Bond Traders Look Ready to Call the Fed’s Bluff

(Bloomberg Opinion) -- Given all the angst about the stock market in recent weeks, including Monday’s 1.66 percent tumble in the S&P 500 Index, it would be easy to overlook the goings-on in the bond market. But doing so risks missing some critical signals about the economy and Federal Reserve policy that might both add to the anxiety and offer a glimmer of hope.

First, the bond market is signaling that the economy is less than ideally healthy. That can be seen in the performance of two-year Treasury notes, which have rallied for six consecutive trading days, pushing yields lower in the longest such streak since 2016. The monthly National Association of Home Builders/Wells Fargo Housing Market Index report released Monday only ratified those concerns as it tumbled by the most since 2014 in an ominous sign for a critical part of the economy. At the same time, the Atlanta Fed’s GDPNow index, which aims to track growth in real time, shows the economy is most likely expanding at about a 2.75 percent rate, a big deceleration from the past two quarters. The upshot is that the bond market is pricing in only about 1.5 interest-rate increases over the next year from the current range of 2 percent to 2.25 percent, compared with the Fed’s projections of four hikes. It’s not as if the Fed hasn’t overpromised before. In early 2014, when its target rate was 0.25 percent, the Fed was saying that it would rise to 1 percent by the end of 2015 and 2.25 percent a year after that. Instead, rates rose to 0.5 percent in 2015 and 0.75 percent in 2016 as the economy underperformed and inflation was slower than expected.

On the face of it, a slowdown in growth flagged by short-term bond yields is not a good thing for equity markets because it makes those double-digit profit forecasts much harder to obtain. But with the unemployment rate solidly below 4 percent, the longer end of the bond market is not reacting to the same degree, suggesting traders don’t see any slowdown as being too severe but probably just enough to maybe cause the Fed to rethink its outlook. “We’ll be likely raising interest rates somewhat but it’s really in the context of a very strong economy,” Federal Reserve Bank of New York President John Williams said Monday. “We’re not on a preset course.”

SELL THE BOUNCE

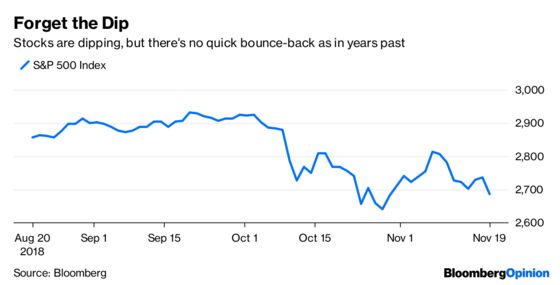

The thing about the current sell-off in stocks, which has taken the S&P 500 down a bit more than 8 percent from its record closing high on Sept. 20, is that one of the most profitable strategies in recent years is failing miserably. In other words, whenever stocks took a tumble it made sense to step in and buy as much as possible because momentum was clearly toward higher prices. But now, instead of buying the dip, more investors are deciding it makes more sense to sell the bounce to help limit losses. Morgan Stanley crunched the numbers on rolling five-day declines in the S&P 500 this year and found that on average, the sixth day also generated a loss: of 0.05 percent. It happened again Monday as the S&P 500 fell as much as 2.02 percent after a decline last week. As Bloomberg News’s Lu Wang put it, this reflects a subtle deterioration in investor psychology that may not be obvious when measuring the market by the index’s price level or through Wall Street forecasts. “While 2018 is clearly not a year of recession, the market is speaking loudly that bad news is coming,” Michael Wilson, Morgan Stanley’s chief U.S. equity strategist, wrote in a research note. “Our view is that the market is sniffing out an earnings recession and a sharp deceleration in economic growth.”

CASH IS KING

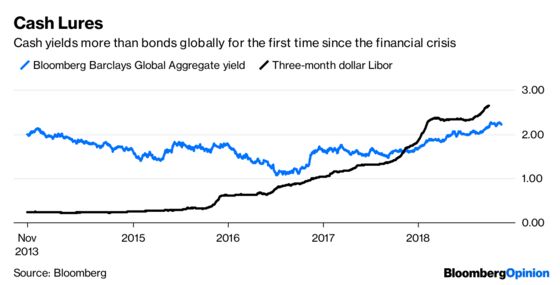

A big reason it’s been such a horrible year for all types of financial assets, from stocks to bonds to commodities, has a lot to do with cash. More specifically, there’s no longer a penalty to holding cash-like instruments, and in many cases it’s the best choice. In a remarkable turn of events, the three-month London Interbank Offered Rate in dollars stands at 2.65 percent, which for the first time since before the financial crisis is above the average yield investors can get on bonds, which is 2.21 percent as measured by the benchmark Bloomberg Barclays Global Aggregate Bond Index. “For nine years since the Lehman crisis, cash was unattractive for investors yielding close to zero and well below the yields of other asset classes such as bonds,” the strategists at JPMorgan Chase & Co. wrote in a research note. “This changed this year.” The strategists conclude that markets “have entered a phase of asset repricing” and unless cash yields stop rising, “this repricing seems likely to continue.”

