(Bloomberg Opinion) -- Can we finally stop doubting the bond market? Last year was supposed to be when the bond market finally “broke,” as interest rates rose, the Federal Reserve started to shrink its balance sheet and a ballooning budget deficit caused the U.S. to more than double its borrowing to $1.34 trillion. And yet the Bloomberg Barclays U.S. Treasury Total Return index managed to gain 0.86 percent. That’s nothing to brag about, but it’s far from the carnage predicted. As a result, bond market naysayers just pushed back their predictions of doom to 2019. And although it’s still early days, it’s looking as if the bears may be wrong again.

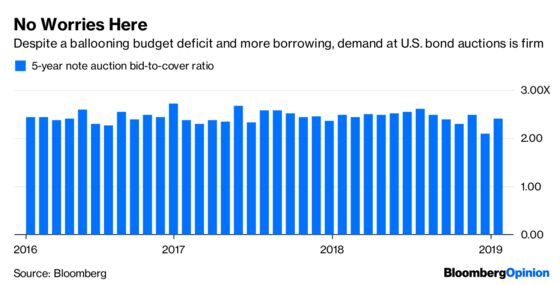

Despite predictions that annual new issuance will range from $1.25 trillion to $1.4 trillion over the next four years, bond sales so far in 2019 are off to a robust start. Even with the U.S. poised to borrow some $320 billion this week alone in bills and notes, demand at the government’s auctions on Monday of two- and five-year securities was in line with the average over the past 36 months. The one thing many bears tend to overlook is the role of the dollar. The greenback is by far the world’s primary reserve currency, with a 61.9 percent share compared with 20.5 percent for the euro. That creates inherent demand for Treasuries. James McCormick, the global head of desk strategy at NatWest Markets, wrote in a research note Monday that he had just returned from a trip to Asia, where “investors seem to care about the massive Treasury supply.” It’s even possible that the rising supply of Treasuries could spur demand rather than diminish it, according to Torsten Slok, Deutsche Bank’s chief international economist. As Slok sees it, the dollars going into Treasuries would otherwise have gone into more productive uses such as credit and equity markets. Logic suggests that as riskier assets struggle, risk-free assets such as Treasuries should do better.

“In finance terms, U.S. Treasuries (are) a risk-free asset, and page one in your MBA finance textbook tells you that with the government issuing more risk-free assets and the Fed running down (its) balance sheet (while) at the same time raising the return on risk-free assets, there are simply fewer dollars available to put into risky assets,” Slok wrote in a research note. “The dramatic increase in the supply of risk-free assets since the beginning of 2018 is probably the reason why” in 2018 “despite very strong GDP growth saw negative returns” in stocks and credit markets, Slok added.

A RECESSION LOOMS — IN EARNINGS

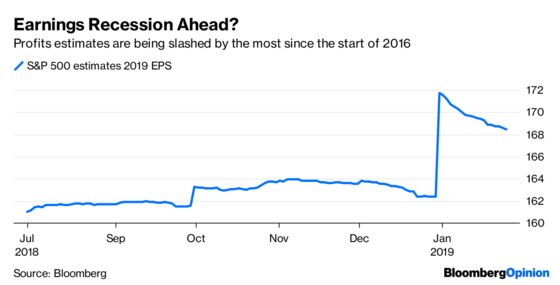

As if confirming Slok’s thesis, the demand for Treasuries rose on Monday as stocks took a big dip lower on global growth concerns and the deteriorating outlook for earnings. At one point, the S&P 500 Index was down as much as 1.53 percent in its biggest intraday loss since Jan. 3 as Caterpillar and Nvidia posted disappointing results. But even before those announcements, there was increased talk of a looming “earnings recession.” According to DataTrek Research, analysts as of Jan. 4 had predicted first-quarter earnings growth of just 2.9 percent, which is well below the 20 percent or more pace for much of last year. Now those expectations have been cut to 0.7 percent. It’s not much better for the second quarter, where profits are seen rising by a meager 2.4 percent, which is barely above the rate of inflation. So was the S&P 500’s 5.15 percent gain for the year through Friday the best it’s going get in 2019? Perhaps so, according to Morgan Stanley chief U.S. equity strategist Michael Wilson. “Even if the full ‘8 seconds’ of this rally hasn’t passed, we’d still look to dismount,” Wilson wrote in a research note. As DataTrek co-founder Nicholas Colas notes, equities have held up well this month despite the cut in profit estimates because of the belief that the Fed will stand pat on rates and the U.S.-China trade war will end soon. “Fair enough, but we worry whenever earnings growth rates teeter around zero,” Colas wrote in a research note. “And that’s the setup we have right now.”

