(Bloomberg Opinion) -- A few years ago, with funding for startups surging, some people worried that the U.S. was in the midst of a new technology bubble. Calmer heads realized that even if venture capitalists were being a little too carefree with their cash, the result probably wouldn’t look anything like the dot-com bubble and crash of 2000. Price-to-earnings multiples for public tech companies weren’t historically high. The funding in the private markets was unlikely to turn into a speculative mania and subsequent bust, because of the difficulty of selling stock in a private company after investing. And since retail investors — the proverbial Main Street — weren’t heavily invested in startups, any drop in valuations was unlikely to spill over into the broader economy.

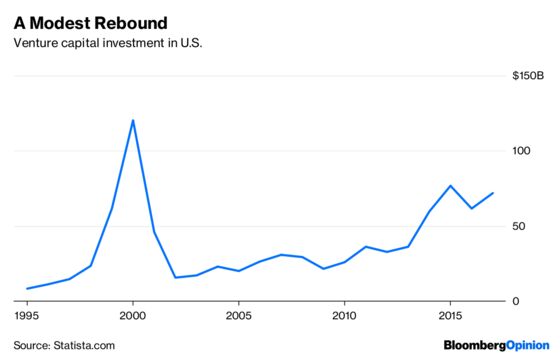

Events bore out these calm predictions. Venture funding did fall modestly in 2016, consistent with the idea that financiers had been mildly overoptimistic in the preceding years:

There were few big failures (excepting the occasional revelation of fraud), and the public stock markets powered ahead. Venture financing recovered in 2017 to a level approaching its 2015 peak, driven partly by interest in new technologies like machine learning.

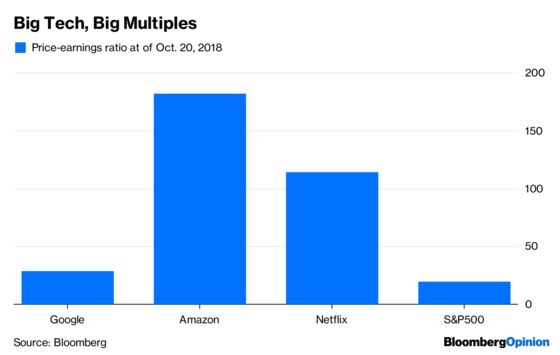

But as the tech sector recovers, there are now a few troubling signs. Some big public tech companies are pretty richly valued:

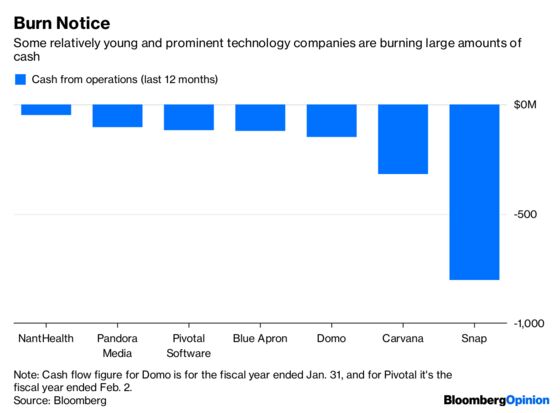

Tesla Inc., a big tech company that went public in 2010, doesn’t make a profit, and so it doesn’t have a P/E ratio. But many believe it to be optimistically valued, especially in light of its recent financial, legal and production troubles. Meanwhile, a lot of young tech companies are burning huge amounts of cash:

Another private tech whale may be set to enter the public markets: Uber Technologies Inc., the ride-hailing company, is talking about doing an initial public offering. Some investment banks have suggested the company could be valued at as much as $120 billion in an IPO, despite never having been profitable, having negative free cash flow, falling behind in the race to develop self-driving cars and being unable to push its chief rival Lyft Inc. out of the market.

Of course, it’s impossible to know whether valuations are justified just by observing that they seem high. Alphabet Inc. (Google), Amazon.com Inc., and other big tech companies might continue their run of growth for decades more. Tesla might overcome its production problems, Snap Inc. might figure out how to monetize its product, and Uber might recover momentum in the self-driving race or finally force Lyft to fold. If every business shifts to software, and a few giant tech companies continue to dominate (without undue interference from antitrust authorities), they might be able to extract oligopoly profits from a huge number of markets at once. If tech eats the world, every investor will need to have a piece of it.

But if things go wrong, there could be a crash. As more big private tech companies go public, both the danger of a bubble and the danger of real economic fallout from a bust will be higher than they were a few years ago.

Public markets are much more liquid than private ones. That means it’s easier to sell stock. If lots of investors decide that tech shares are overvalued, they might buy at inflated prices on the assumption they can sell the stock at even loftier valuations. With everyone pouring money into tech, it can be very easy for investors to convince themselves that a so-called greater fool is out there. This sort of speculative process is behind many theories of why asset markets occasionally escape the pull of rationality, as they did in 1999 and early 2000.

Public markets are also open to many more investors than private ones. This means that normal Americans, whether via their pension funds, 401(k) plans or individual stockholdings, will be exposed to a tech bubble if it does occur. Any ensuing crash would then hit their nest eggs, causing them to cut spending and send consumption lower. A recession would probably be the result.

Of course, calling a crash is almost impossible. Even if tech-company valuations are already inflated, they could easily become more so in the years to come, especially if a slowdown in China leads capital to flee to the U.S. Ironically, the first people to see bubbles forming often find it difficult to profit from them, since betting against a mania can cause you to go bankrupt if the bubble keeps growing for a while. As investor and economist John Maynard Keynes is said to have remarked, “Markets can remain irrational longer than you can remain solvent.”

So although no one knows whether a new tech bubble really is about to form, prudence would dictate keeping an eye out for one. Investors who may have paid little attention to tech company fundamentals need to take a closer look at valuations and rigorously examine the assumptions necessary to justify them. And regulators should carefully track international capital flows to be on the lookout for a flood of dumb or desperate money piling into U.S. tech.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.