America Needs to Revive the American Dream of Homeownership

(Bloomberg Opinion) -- The idea of helping the lower-middle class by using the federal government to encourage homeownership is, to put it mildly, out of favor. There’s a popular narrative that the housing bubble of the 2000s — and, by extension, the financial crisis and the Great Recession — were caused by the government making or encouraging cheap loans to low-income Americans. That narrative is a myth — the leading cause of the bubble was private banks making bad loans, mostly to speculators rather than to low-income owner-occupants. But the myth is unlikely to die, meaning that it will be an uphill battle to convince recession-scarred Americans to support the idea of expanding homeownership.

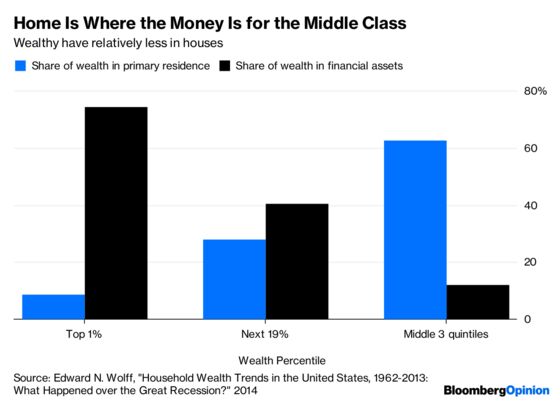

That’s a shame, because for all its drawbacks, homeownership is still a crucial source of wealth for everyone who isn’t rich:

There are big obstacles to building wealth for many Americans. Stocks — the obvious alternative to real estate — can be extremely volatile, and lower-middle-class people can’t afford to run the risk of having their assets wiped out. Stocks are also difficult to understand; people who try to invest their own money tend to do very badly, and people who use professional managers to invest for them tend to pay large fees that swamp their returns. This keeps low-income people out of the market.

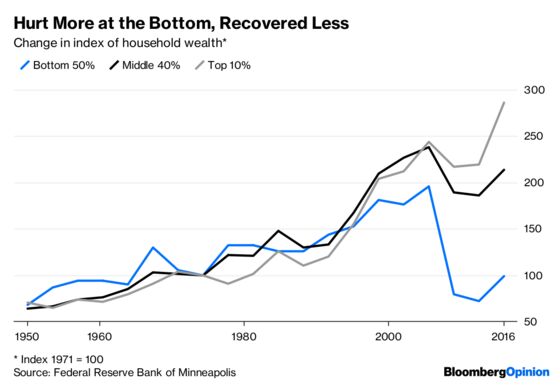

Housing certainly has its own disadvantages — it’s undiversified, and it can tie people to the economic fortunes of a specific location. But despite the occasional market downturns, housing tends to be a pretty good long-run investment. If lower-middle class wealth is to be rebuilt without resorting to something like a social wealth fund, there are few better alternatives to housing. And lower-middle class wealth desperately needs rebuilding:

Housing also has benefits that can’t be counted in dollars. Although housing is an important part of the economy and the largest financial asset of most homeowners, it’s also a form of social equity. Good school districts tend to be in communities full of single-family homes with little rental housing, and homeowners often are more involved in local government than renters, giving them the power to structure their communities to suit their interests. Because local control over schools and land use is so entrenched in American society, it will be difficult to give renters anything close to equal opportunity in America without giving them a path toward homeownership.

Homeownership can also encourage low-income people to build more wealth on their own. Monthly mortgage payments can act as a behavioral nudge that prompts people to save more each month. And homeowners have an incentive to maintain their dwellings, which both improves the quality of the housing stock and helps teach people the basic skills of property management.

If the government is to expand homeownership, it should do so in a way that avoids the mistakes of the bubble period. Previous policies often made it easier for lower-income Americans to borrow money in order to buy houses. But this loaded them up with debt and put them at risk of default — similar to government encouragement of student loans. Instead of repeating this mistake, the government should give low-income grants to put equity into homes.

Several programs like this already exist. The Department of Housing and Urban Development allows families that qualify for housing vouchers in some areas to use them to help purchase homes and pay ownership expenses instead. First-time homebuyers are eligible for a tax credit. HUD also used to administer the AmeriDream down-payment assistance program, but the policy never reached many people and was discontinued in 2008.

These programs, or similar ones, would form the foundation of a broader policy to encourage lower-middle class homeownership and equity building. They would ideally be expanded to cover more areas and more people, and cover more housing costs. The increased expense could be funded by federal wealth taxes or inheritance taxes, perhaps with some contribution from local property taxes or land value taxes. This would amount to a form of direct wealth redistribution — a worthy attempt to fight the inexorably increasing wealth inequality that has caused much consternation in recent years.

But the program would need one more element to make it work — new housing construction. If low-income homebuyers use their government grants to simply bid up the prices of existing homes, the result will be a transfer of money to existing homeowners, not to new homebuyers. Again, the analogy with student loans — which allowed colleges to simply increase their tuition rather than provide more spots for prospective students — is apt.

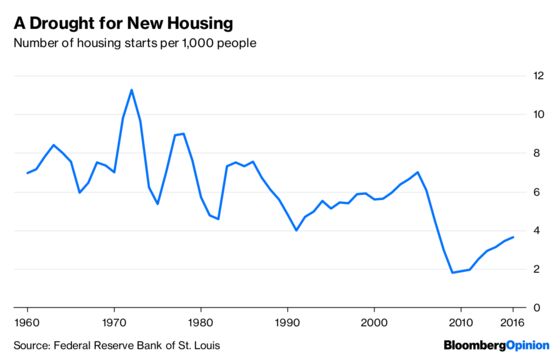

The solution is for the government to make these grants conditional on cities building more housing units. This would be a powerful financial incentive; if a city is willing to increase density and to allow the construction of more multifamily housing, it would receive more federal money in the form of home-equity assistance. If combined with more direct incentives for dense development, would help combat the nationwide housing shortage that has persisted since the crisis:

So a government homeownership program would have to look very different from the efforts of the past. Giving low-income Americans grants to buy new houses, rather than lending them money to buy old ones, would be a wiser path to rebuilding the American Dream.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He is a portfolio manager for New River Investments in Atlanta and has been a contributor to the Atlantic and Business Insider.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.