The Bond Market Hasn’t Forgotten About Inflation

The potential for rising prices leads market commentary. Plus, Saudi crude cutbacks, a boost for Brazil and more.

(Bloomberg Opinion) -- For all the concern about a global synchronized economic downturn, the bond market sure seems to be worried about the potential for faster inflation, and not just because the U.S. Treasury market had a down day on Monday. Rather than in the absolute level of yield levels, the worry seems to be showing up in the relative level of yields.

Breakeven rates on two-year Treasuries — a measure of what bond traders expect the rate of inflation to be over the life of the securities — has risen to the highest since May. In addition, the difference in yield between bonds due in 10 years and longer-term debt due in 30 years – a part of the curve that’s less influenced by Fed policy – is the widest since 2017. That wouldn’t be the case if bond traders expected inflation to stay muted. To be sure, no one is calling for runaway inflation. At 1.90 percent, the two-year breakeven rate is below the Fed’s 2 percent inflation target. Also, the yield curve for longer maturities is about half the average over the past decade. Nevertheless, bond traders are suggesting it’s time to be cautious, given all the talk out of the Fed of late about whether it makes sense to let inflation “run hot” for a period to make up for all the times it fell below the central bank’s target. There was even speculation Fed Chairman Jerome Powell might announce an “inflation averaging” policy during his 60 Minutes Sunday. He didn’t. But that’s not all. Bond traders are also worried wages are finally rising at a pace that should allow consumers to tolerate higher prices. The government said Friday that wages surged 3.4 percent on February from a year earlier, the biggest increase since 2009.

Of course, this repricing of inflation expectations in the bond may be just a correction from the world-is-coming-to-an-end levels seen at the end of 2018, when two-year breakeven rates fell to 0.7 percent, which was the lowest since early 2016. That was a time when there was very real concern about deflation. Some of the questions about whether inflation is a threat may be answered Tuesday, when the government releases its monthly consumer price index report. The median estimate of economists surveyed by Bloomberg is that core consumer prices rose 2.2 percent in February from a year earlier, the same rate as in January.

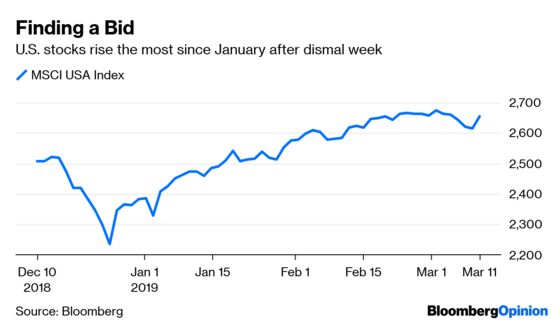

STOCKS HAVE A MARGIN PROBLEM

The stock market shrugged off last week’s malaise, with the MSCI USA Index rising as much as 1.49 percent in its biggest gain since January. Typically, a little bit of inflation is good for equities because it can result in increased revenue. The problem now, however, is that the little extra inflation may not be enough to offset higher labor costs, putting pressure on profit margins. That wouldn’t be much of a problem if profits were actually growing, but they aren’t. Analysts are forecasting that first-quarter corporate earnings will likely fall 3.4 percent from a year earlier, according to DataTrek Research. On top of that, earnings for the second-quarter are only seen rising 0.2 percent, but the way those estimates have been coming down it’s only a matter of time before analysts forecast a drop for that period, too. The strategists at JPMorgan wrote in a research note Monday that on a rolling 12-month average, developed-market profit margins likely peaked around mid-2018. “On balance, it seems likely that margin pressures will build and that the peak of the (developed market) corporate margin is behind us,” the JPMorgan strategists wrote. “There is no free lunch. Limited price inflation may temper central bank normalization, but if wage inflation is rising, corporates will come under increasing pressure.” Since 1960, U.S. margins have peaked on average two years ahead of a recession.

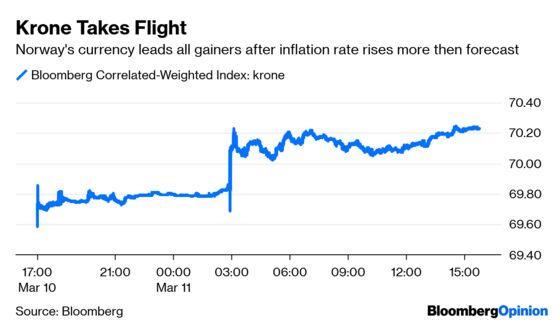

FORGET STERLING. CHECK OUT THE KRONE

The foreign-exchange market was fixated on sterling Monday, as the Bloomberg British Pound Index jjumped 0.83 percent. Fueling the gain were reports that U.K. Prime Minister Theresa May was on her way to Strasbourg, France, for last-minute talks with the European Union, a day before the prime she puts her Brexit deal to Parliament. That’s all very exciting, but the real news in the current market Monday may have been the huge rally in the Norwegian krone. It soared as much as 1 percent in its biggest gain since April 2017 after data showed that a measure of annual consumer-price growth excluding energy costs climbed to 2.6 percent in February, the highest since 2016. Besides adding to evidence that global inflation isn’t dead, the report could bolster speculation that Norway’s Norges Bank might be the only major central bank in tightening mode at the moment. An interest-rate increase this month is a done deal, and another might be in the cards before the year is out. The median estimate in a Bloomberg survey sees the krone rising as much as 5 percent by year-end, outperforming all currencies except the Swedish krona, according to Bloomberg News’s Love Liman. A Norges Bank survey of regional businesses, due for release Tuesday, could be another key piece of data for the krone’s outlook, according to Danske Bank A/S. “If that also surprises positively it would underpin the point that Norway is in a unique position relative to peers,” Kristoffer Kjaer Lomholt, a senior analyst at Danske, wrote in a research note.

