Maybe This Bond Rating System Is as Good as It Gets

(Bloomberg Opinion) -- When it comes to credit ratings in the bond markets, it’s perfectly rational to believe both of the following things:

- S&P Global Ratings, Moody’s Investors Service and Fitch Ratings played an important role in the financial crisis because no one challenged them as they awarded top grades to subprime mortgage investments.

- Adding more competition to S&P, Moody’s and Fitch in the credit-rating industry leads to inflated ratings because borrowers shop around for the best grades.

This is something of a Catch-22, and primarily has to do with the business model of credit ratings. Because debt issuers are the ones that pay for these widely understood grades, there’s inherent pressure to give the best mark possible or risk losing a customer. Institutional investors are broadly aware of this, which is why they still employ their own team of dedicated credit analysts. It’s part of the reason concerns reached a fever pitch last year about the proliferation of highly leveraged triple-B rated companies. Bond buyers sensed that S&P, Moody’s and Fitch might be stretching their analysis to keep household brands from becoming junk.

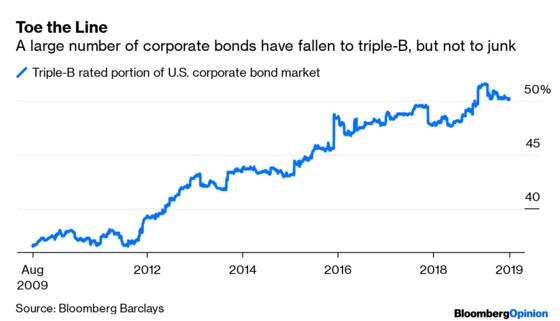

Triple-B bonds, by the way, have returned 13% so far this year, better than any other ratings tier among U.S. corporate debt, Bloomberg Barclays data show. So that fear seems to have dissipated, with investors betting that the Federal Reserve will continue to cut interest rates and these big borrowers will have no trouble refinancing their obligations at a lower cost.

However, the lingering worry about Pollyannaish credit ratings hasn’t gone away entirely. The Wall Street Journal published a feature last week titled “Inflated Bond Ratings Helped Spur the Financial Crisis. They’re Back.” The reporters say they analyzed “about 30,000 ratings within a $3 trillion database of structured securities issued between 2008 and 2019.” They found that each of the biggest ratings companies changed their criteria in some way since 2012, and each time it led to an increase in their respective market share. The conclusion:

“A key regulatory remedy to improve rating quality — promoting competition — has backfired. The challengers tended to rate bonds higher than the major firms. Across most structured-finance segments, DBRS, Kroll and Morningstar were more likely to give higher grades than Moody’s, S&P and Fitch on the same bonds.”

Of course this is what happened. And it’s not just in structured finance. Five years ago, Jim Nadler, president of Kroll Bond Rating Agency, told me something I always recall: “That’s the curse of a new rating agency. No one is going to add a fourth rating that is lower. You’ll never see the ones that we turn away or gave lower ratings to.” Kroll and Morningstar Inc. made the same defense to the Journal, arguing that if unpublished grades were included in the analysis, they wouldn’t look as lenient.

I more or less buy that argument. Are there incentives for the ratings companies, big or small, to alter their criteria to give higher scores and win more market share? Of course. The business model makes the appearance of conflicts of interest virtually unavoidable. Are there also perfectly valid reasons for these firms to update how they see markets evolving and react accordingly? You bet. If analysts did nothing to tweak their methodology, they’d probably be criticized anyway for not keeping up with the times.

This continuing concern that ratings are too optimistic is unsolvable without wholesale change. But I’m not sure anyone truly cares enough to demand it. As I wrote in May, when Morningstar agreed to buy DBRS, the industry isn’t exactly ripe for disruption. For institutional buyers, potentially off-base credit grades are a feature of the system because they can use their own analysis to take advantage of any mispricing. The Securities and Exchange Commission certainly seems in no hurry to shake things up. And if the financial crisis couldn’t bring down the “Big Three” for failing investors, it stands to reason that nothing will.

Some have said the solution is for bond buyers (not borrowers) to pay S&P, Moody’s or other firms for their ratings. This will almost surely never happen. For one, the credit-rating companies need to work with borrowers to gain timely access to crucial financial information. But just as important, the investment-management industry is already being transformed as it looks to cut fees to as little as possible. The last thing money managers need is another added cost of doing business.

That leaves credit markets mired in the status quo. And that’s probably just fine. In general, my theory is that if all of Wall Street is worried about the same thing, then it’s unlikely to be the true flashpoint. I said as much in November, when large fund managers were warning of a “slide and collapse in investment-grade credit” precipitated by triple-B companies like General Electric Co. Fast-forward to the present, and GE’s perpetual bond is again trading closer to 100 cents on the dollar. Broadly, corporate credit spreads last month reached the narrowest level in about 10 months.

The same reasoning applies for credit ratings. The system isn’t perfect by any stretch, but at least the structural flaws are transparent. For those who specialize in commercial mortgage-backed securities or collateralized loan obligations — the Journal highlighted both as having looser credit standards — it shouldn’t take an inordinate amount of effort to understand what’s under the hood of each company’s grades and price the securities accordingly.

So, yes, seemingly inflated bond ratings are back. The truth is, they never left.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.