Blowout Saudi Bond Deal Sends a Message to Markets

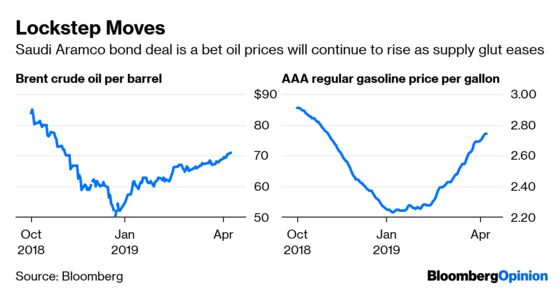

(Bloomberg Opinion) -- Saudi Arabia on Monday began offering $10 billion of bonds of Saudi Aramco, the world’s largest oil company. Most of the focus was on how investors submitted orders for about $60 billion of bonds. Even if you are (rightly) skeptical of “order books” and think the true demand was for half that amount, it’s still a remarkable development for a country that just a few months ago was being ostracized for its role in the killing of Washington Post columnist Jamal Khashoggi. But there’s more to the story.

In essence, the high demand is a referendum on the oil market. Investors are really looking to jump into the deal because they think that oil prices, which are up more than 50 percent from the lows in December, are headed much higher. Rising oil prices are generally not a problem for markets during times of economic strength, but the majority of analysts expect weaker growth, with the Organization for Economic Cooperation and Development having just slashed its global forecast for this year to 3.3 percent from a previous estimate of 3.5 percent. Higher crude prices could act as a further drag on the economy and weigh on riskier financial assets. In the U.S., for example, prices for a gallon of regular grade gasoline have risen to an average of $2.74 heading into the all-important summer driving season, according to the Automobile Association of America, up from January’s low of $2.23 a gallon. Prices are in sight of the $2.90 a gallon seen in early October right before personal spending took a dive and equity markets collapsed. Some might say that higher oil prices indicate an economy that isn’t as bad as thought, but the reality is they probably have more to do with a decline in the supplies, thanks to OPEC.

OPEC and its partners, which pump about half of the world’s oil, have been successful in cutting in production to get oil back to near the levels they need to cover government spending, according to Bloomberg News’s Grant Smith. On top of that, there’s now concern that an escalating conflict in Libya, whose oil is prized for its quality, could cause crude supplies to tighten further. “The expectation that the tightened supply picture is going to boost prices is starting” to gain traction, said Gene McGillian, a senior analyst at Tradition Energy, according to Bloomberg News.

BOND BULLS FACE CRITICAL WEEK

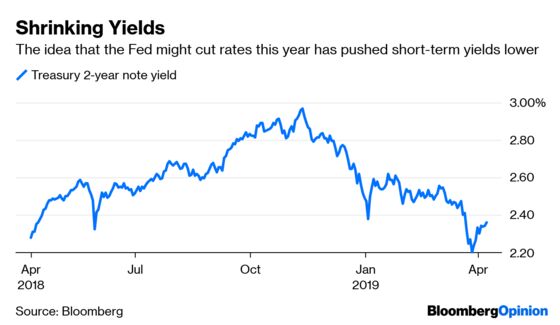

Perhaps it was the potential negative effect of rising oil prices on the global economy that prompted bond investors to step up at the U.S. Treasury Department’s auction of super-safe bills on Monday. The offering of $42 billion of three-month bills attracted bids for 3.07 times the amount offered, the most since January. The offering of $36 billion in six-month bills generated a so-called bid-to-cover ratio of 3.14, the highest since February. Relatively high-yielding cash equivalents such as Treasury bills should see demand in an uncertain economic environment like the one the U.S. currently faces. Plus, the market is pricing in about a 100 percent chance that the Federal Reserve will cut interest rates by 25 basis points this year. Regardless, this is a big week for the world’s most important market. Besides the regular bill auctions, the Treasury Department will offer $78 billion in three-, 10- and 30-year notes and bonds. In addition, the government on Wednesday will release the monthly Consumer Price Index report for March — which is forecast to show faster inflation, in part because of rising oil and gas prices — and the Fed will release the minutes of its March monetary policy meeting the same day. “For the market to begin pricing in a hike, we will need to see persistent inflation pressures,” said Noelle Corum, a portfolio manager in the fixed-income group at Invesco Advisers Inc., according to Bloomberg News.

A PRUDENT STOCK BEAR’S WARNING

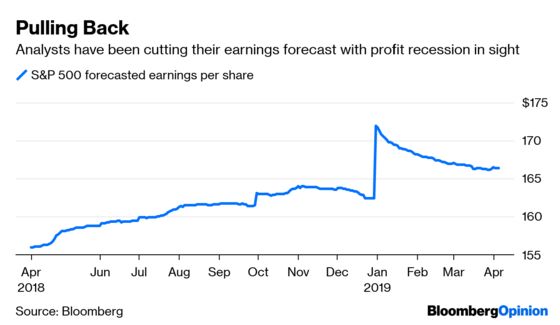

In the second and third quarters of last year, when U.S. stocks were flying higher, Morgan Stanley chief U.S. equity strategist Michael Wilson wasn’t impressed. Wilson stuck to his call that the S&P 500 Index would end that year at 2,750 even as the benchmark jumped above 2,900 and the median estimate among 25 Wall Street strategists surveyed by Bloomberg rose to 3,000. Everyone knows what happened next, as the S&P 500 began a long tumble that pushed it down to around 2,500 at the end of last year. In short, Wilson was right to be skeptical, and his views haven’t really changed even though the S&P 500 rebounded to 2,891 on Monday. His year-end forecast is still 2,750, and his reasoning is sound. As Wilson puts it, the recent gains were mainly due to the notion that bad economic news would be good for riskier assets by forcing the Fed to put its rate-hike plans on hold. But that trade is played out. “Unlike in January, I doubt bad fundamental news will be good for stocks any more, given significantly higher valuations today and the fact that the Fed can’t pivot any further at this point without signaling rate cuts,” Wilson wrote in a Sunday research note. “Historically, the first rate cut is a red flag for stocks because it portends even weaker growth, rather than the positive inflection point that comes from a pause.” Wilson adds that the Fed “has fixed” the tight financial conditions that sparked the sell-off. “However, it can’t roll back the corporate cost pressures created by the fiscal stimulus” and “these pressures now have to play out in what we’ve been calling for since last fall — a profits recession.”

