(Bloomberg Opinion) -- I bumped into a couple from Denver the other day who were spending a long weekend in New York City. We got to talking, and I asked them whether they read the Denver Post.

“No,” the man replied. “A hedge fund bought it and destroyed it.”

“It’s that bad?” I asked.

“There is nothing in it,” said the woman. They went on to tell me that, like many Denverites, they now relied on the Colorado Sun for their local news. The Sun is a journalism website started by former Post reporters and editors.

I suppose I don’t need to tell you which hedge fund the couple was referring to. Yes, it’s Alden Global Capital LLC, whose newspaper company, MNG Enterprises Inc., has mastered the art of maintaining profitability by cutting staff, and then cutting staff again as readers stop buying the diminished product. And then doing it again … and again … until all that’s left is a shell. The Denver Post business model, you might call it.

In an effort to perpetuate this model, Alden Global and its president, 39-year-old Heath Freeman, made a $1.36 billion bid for Gannett Co., the largest publicly traded newspaper chain in the country, a few months ago. After Gannett rejected the bid, Alden Global started a proxy fight, hoping to install its own slate of directors.

We’ll get to that proxy fight in a moment, but first, let’s take a look at some of the other things Alden Global has been up to lately.

There’s the Payless Inc. liquidation, for instance. Alden Global became the majority shareholder when the discount shoe retailer emerged from bankruptcy in 2016. What normally happens in such situations is that the new owner installs new, improved management, and goes forward with a plan to return to profitability.

That does not appear to have happened with Payless, which was bankrupt again less than two years later. This time, it’s not reorganizing; it’s liquidating its 2,500 U.S. stores. At a hearing in February, a lawyer for the company’s creditors told the court that Alden Global had either not replaced departed executives or replaced them “with incompetent Alden personnel,” according to Bloomberg News.

More recently, a committee of unsecured Payless creditors has complained that Alden Global is maneuvering to do what hedge funds and private equity guys invariably do when one of their companies is going down the tubes: make sure they get paid before anyone else. According to Bloomberg Law, the committee told the bankruptcy court that Alden is “seeking to deplete assets that should be available to pay unsecured creditors, most vendors and suppliers who are owed about $225 million.”

There’s trouble too at Fred’s Inc., a middling pharmacy chain in the southeastern U.S. that became Alden Global’s biggest investment in 2016. A few years ago, Freeman told a Duke University publication — did you know he was once a field goal kicker for the football team? — that his fund focused on “opportunistic and distressed investing.”

Indeed, when Freeman started buying Fred’s it must have seemed like he truly had found a value stock; Alden Global paid, on average, $12 a share for a stock that was down from $20. But Alden Global has done pretty much nothing right, causing the stock to fall to $1.38 by last June. Freeman is now the chairman of the board, and the chief executive is the well-known pharmacy executive Joe Anto. Just kidding! Prior joining Fred’s early last year, Anto was a senior vice president at MNG Enterprises. His job was to identify the newspapers that Freeman could then buy and pillage.

It looked for a while this year like Fred’s was finally moving in the right direction. The stock got as high as $3.29. But last week, Fred’s announced its annual report wouldn’t be ready on time. Why? Because it is closing 159 stores and needs more time to assess the effect on its bottom line. It also revealed that its net loss for 2018, when the annual report does come out, will be $144.5 million. Fred’s closed Tuesday at $1.67.

Freeman hasn’t bought any newspapers recently, but that doesn’t mean his newspaper company hasn’t been in the news. Last week, the Washington Post reported that Alden Global was being investigated by the U.S. Labor Department for moving “nearly $250 million of employee pension savings into its own accounts in recent years.”

It’s a little hard to know what to make of this news. An Alden Global spokesman says that the firm “successfully” managed the pension money for a short time, that it has since either paid it out to pensioners or returned almost all of it, and that it did nothing to violate the law. The Post raised the possibility that Alden Global might have used some of the money to purchase the Orange County Register in 2016 — which would be against the law — but the spokesman insisted in an email that that didn’t happen.

The Post also suggested that the inquiry “could become a factor in Alden’s effort to acquire” Gannett. Of this I have no doubt. Gannett has made it clear it has no interest in being bought by Alden Global’s newspaper company, and it is using every bit of ammo at its disposal to repel Freeman and his allies.

On the one hand, the Alden Global bid can seem like a joke. The firm can’t afford to make the bid without a partner to put up the money — and it has yet to find one. Instead it got another hedge fund, Oaktree Capital Management LP, to issue a letter saying it was “highly confident” that Alden Global will be able to come up with the money. Where this confidence comes from is unclear, because Oaktree apparently has no plans to put in its own money. Gannett has mocked the letter, and rightly so.

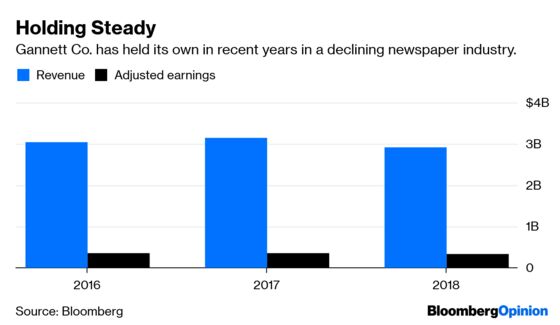

On the other hand, Alden Global owns 7.5 percent of Gannett’s stock. And it’s running a proxy contest, putting up six possible directors, including Freeman himself. All things considered, Gannett has performed pretty well in recent years given that Warren Buffett believes most newspapers are “toast”: Since 2016, its revenue, adjusted earnings and earnings per share have pretty much held steady. But investors are rarely satisfied with “steady.” The idea that Alden Global would apply its ruthless approach to boost Gannett’s stock price could appeal to antsy Gannett shareholders.

Gannett is counting on two things to win the proxy fight. The first is Alden Global and Freeman’s record of corporate ineptitude, which it hopes will scare shareholders. The second is that there are enough people, including its own shareholders, who believe that journalism has a value that goes beyond profits. That local newspapers are a critical part of our democracy. And that the Alden Global model is damaging not just newspapers and their employees, but also the country.

All will soon become clear, when Gannett holds its annual meeting on May 16. I wouldn’t miss it for the world.

So far I can tell, this is the only interview Freeman has ever granted.

To contact the editor responsible for this story: Stacey Shick at sshick@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Joe Nocera is a Bloomberg Opinion columnist covering business. He has written business columns for Esquire, GQ and the New York Times, and is the former editorial director of Fortune. He is co-author of “Indentured: The Inside Story of the Rebellion Against the NCAA.”

©2019 Bloomberg L.P.