(Bloomberg Opinion) -- Must a safer banking system inevitably be less dynamic? Judging from the experience of the U.S. and Europe since the 2008 financial crisis, not necessarily.

Bank executives typically portray efforts to shore up the financial system as a trade-off, in which greater resilience means less of something good. They often warn, for example, that requirements to increase capital buffers will starve the economy of much-needed credit.

Many academics don’t buy it. They note that capital, also known as equity, isn’t some kind of untouchable rainy-day fund. It differs from debt in that shareholders have signed up to bear the brunt of any losses, which is why banks with a lot of it can weather crises better. Other than that, it’s money that banks can lend and invest. More of it should mean more credit.

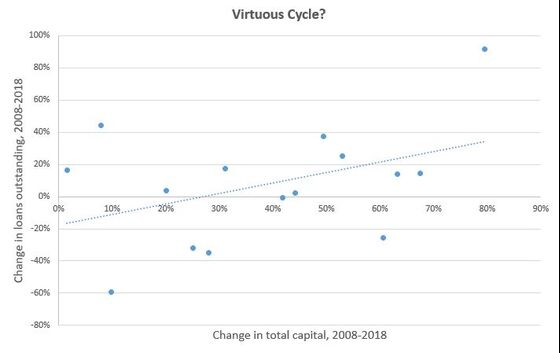

So who’s right? Is capital good or bad for lending? One way to get a sense: See how banks behave when someone actually requires them to have more equity. As it happens, that’s precisely what regulators in the U.S. and Europe did after the 2008 crisis. Now, 10 years later, there’s ample data to assess how things played out. Here’s how capital and lending changed in the U.S. and 14 European countries from late 2008 to late 2018:

The picture is a little messy. There are some cases where capital increased and lending shrank. For the most part, though, countries with larger capital increases more also saw more loan growth. Specifically, a simple statistical analysis — known as a regression — suggests that a 1 percent increase in capital was associated with a 0.7 percent increase in lending.

To be sure, the causality could go both ways. Maybe better economic conditions in certain countries facilitated lending and boosted profitability, allowing banks to meet higher capital requirements more easily. One way to test that: See if the countries with stronger economic growth also had bigger equity increases. They didn’t. There was no significant relationship.

This is far from a full and scientific treatment. That said, it’s consistent with other studies showing that, while capital increases might temporarily impair lending, banks with more equity tend to lend more throughout the economic cycle.

Why, then, don’t banks have more? For one, in good times, more debt — or leverage — magnifies measures of profitability used to assess executives’ performance. Also, debt is cheaper than equity, because it enjoys tax breaks and — in the case of big, highly leveraged banks — because governments have tended to bail creditors out in times of distress.

In other words, banks have private incentives to fund themselves in ways that are not in society’s best interests. It’s a force that regulators must do more to counteract.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Whitehouse writes editorials on global economics and finance for Bloomberg Opinion. He covered economics for the Wall Street Journal and served as deputy bureau chief in London. He was founding managing editor of Vedomosti, a Russian-language business daily.

©2019 Bloomberg L.P.