THE PRESIDENT WHO CRIED WOLF

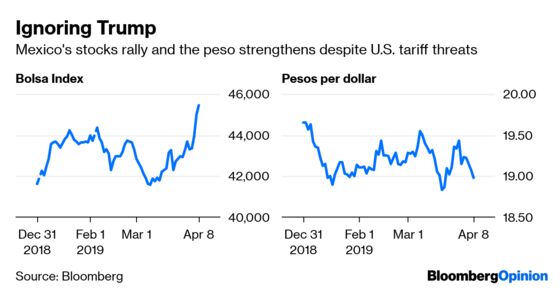

Time was when President Donald Trump could rattle the peso with a tweet or an off-the-cuff remark criticizing Mexico over trade or its handling of immigrants passing through that country on their way to the U.S.’s southern border. No more. The peso gained on Monday despite broader weakness in emerging-market currencies and threats by Trump over the weekend to close the border with its southern neighbor “and/or” tariffs. The peso appreciated as much as 0.84 percent on Monday, strengthening below 19 a dollar in its fourth intraday gain and becoming the biggest driver of the Bloomberg Dollar Spot Index’s decline. The moves suggest that traders are starting to ignore Trump’s repeated threats against Mexico, having seemingly made contradictory remarks about potential tariffs of 25 percent on Mexican–made cars and a border closing. As Bloomberg News’s Sebastian Boyd points out, a lot of U.S. car companies such as Ford, Chysler and General Motors use factories in Mexico, and any tariffs like the one Trump has threatened could harm the U.S. economy. Plus, Mexican auto-parts suppliers such as Metalsa, which makes the chassis for the Chevy Colorado, Chrysler Ram and Ford F-150 pickup trucks, also have plants in the U.S. Tariff-induced pain could also cause them to cut back there, hurting jobs. Mexico’s stock market is also starting to hum, with the benchmark Bolsa IPC rising on Monday to its highest level since November.

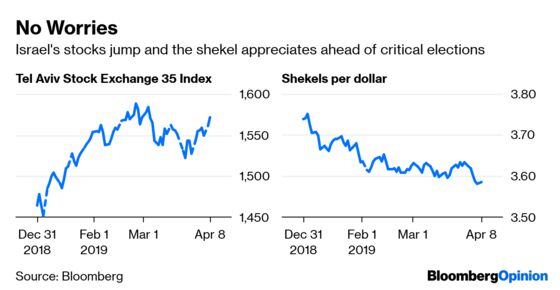

ISRAELI INVESTORS ARE BECALMED

Given Israel’s strategic Middle East location and geopolitical influence, elections there are always an important event. The stakes are higher than usual in this week’s elections, with Prime Minister Benjamin Netanyahu facing the possibility of being indicted for fraud and bribery and, as Bloomberg Opinion contributor Pankaj Mishra puts it, Israel’s traditional support base in the U.S. showing signs of weakness as a more outspoken left seeks to reshape foreign policy. And yet, investors appear unfazed. The shekel has steadily appreciated this year, gaining 4.30 percent in one of the world’s best performances against the dollar. The benchmark Tel Aviv Stock Exchange 35 Index has gained more than 7 percent this year. All this even though the Bank of Israel’s research department on Monday cut its growth forecast for this year to 3.2 percent from 3.4 percent, predicting exports would underperform amid sluggish global trade. Even so, that’s not so bad and the central bank is in an accommodating mood, deciding to keep interest rates at an ultralow 0.25 percent. “We think that the window for rate hikes in Israel is rapidly closing,” Guy Beit-Or, head of macro research at Psagot Investment House Ltd., wrote in a research note. “In the likely event of rate cuts in the U.S. and around the world in 2020, we don’t see a scenario in which the BOI will hike.”

TEA LEAVES

The National Federation of Independent Business’s monthly index of sentiment among U.S. small-business owners had fallen for five straight months through January before showing a small gain for February. So, was that increase the start of a new upswing or a just a pause on the way to a deeper slide? Markets will get some answers Tuesday when the next report is due. The median estimate of economists surveyed by Bloomberg is for another small rise, to 102 from 101.7 in February. But that would still keep the gauge a long way from the 35-year high of 108.8 in August. “Companies in this segment have recently become cautious about taking on new workers, a trend also reflected in the recent ADP private-hiring data by company size,” Bloomberg Economics noted in a research note Monday. “Such vigilance could have been related to uncertainty surrounding small business owners’ expectations for 2018 tax refunds, and will likely be temporary.”

DON’T MISS

The Inverted Yield Curve Needs a Fresh Look: Scholes and Alankar

Libya’s Armed Conflict Could Send Oil Prices Soaring: Julian Lee

A Weak Euro Does What a Fractured ECB Can’t: Marcus Ashworth

China-U.S. Trade Deal Could Be Just a Truce: Mohamed A. El-Erian

Germany Needs to Reboot Its Economic Model: Ferdinando Giugliano

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.