BRAZIL TAKES PENSION REFORM SERIOUSLY

Powell’s dovish comments on “60 Minutes” gave a boost to emerging markets, partly because it helped pressure the dollar lower. Given the huge amount of dollar-denominated debt taken out by emerging-market borrowers in recent years, any decline in the greenback has become a green light to buy. And within emerging markets, few benefited as much as Brazil. The Ibovespa’s 2.79 percent gain dwarfed the 1.07 percent rally in the MSCI EM Index. It was a similar story with the real, which appreciated 0.63 percent, compared with a 0.23 percent gain in the MSCI EM Currency Index. Granted, this isn’t solely the result of a weaker dollar. Brazil’s economy actually seems to be picking up. Economists forecast Latin America’s largest economy will grow 2.8 percent next year, up from 2.5 percent one month ago, according to a weekly survey compiled by the central bank. It was the fourth consecutive week that the survey showed an increase in forecasts. The reason for the optimism seems to be centered on progress in much-needed pension reform. In a live event on social media late last week, President Jair Bolsonaro talked about the importance of pension reform, saying Brazil can’t put it off any longer. He emphasized how the economy depends on the approval of pension reform, linking it to the stabilization of accounts, a boost in investments, tax reform and reducing the size of the government. As the “B” in the BRIC acronym that also includes Russia, India and China, any strength in Brazilian markets has the high potential to boost emerging-market investors globally.

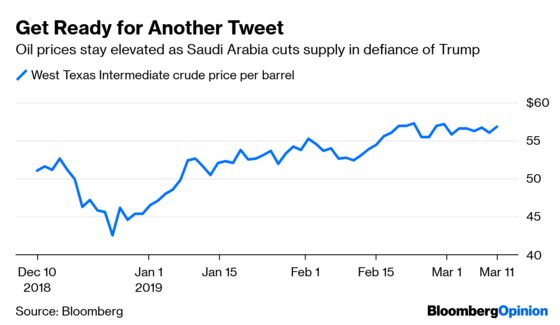

THIS WON’T MAKE TRUMP HAPPY

It’s been two weeks since President Donald Trump took to Twitter to warn OPEC that oil prices were too high and to “take it easy” in cutting supplies. Well, oil prices are right back to where they were on Feb. 25, and OPEC seems to be paying no heed to Trump. Saudi Arabia plans to produce well below 10 million barrels a day in April, a Saudi official said over the weekend. Disruptions in Venezuela, Libya and Iran also have tightened supplies, although U.S. production remains at an all-time high, according to Bloomberg News’s Alex Nussbaum and Grant Smith. With plans to export less than 7 million barrels a day, Saudi Arabia will supply clients with significantly less oil than they’ve requested for April, the Saudi official said. The dilemma OPEC faces is whether to suffer through a rout in oil prices that batters their export-dependent economies or defy Trump, who could enforce legislation that shakes the group to its foundations. It’s not an easy decision for Saudi Arabia, as the U.S.’s booming oil production could set the stage for country’s total petroleum exports to surpass those of Saudi Arabia by year-end, according to Rystad Energy AS. The U.S. will add another 1 million barrels a day of crude production in 2019, after last year’s 2 million barrel-a-day increase. That would push push America’s total petroleum shipments to around 9.5 million barrels, Oslo-based Rystad said.

TEA LEAVES

The National Federation of Independent Business’s monthly index of sentiment among U.S. small business owners has suddenly become a can’t-miss data point. Usually a sleepy affair, the release garnered attention last month when it showed that optimism in January slumped to the lowest level since Donald Trump became president in 2016. Also, it was the fifth straight monthly decline. The recent weakness is notable because some strategists think the gauge skewed higher under Trump because small-business owners tend to be Republicans. That’s not easy to prove, but it’s clear that the group’s next report due out Tuesday will be closely watched. The median estimate among economists surveyed by Bloomberg is for the index to gain slightly, to 102.5 for February from 101.2 in January.

DON’T MISS

The Fed Has Given MMT Proponents Ample Ammunition: James Bianco

Keynes Redux? How Lawrence Summers and MMT Align: Tom Orlik

Junk Bonds Are Winning Even When They’re Losing: Brian Chappatta

Don't Underestimate China's Low-Inflation Headache: Daniel Moss

Replacing the Most Important Number in the World: Satyajit Das

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.