COMMODITIES CONFIRM THE TREND

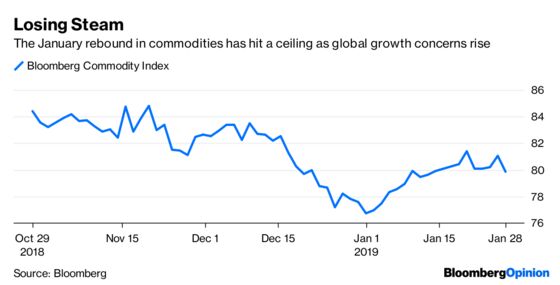

The market for raw materials confirmed the negative tone of risk assets. The Bloomberg Commodity Index fell as much as 1.63 percent in its biggest decline since December. Oil, base metals and most agricultural products took a beating in a coordinated sell-off that would be unlikely if the economic outlook was even somewhat bright. “This is a broader risk-off move,” Ryan McKay, a commodities strategist at TD Securities, told Bloomberg News. The earnings reports are “a bad sign for demand in China and for global growth overall, and that’s a big worry for crude markets these days.” Crude oil futures in New York dropped as much as 4.4 percent even as Saudi Arabia said it expects to reduce oil output once again in February and pump for six months at levels “well below” the production limit it accepted under OPEC’s oil-cut accord. Aluminum was a big loser, dropping as much as 3 percent in London, as the U.S. lifted sanctions on Russia’s United Co. Rusal, removing the threat of major supply disruption that had lingered since last April. Iron ore was one of the few winners, with May futures rallying as much as 6.3 percent in China after a deadly dam collapse at a Brazilian mine run by top producer Vale SA spurred concern that global supplies will be interrupted, potentially tightening the market and aiding the company’s rivals.

DAM BREACH TESTS BRAZIL

The so-called Bolsonaro bull market in Brazil took a hit Monday after the Vale dam breach that left at least 60 people dead and 292 missing. The world’s biggest producer of iron ore suspended dividends as it braces for the financial fallout of the catastrophe, according to Bloomberg News. The shares plunged the most on record, wiped out about $18 billion in market value and contributed to a decline of as much as 2.96 percent in Brazil’s benchmark Ibovespa index of equities. Of course, the Ibovespa was due for a pullback after surging 40 percent since mid-June, but it’s hard to overestimate the fallout from the dam breach on Brazil’s economy. Analysts see Vale’s stock remaining under pressure as remediation charges, lawsuits and potential halts in other mines pose growing risks. The dam break in the city of Brumadinho in the Minas Gerais state has already prompted $3 billion in blocked funds and fines. It is also a test of new President Jair Bolsonaro, a populist who brought with him big plans for reform. The question now is whether he will be able to push through his various market-friendly economic proposals, such as easing environmental restrictions and boosting mining production through reforms.

HARD LUCK FX TRADERS

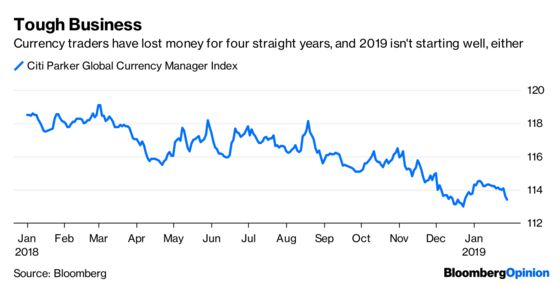

Currency traders are starting 2019 like they ended 2018, 2017, 2016 and 2015. In other words, the losing streak continues. The Citi Parker Global Currency Index, which tracks nine distinct foreign-exchange investment styles, is down 0.78 percent for the month with just three trading days left in January. But then, that shouldn’t be surprising because the index has fallen in each of the last four years and in seven of the last eight. Of course, there’s plenty of time left in the year for currency traders to turn it around, but history isn’t on their side. In an increasingly globalized economy, the old textbooks that once taught how exchange rates were largely set by interest-rate differentials among countries and trade flows are largely irrelevant. Now, traders must consider a seemingly infinite number of variables, including equity flows, direct investment, valuations and investor sentiment, GAM Holding AG group chief economist Larry Hatheway wrote in a Bloomberg Opinion piece last year. Add the lack of volatility, which reduces the chances to profit from price discrepancies, to the mix. The JPMorgan Global FX Volatility Index fell to 7.80 on Friday, its lowest since the start of August.

TEA LEAVES

The global economic and geopolitical calendar is loaded this week, from the Fed meeting to the resumption of U.S.-China trade talks to the monthly U.S. employment report on Friday. In other words, it would be easy to overlook some events that have the potential to impact markets worldwide. One of those events is Tuesday, when rival factions of the U.K. Parliament will fight to take control of Brexit and determine whether it will probably be paused — perhaps indefinitely — or whether Prime Minister Theresa May will be sent back to Brussels to negotiate a new deal to leave the European Union, according to Bloomberg News. Currency traders could be among the most vulnerable if something unexpected happens. That’s because sterling has been among the best-performing currencies this month, with the Bloomberg Pound Index rising on Friday to its highest level since June.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.