(Bloomberg Opinion) -- Don’t be fooled: The economy is still slowing down.

The White House on Friday seized on surprisingly strong real GDP growth of 3.2 percent in the first quarter as unalloyed good news, and on some level it’s right: It’s better to have more growth than less. Look beyond the headline number, however, and there’s cause for concern.

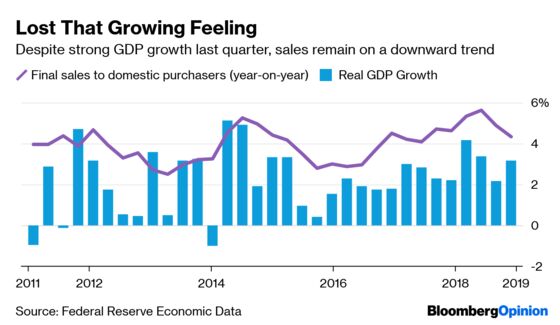

Sharp observers noted that GDP was boosted by an increase in inventories and exports, two traditionally volatile sectors. Underlying consumer demand was weak. Just as important, inflation is continuing to slow, indicating that businesses don’t feel sales are strong enough to support price increases.

All these concerns can be combined into a single statistic: year-over-year growth in final sales to domestic purchasers. It measures how much U.S. consumers, businesses and governments (local, state and federal) are spending relative to the same period last year. It isn’t adjusted for inflation, which makes it an especially useful tool for judging how much total demand there is in the economy. Greater demand can show up either as more real growth or as more inflation, and this statistic captures both.

So: How is it doing?

Sales had been trending upward since late 2016, reflecting two things: the recovery of the U.S. fracking industry and the anticipation (and eventual passage) of a tax-cut bill. They peaked, however, late last year and are now falling.

There are several reasons for this trend: The boost from the tax cuts, which juiced consumer spending, is wearing off. A long-lasting increase in business investment has failed to materialize, probably due to the uncertainty created by the ongoing trade tensions. Finally, and most important, the Federal Reserve has raised rates eight times since 2016 in an effort to head off inflation.

That inflation never materialized, and now overall U.S. demand is weakening. Next quarter is almost certain to be worse, and unless something surprising happens, the quarter after that will be worse still.

The upshot is that, despite last quarter’s surprisingly high GDP numbers, the economy is far from healthy — and in fact, a recession late this year or early next remains a live possibility. Congress and the Fed should both be looking to stimulate growth now, by completing tax reform and cutting interest rates. A more long-term response will require more fundamental change in both institutions.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a former assistant professor of economics at the University of North Carolina's school of government and founder of the blog Modeled Behavior.

©2019 Bloomberg L.P.