UNLIKELY HAVENS

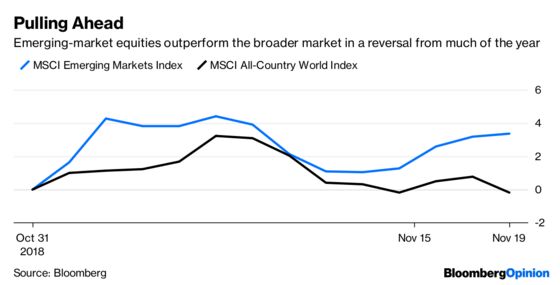

One area of the markets this is looking fairly solid is emerging markets. The MSCI Emerging Markets Index of equities has gained 3.39 percent this month, while a sister index tracking their currencies is up 1.25 percent. In contrast, the MSCI All-Country World Index of stocks is little changed. As with the U.S. Treasury market, the rally in developing-nation assets may reflect a sense among investors that the Fed is likely to raise rates less than it’s now projecting. Recall that a hawkish Fed was largely to blame for the woes in emerging-market assets between late January and last month, a period when the MSCI EM Index tumbled as much as 27 percent. UBS AG is one of a growing number of firms forecasting big gains in emerging markets in the months ahead. The firm’s strategist wrote in a report that emerging-market equities should return from 7 percent to 8 percent in 2019. Goldman Sachs says the main risk for these assets is an overheating U.S. that prompts the Fed to not only stick with its hawkish outlook, but possibly accelerate the pace of rate hikes. But the latest data show that’s looking less probable.

BEARS TAKE AIM AT OIL

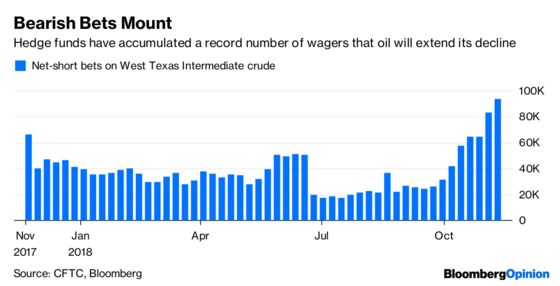

Oil managed another small gain Monday, but few traders think that crude can sustain any sort of rally that reverses the nasty four-week slump that pushed it into a bear market. The dour mood can be seen in the positioning of hedge funds, which seem to be betting OPEC will struggle to reverse oil’s plunge. Their combined wagers against West Texas Intermediate and Brent crude soared for a seventh consecutive week, the longest global short-selling streak in data going back to 2011, according to Bloomberg News’s Alex Nussbaum. The bearish bets jumped 14 percent in the week ended Nov. 13 and have tripled since the end of September, according to data from the U.S. Commodity Futures Trade Commission and ICE Futures Europe on Friday. It may take a reduction well beyond the 1 million barrels a day that’s been discussed publicly to restore faith, according to Daniel Ghali, a commodities strategist at TD Securities in Toronto. “We’ve been through not just a price shock but a momentum shock,” Ghali told Bloomberg News. “Given that, we don’t think oil will recover these losses in short order without a significant catalyst, and that may have to be OPEC doing more than expected.”

TEA LEAVES

The disaster that was Monday’s National Association of Home Builders/Wells Fargo Housing Market Index report just raised the stakes for Tuesday’s data on U.S. housing starts for October. Government figures are forecast to show a slight rebound of 1.8 percent after September’s 5.3 percent drop that likely reflected disruptions from Hurricane Florence in the South. It’s too soon to call for a real estate crash, but it’s clear that 30-year fixed mortgage rates hovering around 5 percent — the highest since 2011 and up from less than 3.50 percent in late 2016 — are biting. The National Association of Realtors says housing affordability is the lowest since 2008.

DON’T MISS

Ray Dalio Sees 1930s Parallels in Markets Today: Brian Chappatta

Hedge Funds Appear Headed Back on Defense: Stephen Gandel

How Powerful Companies Might Hold Back Growth: Mark Whitehouse

Big Oil Only Likes Its Own Subsidies, Not EVs: Liam Denning

Warren Throws Down Leveraged-Loan Gauntlet: Brian Chappatta

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.