(Bloomberg Opinion) -- President Donald Trump did it again Monday, making a statement about the economy so obviously incorrect that this time even the chairman of his Council of Economic Advisers, Kevin Hassett, publicly disowned it. Trump’s claim was that GDP growth (an annualized 4.2 percent in the second quarter) was higher than unemployment (3.9 percent in August) “for the first time in 100 years.” Actually, this has happened 63 times since 1948, most recently in 2006.

Meanwhile, Hassett held a media briefing where he shared a bunch of charts about the economy’s performance that were all factual, as best I can tell, but made some interesting choices of which data to display. Several of them, for example, showed six-quarter compounded annual growth rates, which are not really a thing, and became the source of some amusement on economist Twitter. So did the CEA’s choice of trendlines. (People need to find amusement somewhere, you know.)

Let’s be clear about one thing: The U.S. economy is by most measures doing quite well at the moment, and the president has every right to bask in its glory. He’s not really responsible for everything that’s going well — no president ever is — but the way things generally work in the U.S. is that if you’re in the White House and the economy is growing at a healthy clip, you get the credit. As I wrote a few weeks ago, though, Trump seems congenitally inclined to demand far more credit than the current state of the economy reasonably allows, so he makes ridiculous claims of unprecedented economic success that the mainstream media then spends the rest of the day debunking, while his aides feel compelled to make claims that are less ridiculous but still often dodgy enough to merit criticism.

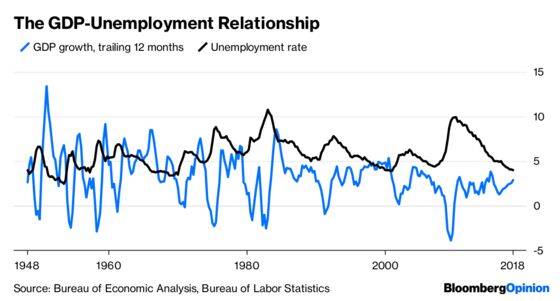

I’m not here to offer more such critical commentary! Instead, I decided to look for a few less-dodgy metrics by which to judge the current economy. First, here’s the president’s own metric of choice from Monday, rendered using the less noisy and thus more meaningful statistic of GDP growth over the preceding four quarters. It actually has become quite rare for four-quarter GDP growth to surpass the unemployment rate — rare enough that it hasn’t happened since the third quarter of 2000 and isn’t happening now:

Comparing GDP growth and unemployment is admittedly an apples-to-oranges endeavor that doesn’t contribute a huge amount to our understanding of the economy. But the early 1950s, the mid-1960s and the late 1990s, when GDP growth surpassed the unemployment rate and stayed there for a while, are generally seen as economic golden ages. If the U.S. economy can get there again — and the trendlines at least look good — that would undeniably be swell.

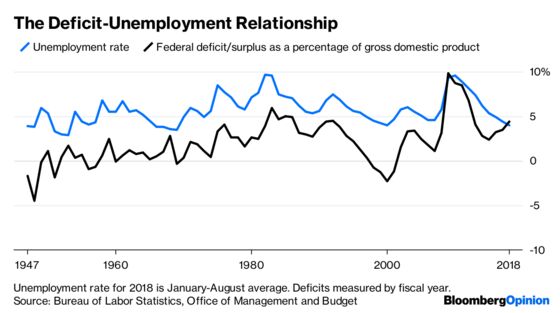

Here’s another fun apples-to-oranges comparison that I also think sheds some light: unemployment versus the federal deficit (expressed as a percentage of GDP). The fiscal year that ends this month looks like it will be only the second on record during which the latter will surpass the former; it surely also happened during the double-digit deficit years of 1942 through 1945, but the unemployment data doesn’t go back that far.

In general, the deficit grows when unemployment rises and shrinks when unemployment falls. That is, the federal government usually stimulates the economy when times are tough and pulls back when the private sector is doing well. Since 2015, though, the deficit has been rising even as employment continues to fall. With last year’s tax cuts and this year’s spending deal in particular, Congress and the president have been providing pro-cyclical stimulus, which is perhaps the single biggest cause of this year’s acceleration in GDP growth.

Is such late-cycle stimulus a good idea for a government with a debt-to-GDP ratio of more than 100 percent? I really don’t know, but I do know there are reasonable people, such as my fellow Bloomberg Opinion columnist Karl Smith, who think the best way to heal the still-deep job-market scars of the last recession is to “run the economy hot.” When I look at a chart like the following one, I’m a little more inclined to agree with them:

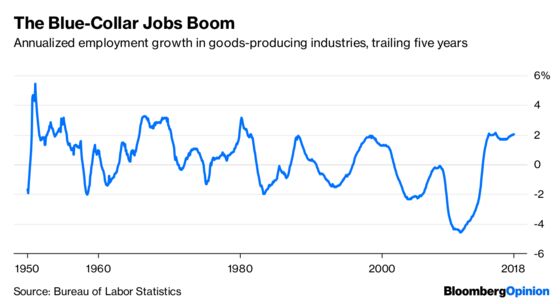

The goods-producing industries are manufacturing, construction and mining (which includes oil and gas extraction). They tend to employ lots of men without college educations, a group that has struggled mightily with the economic changes of the past half century. Hassett featured goods-producing jobs in his slide show on Monday, labeling them “blue-collar jobs” and showing their six-quarter growth rate because that makes it look like there’s been a big takeoff since the November 2016 election. I chose the five-year growth rate because it cuts out a lot of noise and makes clearer how different this expansion has been than the past few. Since early 2010, we have been experiencing the strongest run of goods-producing job growth since the 1960s.

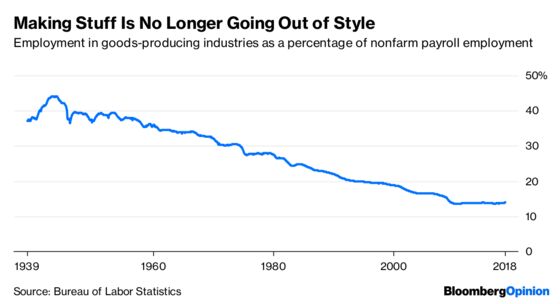

This is, to be sure, partly just a reflection of how far goods-producing employment had fallen during the Great Recession. During World War II, it accounted for as much as 44.1 percent of nonfarm payroll employment; now it’s just 13.9 percent.

But since 2009, that share has stopped falling. That’s … kind of exciting. And while the new trend was already in place during the Barack Obama years, it has gained strength since Trump became president, as has job growth in the rural areas and small metropolitan areas that have struggled most over the past few decades. Which sounds like something worth bragging about.

To contact the editor responsible for this story: Brooke Sample at bsample1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Justin Fox is a Bloomberg Opinion columnist covering business. He was the editorial director of Harvard Business Review and wrote for Time, Fortune and American Banker. He is the author of “The Myth of the Rational Market.”

©2018 Bloomberg L.P.