of low volatility, which generally provides fewer opportunities to exploit wild market swings. Overall volatility in the foreign-exchange market as measured by a JPMorgan index is about the lowest since 2014. The euro-dollar cross, which sees roughly $1.25 trillion of transactions a day, has traded within 3.4 U.S. cents since the beginning of 2019, marking the tightest quarterly range since the inception of the euro two decades ago, according to Bloomberg News’s Katherine Greifeld. The most plausible reason for the decline in volatility has been the dovish shift in central bank rhetoric. To the strategists at Morgan Stanley, the drop in volatility suggests markets aren’t prepared for potential negative shocks. They cite the large 0.5 percent decline in the South Korean won on Thursday after summit talks between the U.S. and North Korea unexpectedly broke down as just one example of how the currency market is too complacent, especially given the number of potential flash points out there. These include tensions between India and Pakistan, U.S.-China trade talks that continue to drag on, the danger of a no-deal Brexit, and the political and humanitarian crisis in Venezuela.

EMERGING MARKETS ARE GETTING TIRED

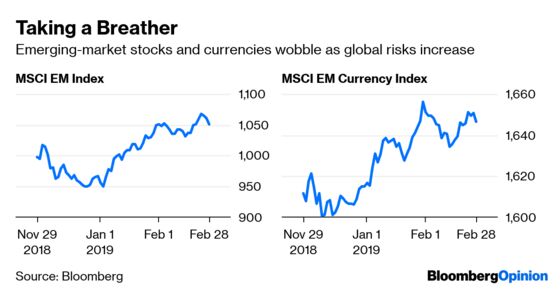

February wasn’t very kind to emerging markets outside of bonds, where yield spreads narrowed to their tightest levels since October. The MSCI Emerging Market Index of equities was essentially flat and a similar index measuring the performance of their currencies fell for the first time since October. Such results don’t speak well for the outlook for riskier assets in general. That’s especially true now that one of the bellwethers in emerging markets looks to be running into some trouble. Data on Thursday showed India’s economy expanded 6.6 percent in the fourth quarter from a year earlier, down from 7 percent in the July-September period. Waning consumer demand dampened momentum in the economy where domestic spending makes up about two-thirds of GDP, according to Bloomberg News’s Anirban Nag and Vrishti Beniwal. And that was before this week’s tensions with neighboring Pakistan. “This comes at a tricky time for both sides, as India heads into the general elections in April-May 2019, while Pakistan is in a tenuous economic position," Radhika Rao, an economist at DBS Bank, told Bloomberg News. Tensions are likely to overshadow the growth data, she added. With it’s $2.6 trillion economy, India is the “I” in the BRIC acronym that also includes Brazil, Russia and China. So, any weakness in Indian markets has the high potential to turn off emerging-market investors globally.

BEEF IS ONE COMMODITIES BRIGHT SPOT

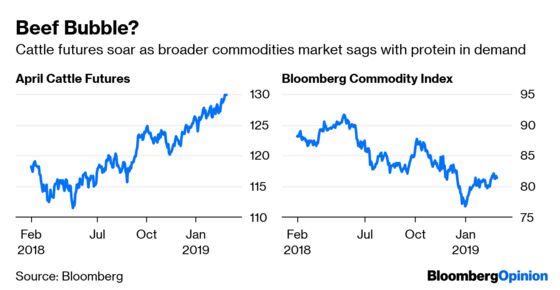

The commodities market eked out its second straight monthly gain in February, with the Bloomberg Commodity Index rising less than 1 percent following January’s big 5.23 percent surge. The results for February would have been much better if not for agricultural commodities, which tumbled about 4 percent and negated much of the gains in energy and industrial metals, which rallied more than 5 percent and 3 percent, respectively. On the whole, this is a positive sign for the global economy, or at least shows that worries about an imminent recession are overblown. But even within the agriculture complex, there are reasons for optimism. Take the cattle market, which is booming. Futures for April delivery touched a record high for the contract in Chicago this week at $1.30 a pound. The contract, which debuted in late 2017, is up 18 percent from a low in April, according to Bloomberg News’s Lydia Mulvany. Beef is a premium protein, and consumers generally cut back in times of trouble in favor of less expensive chicken and pork. And yet sales in the past four weeks for delivery 22 to 60 days out are up 16 percent compared with a year earlier, Mulvany reports, citing the Steiner Consulting Group’s Daily Livestock Report. Sales over the past four weeks for delivery 60 to 90 days out are even more impressive, more than double from 2018. “Retailers that want to once again promote ribs, strips or other such cuts now have to jump on this earlier in order to make sure they can get the regular supply,” according to the Daily Livestock Report.

TEA LEAVES

The Commerce Department said Thursday that U.S. economic growth decelerated to a 2.6 percent annualized rate in the fourth quarter. Still, that was seen as mildly positive, as economists had forecast a rate of 2.2 percent. But on Friday, market participants are likely to find out that things are probably much weaker than they seem. That’s because the government is forecast to say that real personal spending in December, which excludes inflation, fell 0.3 percent in the biggest decline since 2009. Consumer spending accounts for two-thirds of the economy. There’s more: The Institute for Supply Management is expected to say that its monthly manufacturing index dropped to 55.7 for February from 56.6 in January. Although that would still indicate healthy growth, the risk is to the downside. The reason is that the index unexpectedly rose in January, propelled higher as the orders portion of the index jumped by the most since 2014 and production gained the most in eight years. So it makes sense that there could be a big give-back in the February numbers, especially since other manufacturing data has been a mixed bag.

DON’T MISS

Central Banks Signal Need to Be Selective: Mohamed A. El-Erian

Forget FAANGs. Stock Bubble Could Be in the Cloud: Shira Ovide

The Obama-Trump Economy Is Still Chugging Along: Justin Fox

Draghi the Heretic Has a Vision for Europe: Ferdinando Giugliano

South Korea's Economy Is Alive But Not Well: Daniel Moss

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.