(Bloomberg Opinion) -- Amundi SA, Europe’s biggest independent fund manager, saw customers withdraw money for a third consecutive quarter in the three months through June. It’s far from the only asset manager suffering outflows. And as the drumbeat of reports and research questioning portfolio managers’ claims to beat the market grows ever louder, the reluctance of clients to commit funds is completely rational.

Halfway through the 36 pages of slides Amundi published along with its results on Wednesday is a data set entitled “Solid Performances.” There is another – less Panglossian – way of reading the numbers.

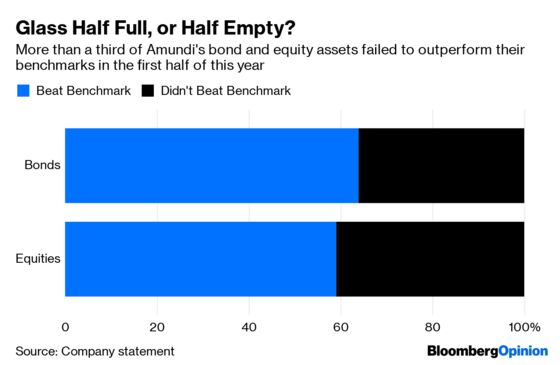

One of the slides purports to argue that 64% of the firm’s fixed income assets and 59% of its equity holdings outperformed their relevant benchmarks in the first half of this year. I’d argue that customers should read those figures the other way around; that more than a third of Amundi’s bond bets and almost half of its stock picks fared no better than their respective indexes.

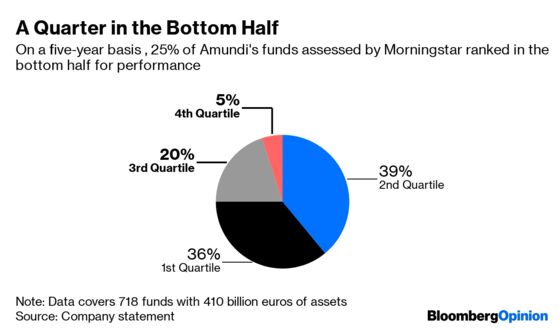

Similar skepticism is justified with respect to how Amundi’s performance ranks against that of its peers. On a five-year basis, for example, the firm highlights that 75% of its funds ranked in the top two quartiles for performance as measured by research firm Morningstar. Or, alternatively, the figures show that a quarter of its funds languished in the bottom half – hardly a terrible performance, but still suggesting a one-in-four chance that you’d have been better off buying an index tracker.

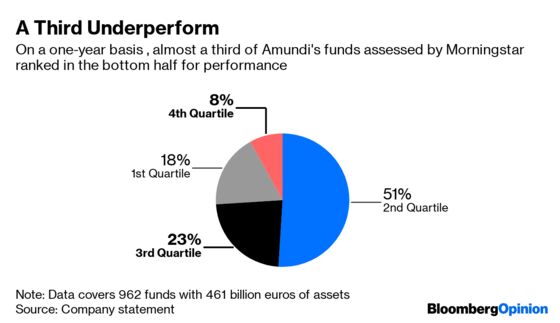

On a shorter timescale, its performance has become even less impressive, depending how you look at it. On a one-year horizon, almost a third of Amundi’s funds were in the bottom two quartiles.

And all of these figures are calculated before fees. Having a 69% chance of beating the benchmark over the course of a year, depending which Amundi fund you chose, doesn’t seem like disastrous odds – until you include those fees, which erode your returns.

None of this is to single out Amundi for criticism. The entire fund management industry uses similar marketing methods, and arguably the French firm’s five-year performance is still impressive. But it is far from the only asset manager to suffer outflows. Janus Henderson Group Plc said on Wednesday that it suffered a seventh consecutive quarter of withdrawals in the second quarter, while Man Group Plc, the world’s biggest publicly traded hedge fund, saw net outflows of $1.1 billion in the first half of this year.

The European asset management industry in general has seen “virtually zero net inflows” so far this year “given the persistent wait-and-see approach from savers and investors resulting from strong risk aversion,” Amundi says.

I’d add a caveat to that. As more customers question the value that active managers claim to be able to add to investment strategies, the industry faces an existential crisis. Even if surging markets restore investor faith in the outlook, low-cost index-tracking funds will capture more of their money.

At least Amundi has a hedge against that trend; its passive business attracted almost 7 billion euros ($7.8 billion) of assets in the first half of the year, growing assets under management in exchange-traded and smart beta funds to 114 billion euros. For fund managers that don’t offer those products, the future looks increasingly bleak.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.