How to Make Money Out of Misery

The strategy of taking advantage of others’ misery by acquiring brands to sell in his stores is a sensible one.

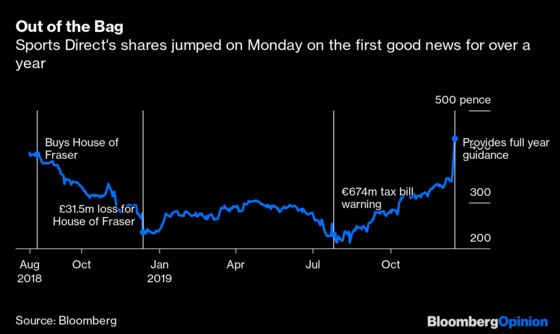

(Bloomberg Opinion) -- Billionaire Mike Ashley has unpacked a haul of good news from his giant Sports Direct bag, the first investors in the sportswear-to-statement jacket empire have enjoyed for a while.

After a dismal showing in July — when Sports Direct International Plc first delayed its full-year earnings statement, and then accompanied it with news it faced a surprise tax bill in Belgium potentially worth 674 million euros ($750 million) — the bar for doing better was pretty low.

But the group seems to be stabilizing after the tumultuous period in the wake of its acquisition of the troubled House of Fraser department store chain in August 2018.

For now, Sports Direct hasn’t split out House of Fraser’s sales and profits. Instead, the storied British chain has been lumped in with the premium lifestyle division, which includes the upmarket Flannels boutiques. In the half year to Oct. 27, the unit made a loss on an underlying Ebitda basis of 5.6 million pounds, compared with a deficit of 29 million pounds in the year-earlier period.

This implies House of Fraser’s losses shrunk noticeably. Tony Shiret at Whitman Howard estimates the loss at about 10 million pounds, compared with 31.5 million pounds previously.

This all led Ashley to declare “green shoots of recovery” at the department store. More importantly, he also had good news for the outlook. The company now expects full-year underlying Ebitda of between 356.4 million pounds and 390.3 million pounds. That’s up by between 5% and 15% — the range the company has historically targeted — from 339.4 million pounds in the year to April 2019, excluding House of Fraser.

Ashley also provided reassurance on the Belgian tax bill, saying that it won’t be such a big problem after all, and should not lead to a material charge. Finally, a 120 million-pound sale and leaseback for Sports Direct’s Shirebook campus has helped to halve net debt, which had been ratcheting up.

The shares rose as much as 27%. But investors shouldn’t get too ahead of themselves. First of all, there is still work to do at House of Fraser. While the group will move forward with a number of stores under the Frasers banner — also the new name for Sports Direct — more outlets will close. Sports Direct must also convince the luxury brands to back his Frasers vision, although this should receive a boost from the Flannels offering. Brands such as Burberry Group Plc were much in evidence at Flannels’ new flagship on London’s Oxford Street.

While much attention has focused on House of Fraser, it and Flannels are still a small part of the group. It is the core Sports Direct sportswear stores that drive the performance. Here sales, excluding acquisitions, fell 8.6%, as Sports Direct took the division upmarket. Revamped stores are performing well, and selling more expensive items, together with less discounting, is bolstering margins. But the group can’t let up the pace of these refurbishments. Ashley will have to convince the big sportswear brands, Nike Inc. and Adidas AG to supply it with their hottest sneakers, just at a time when Nike is becoming more choosey about who it sells to.

And let’s not forget the risk of impulsive action from Ashley himself. The strategy of taking advantage of others’ misery by acquiring brands to sell in his stores is a sensible one. But the dangers of overstretch, as well as unconventional corporate governance moves, are ever present.

Compared to this time last year, Sports Direct has things under more control. Investors will be looking out to see if the same can the same be said of its unpredictable founder.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.