Bill Gross Is a Cautionary Tale for Any Future Bond Kings

(Bloomberg Opinion) -- Six months ago, I asked if “it’s worth stepping back to wonder whether we’re witnessing the end of the line” for Bill Gross. There’s no need to wonder any longer.

Gross is retiring from Janus Henderson Group Plc, the firm announced Monday, more than four years after leaving his perch atop the bond-market world at Pacific Investment Management Co. His stint running the Janus Henderson Global Unconstrained Bond Fund should serve as a cautionary tale for fixed-income investors who think they’re smarter than the rest of the market.

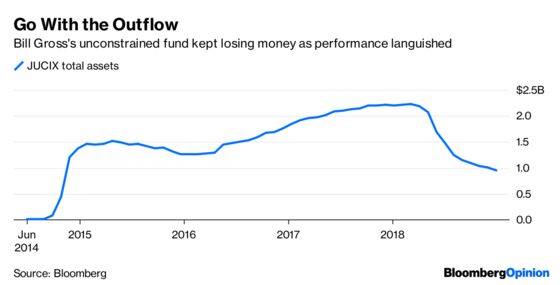

The issue that plagued Gross was that he was too unconstrained for his own good at Janus. His fund topped out at about $2.2 billion of assets — not an insignificant sum, but a far cry from the almost $300 billion that he ran at Pimco. That huge pool of money meant he was the market, which explains why bond traders used to hang on his every word. Being the world’s largest mutual fund also restrained his investing because by and large there wasn’t enough for him to buy aside from the more traditional fixed-income securities.

During his time at Janus, however, he was nimble enough to invest like a hedge-fund manager. He made a big bet on the convergence of U.S. and German 10-year yields at precisely the wrong time, with the Federal Reserve raising interest rates while the European Central Bank remained on hold. The effective duration of his fund somehow fell to minus 4.58 years at one point, even though the prospectus on Janus’s website says the “fund’s average portfolio duration may range from negative 4 years to plus 6 years.” What’s more, it went against what Gross was saying publicly — that the bond bear market would be “relatively mild,” hardly an environment to take a big bet on rising rates. Most recently, he appeared to employ a “merger arbitrage” strategy: a long position in shares of Express Scripts Holding Co. and a short position in those of Cigna Corp.

This experiment didn’t end well for Gross or for those who entrusted their money with him. “The unconstrained strategy Mr. Gross manages has underperformed its three-month Libor benchmark since Mr. Gross joined Janus Henderson in late 2014,” according to the press release announcing his retirement. Just over the past year, the fund fell 4.86 percent. It gained 2.43 percent in 2017 and 5.26 percent in 2016, which trailed its peer group, according to data compiled by Bloomberg. In 2015, when the fund fell 0.43 percent, it did better than its counterparts.

Gross, for his part, seems to understand that he may have miscalculated with his unconstrained fund.

“Maybe I should have stuck to total return and been a little more constrained,” he said in an interview with Tom Keene on Bloomberg Television. He said he managed some total return accounts at Janus and they outperformed “like the old days.”

Gross said that the idea of total return investing, in his mind, was “based on measured risk taking.” He didn’t heed that advice, and that was his downfall. He seemed contemplative during the interview with Keene, comparing his big bet on Treasuries versus bunds in terms of blackjack, saying he put too many chips on the table with that trade. Of course, Gross was briefly a blackjack success in Las Vegas — turning $200 into $10,000 over four months, raising the tuition for his MBA at UCLA — which only added to his mystique as a bond savant.

By now, it should be clear that there is no such thing. Not when a fund manager is able to “go anywhere,” unshackled by any sorts of guidelines or parameters. Gross learned that the hard way. After all, much of his own money was at stake. Anyone else who wants to stake their reputation on running an unconstrained strategy — or investing in one — should do so at their own risk.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.