Sanders, Ocasio-Cortez Chose the Wrong Interest-Rate Cap

(Bloomberg Opinion) -- Representative Alexandria Ocasio-Cortez and Senator Bernie Sanders have called for new legislation to cap credit-card interest rates. It’s not necessarily a bad idea, but there’s a better way to do it.

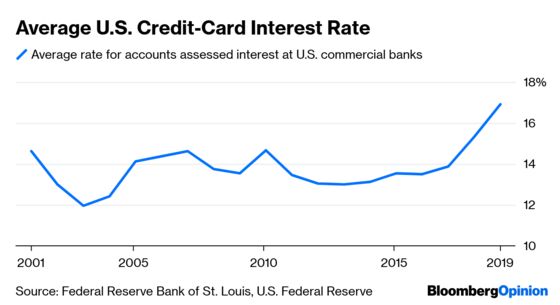

The legislators’ proposal would impose a 15% ceiling on rates. This probably wouldn’t crush the U.S. credit card industry, where the average rate on interest-bearing accounts is around 17%:

But some card plans do charge higher rates, and these would be banned. Meanwhile, if interest rates in general were to rise, the law would prevent credit card rates from rising with them.

The debate over interest is not a new or unusual one. The Bible contains many passages urging people not to charge interest on loans, and almost every religion has some sort of anti-usury provision. In the modern world, interest-bearing loans are extremely common, but governments still often set caps on the rates that can be charged for certain types of borrowing, especially for consumer loans. In the U.S., anti-usury laws have so far been left to the states, though credit cards and banks can get around this by charging the highest rate allowed in the state where the company is incorporated (usually South Dakota, Nevada, or Delaware).

The justification for rate caps comes from behavioral economics. The idea is that people overestimate their ability to pay back loans, and end up getting trapped into a cycle of debt. There is evidence to back up the theory — for example, access to payday loans tends to make poor people worse off financially. Restricting these loans is therefore a form of benevolent paternalism.

But payday loans may be a special case. Americans use credit cards for lots of things — to help finance a new business, to get through periods of unemployment, to pay a surprise bill. Restricting interest rates could cause credit card companies and banks to pull back on this sort of lending, making it harder for Americans to borrow in a pinch. That could end up undermining financial security. Researchers at Policis, a development consultancy, argue that many families have an “irreducible need” to borrow, and are therefore hurt by credit limitations.

To find out whether people overall would benefit or lose out from rate caps, it helps to look at the evidence from other countries. A 2014 report by World Bank economists Samuel Maimbo and Claudia Henriquez Gallegos surveyed anti-usury laws around the world and found that most such laws use a relative rate that can fluctuate with general credit conditions. In other words, laws that simply pick a number — like the one being proposed by Ocasio-Cortez and Sanders — are rare, and occur mostly in Africa.

Looking at the history of these laws and the events that followed, Maimbo and Henriquez Gallegos conclude that when rate caps are set well above the market rate, the effect tends to be benign — only lenders who charge very high rates, and are hence likely to prey on the vulnerable, are shut out of the market. But Maimbo and Henriquez Gallegos find that when caps are set below the average market rate — as Ocasio-Cortez and Sanders’ bill would do if enacted today — credit availability generally worsens in some way.

A recent paper by economists Jose Ignacio Cuesta and Alberto Sepulveda helps quantify the potential effects. The authors look at reforms in Chile between 2013 and 2015 that lowered rate caps on small-sized consumer loans by between 17 and 24 percentage points. They found that the reform did lower interest rates by about 2.6 percentage points, and borrowing fell by 19%. For riskier borrowers, the drops were a bit larger.

The drop in rates seems unambiguously positive. But the drop in lending could be good or bad — good if it represents fewer people taking out loans they don’t need and can’t afford, and bad if it means people aren’t able to borrow when they really need to.

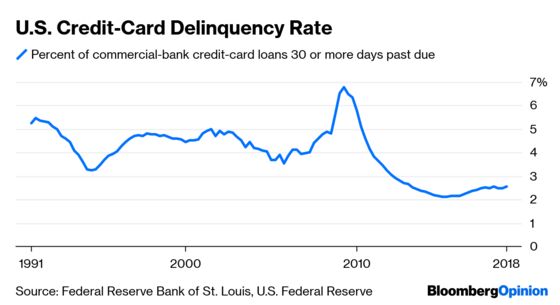

So are Americans overall using their cards wisely, or borrowing when they don’t need to? Since the financial crisis, the delinquency rate on credit card debt in the U.S. has fallen substantially:

This suggests that many people are using their credit cards responsibly, as a way of smoothing out the bumps in their economic lives. That’s not good news overall, of course — the fact that people are forced to rely on borrowing means that their lives are turbulent and their savings are thin. But it suggests that instead of cutting people off from credit cards, a better solution is to let them borrow while addressing the root causes of their insecurity — big health care bills and stagnant wages.

The balance of evidence suggests that Ocasio-Cortez and Sanders should take a different approach to regulating consumer finance. They should set the interest rate cap higher — perhaps at 25% to start — and allow it to fluctuate based on market interest rates. That would target the most exploitative lenders while allowing the bulk of Americans to borrow when needed.

To contact the editor responsible for this story: Mark Whitehouse at mwhitehouse1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.