(Bloomberg Opinion) -- It’s about the workers, not their shelter.

Despite angst about lower Australian home prices and their impact on the economy, consumer spending and the labor market are more important in the eyes of the central bank. That’s the gist of a speech Wednesday by Reserve Bank Governor Philip Lowe.

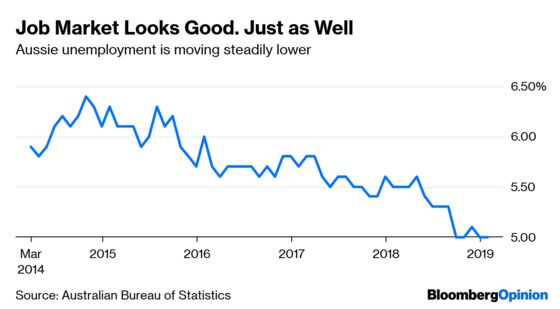

The job scene is pretty solid and Lowe, like his counterparts in much of the world, is banking on that translating into wages and a bit more inflation. Amen. Inflation is too low and, given the length of the expansion and benign levels of unemployment, prices just aren’t taking off. Makes you wonder what it will take for that to happen.

Lowe’s address was typically thoughtful and the most interesting of a trilogy of key economic readings within 24 hours. The two others were the RBA’s monthly decision on interest rates and the release of numbers showing slackening growth in late 2018.

In his remarks, Lowe drew on a paper on the housing slump that the RBA reviewed at its February board meeting. I chastised the bank here for not making a document of such interest freely available. That Lowe devoted a large part of a speech to it is commendable. (The RBA says board papers aren’t public documents.)

Yes, the housing slide is an issue. Solo, it won’t unmake the almost three-decade Aussie growth run, says Lowe. And by making housing affordable for many people, the declines will have some societal benefit.

What’s implicit here is that Lowe’s use of “manageable” to describe the slump doesn’t preclude a shift in policy if the consumer and labor market don’t behave as envisaged. Or even if they look a bit wobbly.

When an economy is at an inflection point, small deviations in models can mean a lot. We do seem to be at such a point. The RBA is studiously neutral on its next step in rates, which could go up as much as down. But this itself is a fairly recent change. Until this year, a climb seemed more likely than a descent. Seasoned RBA watchers foresee cuts. In response to a question after his speech, Lowe conceded that it’s hard to picture a scenario this year where he would nudge rates higher.

Unspectacular gross domestic product numbers, published a few hours after his speech, underscore the risk. The economy Down Under expanded 2.3 percent from a year earlier, compared with a 2.6 percent estimate. Construction took a hit — not a shock, given housing travails — and consumption hung in there.

A lot is hanging on consumption, and the employment that can spur it. Australians’ views of their future income — tied to jobs and pay — count for more than the household wealth effect of bricks and mortar.

“A strong labor market is the central ingredient in the expected pick-up in inflation. We are expecting that as the labour market tightens, wages growth will increase further. In turn, this should boost household income and spending and provide a counterweight to the fall in housing prices. The pick-up in spending is, in turn, expected to put upward pressure on inflation.’’

If there’s an issue with inflation right now, it’s that it isn’t going anywhere. It’s not a leap to see the risk manager deep inside most central bankers stirring in Martin Place, Sydney.

Things will probably be fine. But would you bet on inflation? Or take out a little insurance just in case?

The RBA is edging toward the latter.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.